- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

The Bull Case For Viasat (VSAT) Could Change Following New Magnite In‑Flight Ad Partnership – Learn Why

- On 17 June 2026, Magnite Inc. announced a partnership with Viasat Aviation to enable programmatic advertising across Viasat’s in-flight Wi-Fi and entertainment network, spanning more than 60 airlines and over 4,000 aircraft worldwide.

- The deal turns in-flight connectivity into premium, addressable ad inventory, allowing brands to target travelers by route, destination, and events in a highly engaged, previously offline setting.

- Next, we’ll assess how unlocking targeted, programmatic ad revenue from Viasat’s in-flight ecosystem might reshape the company’s broader investment narrative.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

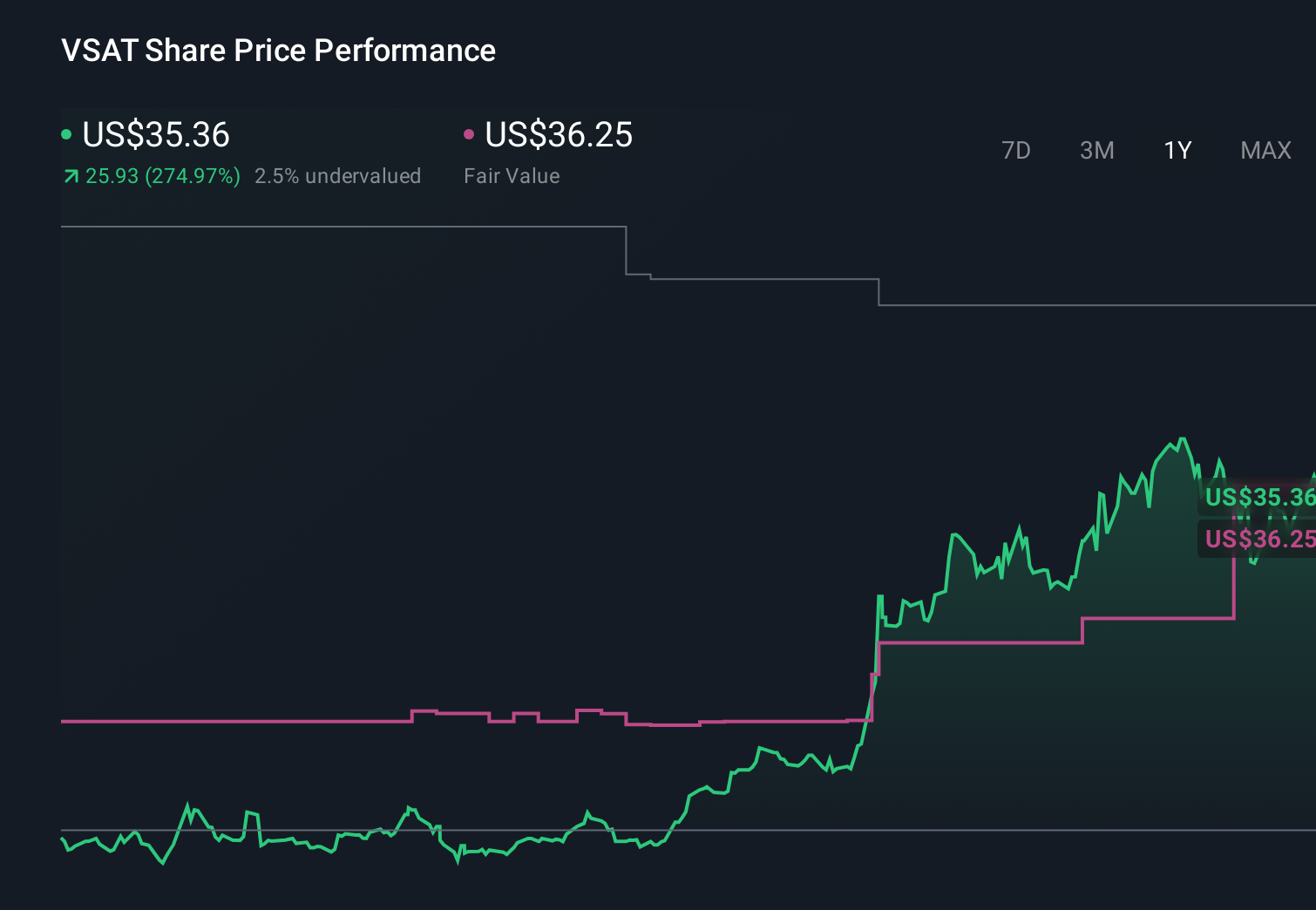

Viasat Investment Narrative Recap

To own Viasat, you need to believe its heavy satellite and Inmarsat investments will convert into higher quality connectivity revenues faster than debt and cash burn become problematic. The Magnite deal adds a new way to monetize existing aviation assets but is unlikely to change the near term focus on integrating ViaSat 3 capacity, managing high CapEx, and stabilizing margins. It modestly supports the aviation growth story, while balance sheet pressure remains the key risk.

The most relevant recent announcement is Viasat’s Q4 2026 result, which showed full year revenue of US$4,640.28 million and a small net loss of US$34.09 million. Against that backdrop, the Magnite partnership looks incremental, potentially improving the economics of in flight connectivity as ViaSat 3 capacity comes online, but it does not yet address the core issues of high capital intensity, leverage, and the challenge of lifting the group to consistent profitability.

Yet while the in flight ad opportunity is exciting, investors should also be aware of...

Read the full narrative on Viasat (it's free!)

Viasat's narrative projects $5.1 billion revenue and $557.4 million earnings by 2029.

Uncover how Viasat's forecasts yield a $51.14 fair value, a 17% downside to its current price.

Exploring Other Perspectives

The most optimistic analysts already saw Viasat reaching about US$5.1 billion in revenue and US$568.8 million in earnings by 2029, while also warning that rapid low Earth orbit disruption could squeeze pricing power, so this new aviation ad angle may either strengthen that bullish view or highlight just how differently you and those analysts might assess Viasat’s future.

Explore 8 other fair value estimates on Viasat - why the stock might be worth as much as 50% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Viasat research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Viasat research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Viasat's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com