- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

SpaceX's Market Cap Quickly Leapfrogged This AI Giant Before Crashing. Here's Which One I'd Buy Today.

Key Points

SpaceX briefly surpassed Amazon's market cap.

Amazon's financial might is much larger than SpaceX's.

Both companies still have a huge potential for growth, making Amazon a better buy today.

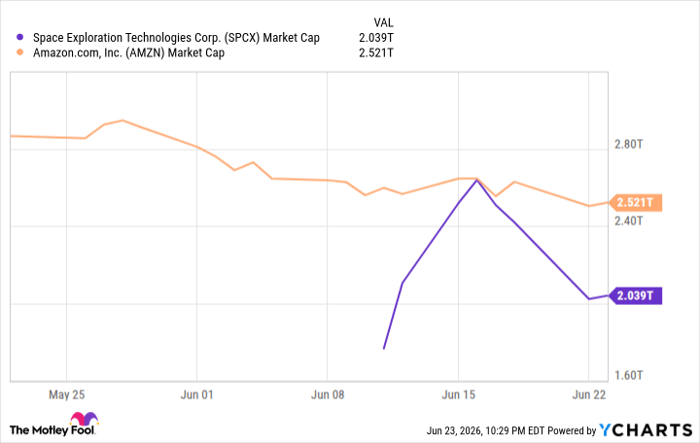

Space Exploration Technologies (NASDAQ: SPCX) has quickly become the most talked-about stock on the market after its gargantuan IPO. For a brief moment in the days after its debut, its market cap soared above Amazon's (NASDAQ: AMZN).

A bit of these gains have been given up, with SpaceX now trading at a market cap of around $2 trillion as of this writing after the close on June 23. However, there is still clearly extreme optimism around SpaceX and its ambitions to dominate the satellite internet and artificial intelligence (AI) markets, with an addressable market projection in the trillions.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

At similar prices, which stock is the better buy: SpaceX, the newcomer, or Amazon? The answer is clear when you get past the headlines.

Revenue and earnings size

There is no comparing SpaceX and Amazon financially right now. In 2025, SpaceX generated $18.7 billion in revenue and reported a $2.6 billion loss from operations. In that same year, Amazon's revenue was $717 billion with operating income of $80 billion.

Amazon's business is significantly more mature than SpaceX's, with a sprawling logistics empire and e-commerce platform spanning the globe, along with a cloud computing division, Amazon Web Services (AWS), that leads its field with $129 billion in revenue.

SpaceX is growing faster on a percentage basis, with 33% revenue growth compared to 12% at Amazon last year. However, when you compare the $638 billion in revenue Amazon generated in 2024 to the $717 billion it generated last year, the company grew revenue by around four times the entire size of SpaceX's business in a single year. This should illustrate the different financial scales on which these two businesses operate.

Image source: Getty Images.

Closer market potential

Looking to the future, both SpaceX and Amazon are pursuing similar markets, aside from Amazon's mature e-commerce empire. Amazon is not trying to directly compete with SpaceX in rocket launches, but that is not a huge market, with SpaceX holding dominant market share today and generating only $4 billion in revenue from its space segment last year.

The two companies overlap in satellite internet and AI data center services. SpaceX's Starlink internet service generated $11.4 billion in revenue last year, up 50% year over year. The company estimates an addressable market of over $1 trillion across the broadband and mobile internet sectors, which it aims to disrupt. Amazon is an up-and-coming competitor to Starlink, investing billions in a satellite constellation it calls Amazon Leo, which should be fully operational within a few years. SpaceX remains far in the lead, though.

SpaceX is trying to tackle the AI data center sector with its acquisition of xAI and major infrastructure investments. It recently signed deals worth tens of billions of dollars annually but generated only $3.2 billion in revenue last year, including revenue from the company formerly known as Twitter. AWS, as mentioned above, generates $129 billion in annual revenue and continues to grow at an impressive clip.

SPCX Market Cap data by YCharts

Why Amazon is clearly the better buy

SpaceX clearly has potential, but Amazon also has massive potential and an existing business that generates significant profits. That cannot be said for the rocket flight and AI business today. SpaceX trades at a price-to-sales ratio (P/S) of over 100 compared to its 2025 revenue. Amazon trades at a price-to-earnings ratio (P/E) -- much different than sales -- of 28.

Smart investors know that valuation matters above all else. Unless SpaceX can miraculously accelerate its revenue growth to 100% annually over the next few years, this current market cap of $2 trillion looks extreme compared to Amazon's massive earnings power. Amazon stock is likely the much better buy for investors over the next few years.

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.