- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

June 2026's Top Value Stocks With Estimated Discounted Valuations

Over the last 7 days, the United States market has experienced a 2.7% decline, yet it remains up 19% over the past year, with earnings projected to grow by 18% annually in the coming years. In this context of fluctuating short-term performance and strong long-term growth expectations, identifying undervalued stocks with discounted valuations can be an effective strategy for investors seeking to capitalize on potential market opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Warrior Met Coal (HCC) | $84.86 | $165.99 | 48.9% |

| Tutor Perini (TPC) | $81.56 | $155.21 | 47.5% |

| Natera (NTRA) | $260.74 | $499.12 | 47.8% |

| MercadoLibre (MELI) | $1619.25 | $3083.54 | 47.5% |

| Luckin Coffee (LKNC.Y) | $30.00 | $58.89 | 49.1% |

| Gold Royalty (GROY) | $2.68 | $5.34 | 49.9% |

| Genuine Parts (GPC) | $112.99 | $224.32 | 49.6% |

| DLocal (DLO) | $12.34 | $24.63 | 49.9% |

| Clear Secure (YOU) | $53.18 | $101.49 | 47.6% |

| Beacon Financial (BBT) | $30.83 | $60.24 | 48.8% |

Let's review some notable picks from our screened stocks.

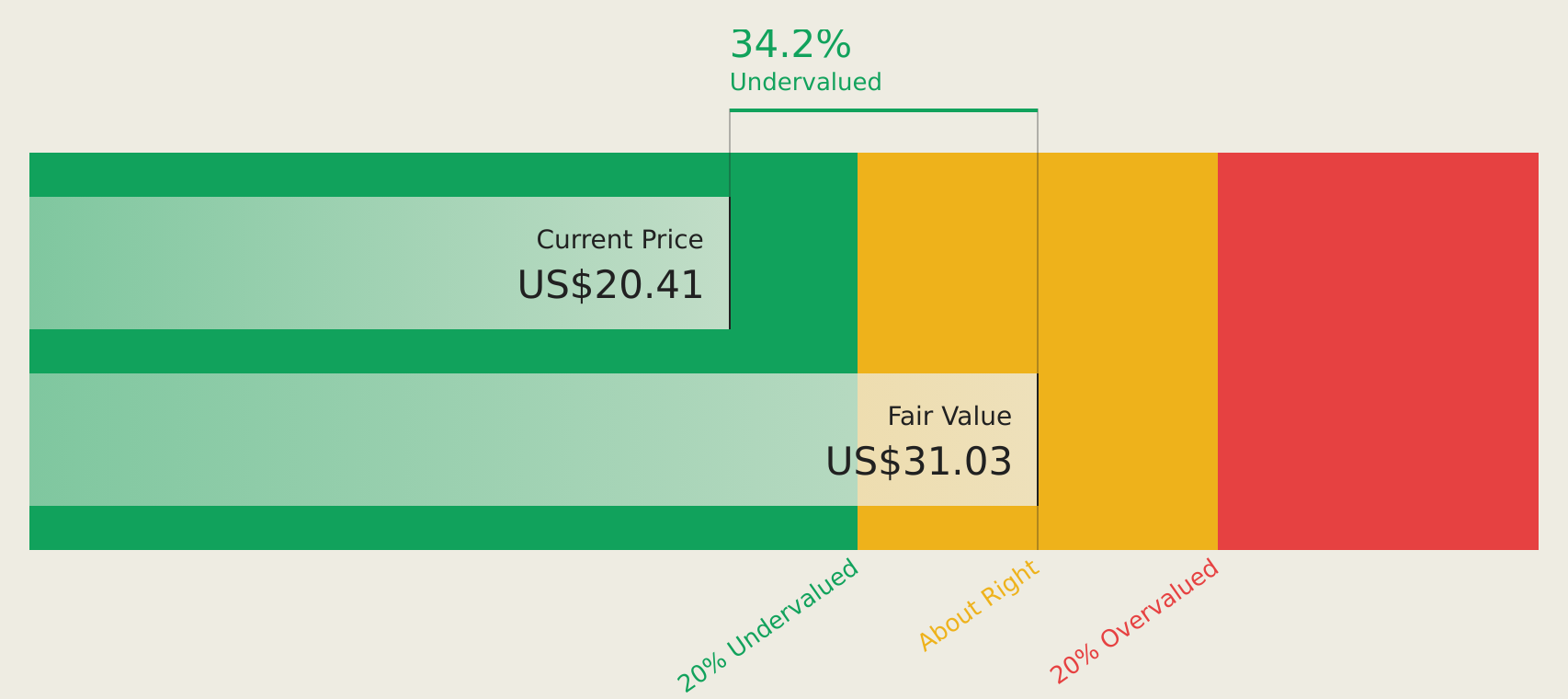

CVB Financial (CVBF)

Overview: CVB Financial Corp. is a bank holding company for Citizens Business Bank, providing banking and financial services to small to mid-sized businesses and individuals, with a market cap of approximately $3.89 billion.

Operations: The company generates revenue primarily from its banking segment, which amounts to $519.40 million.

Estimated Discount To Fair Value: 28.6%

CVB Financial is trading at US$22.46, significantly below its estimated future cash flow value of US$31.47, highlighting potential undervaluation. The company's earnings are forecast to grow 28.23% annually over the next three years, outpacing the broader US market's expected growth rate of 18.5%. Recent strategic actions include a share repurchase program and a stable dividend payout of $0.20 per share for Q2 2026, reinforcing shareholder value focus amidst leadership transitions and mergers.

- Our growth report here indicates CVB Financial may be poised for an improving outlook.

- Get an in-depth perspective on CVB Financial's balance sheet by reading our health report here.

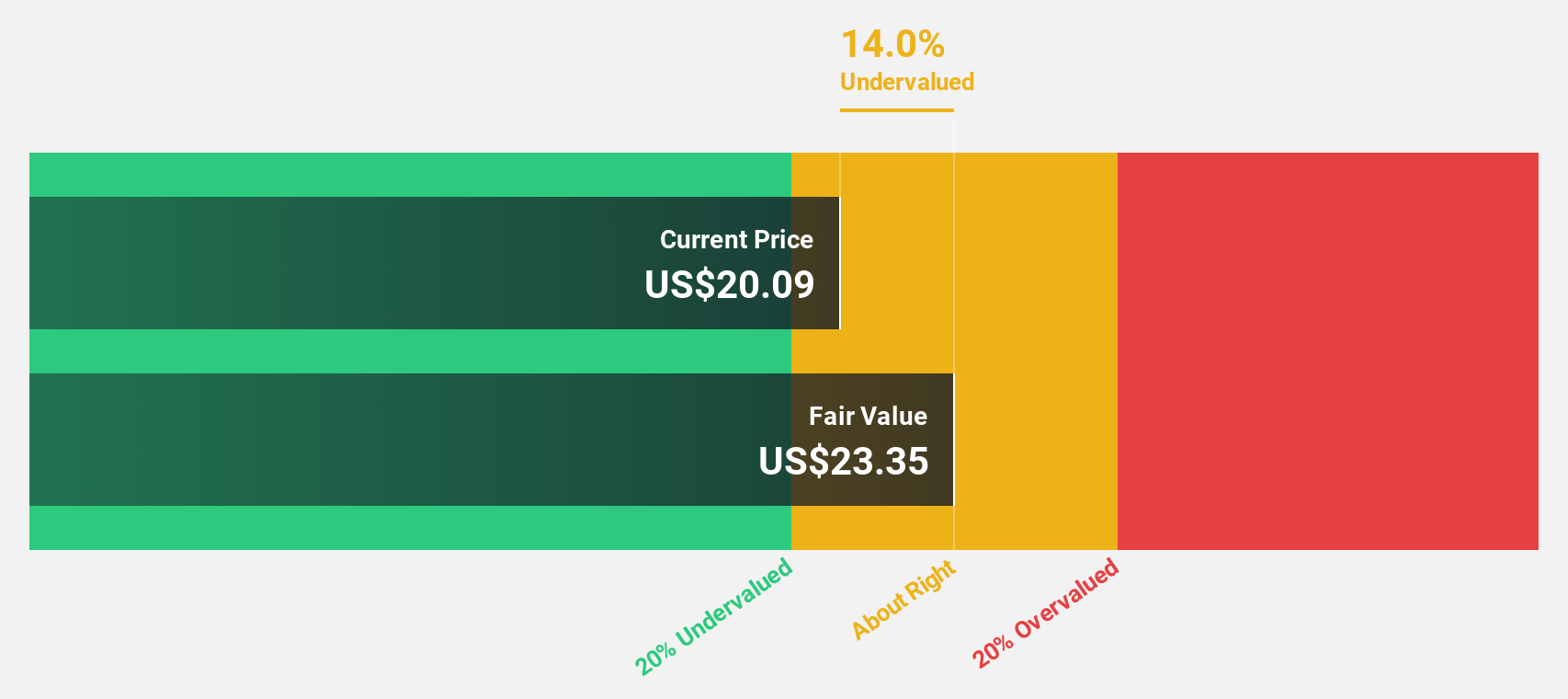

Simmons First National (SFNC)

Overview: Simmons First National Corporation is a bank holding company for Simmons Bank, offering a range of banking and financial products and services to individuals and businesses, with a market cap of approximately $3.29 billion.

Operations: The company generates revenue primarily from its Community and Commercial Banking segment, which accounted for $38.99 million.

Estimated Discount To Fair Value: 37%

Simmons First National is trading at US$22.97, below its estimated future cash flow value of US$36.47, suggesting undervaluation. Revenue growth is projected at 55.3% annually, outpacing the US market significantly. Despite strong earnings growth of 112.84% forecasted per year, the dividend yield of 3.74% may not be sustainable long-term due to coverage issues, and recent shelf registration filings for $73 million could impact future share value dynamics.

- Our comprehensive growth report raises the possibility that Simmons First National is poised for substantial financial growth.

- Unlock comprehensive insights into our analysis of Simmons First National stock in this financial health report.

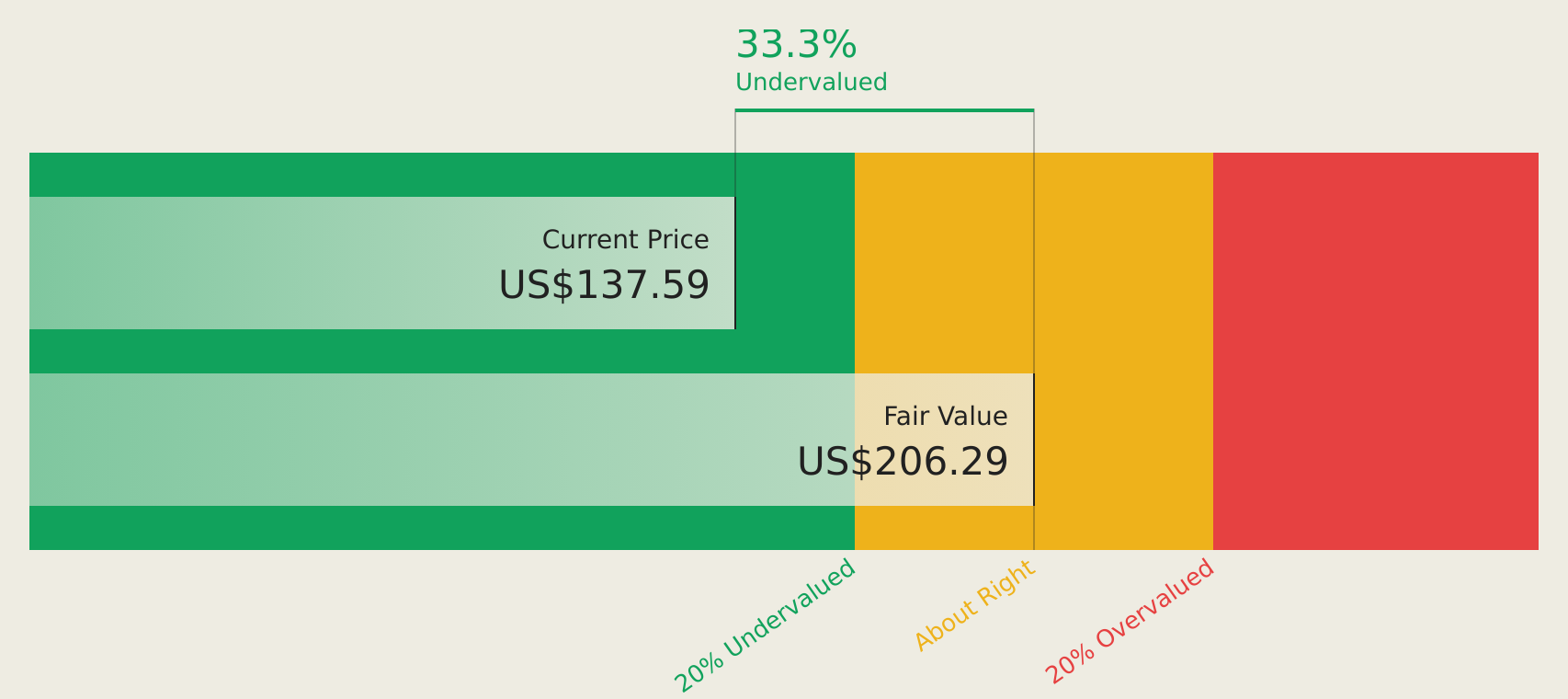

Guidewire Software (GWRE)

Overview: Guidewire Software, Inc. offers a platform for property and casualty insurers globally and has a market cap of approximately $9.19 billion.

Operations: The company's revenue primarily comes from its Software & Programming segment, which generated $1.42 billion.

Estimated Discount To Fair Value: 42.5%

Guidewire Software is trading at US$110.1, significantly below its estimated future cash flow value of US$191.63, highlighting potential undervaluation. The company's earnings are projected to grow by 21.4% annually, surpassing the broader US market's growth expectations. Recent client wins and product innovations like Guidewire Cloud and ProNavigator AI assistant enhance its competitive edge in the insurance technology sector, although substantial insider selling over the past quarter warrants caution for investors.

- According our earnings growth report, there's an indication that Guidewire Software might be ready to expand.

- Dive into the specifics of Guidewire Software here with our thorough financial health report.

Seize The Opportunity

- Click this link to deep-dive into the 130 companies within our Undervalued US Stocks Based On Cash Flows screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com