- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Talen Energy’s US$983 Million Shelf Registration At Talen Energy (TLN) Has Changed Its Investment Story

- In June 2026, Talen Energy Corporation filed a shelf registration to offer up to US$983.54 million of common stock, covering 2,399,998 shares.

- This move gives Talen a flexible way to raise sizable equity capital when conditions suit, which could influence its funding mix and future plans.

- We’ll now examine how this new shelf registration, and the potential equity issuance it enables, affects Talen’s existing investment narrative.

This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

Talen Energy Investment Narrative Recap

To own Talen, you need to believe its mix of nuclear, gas, and data center exposure can translate into durable cash generation despite commodity, regulatory, and leverage pressures. The new US$983.54 million shelf registration could modestly reshape the near term balance between debt and equity funding, but it does not fundamentally change the key near term catalyst, which remains execution on recent plant acquisitions, or the core risk around fossil-heavy assets and balance sheet pressure.

Against this backdrop, the recent regulatory approvals for the Lawrenceburg, Waterford, and Darby plant acquisitions look particularly relevant, since those gas-fired assets expand Talen’s footprint in high demand markets just as it lines up fresh equity capacity. How and when the company chooses to tap this shelf will matter for existing shareholders, especially after a period of sizable buybacks and ongoing focus on deleveraging and funding growth projects.

Yet, while the growth story is appealing, investors should also be aware that...

Read the full narrative on Talen Energy (it's free!)

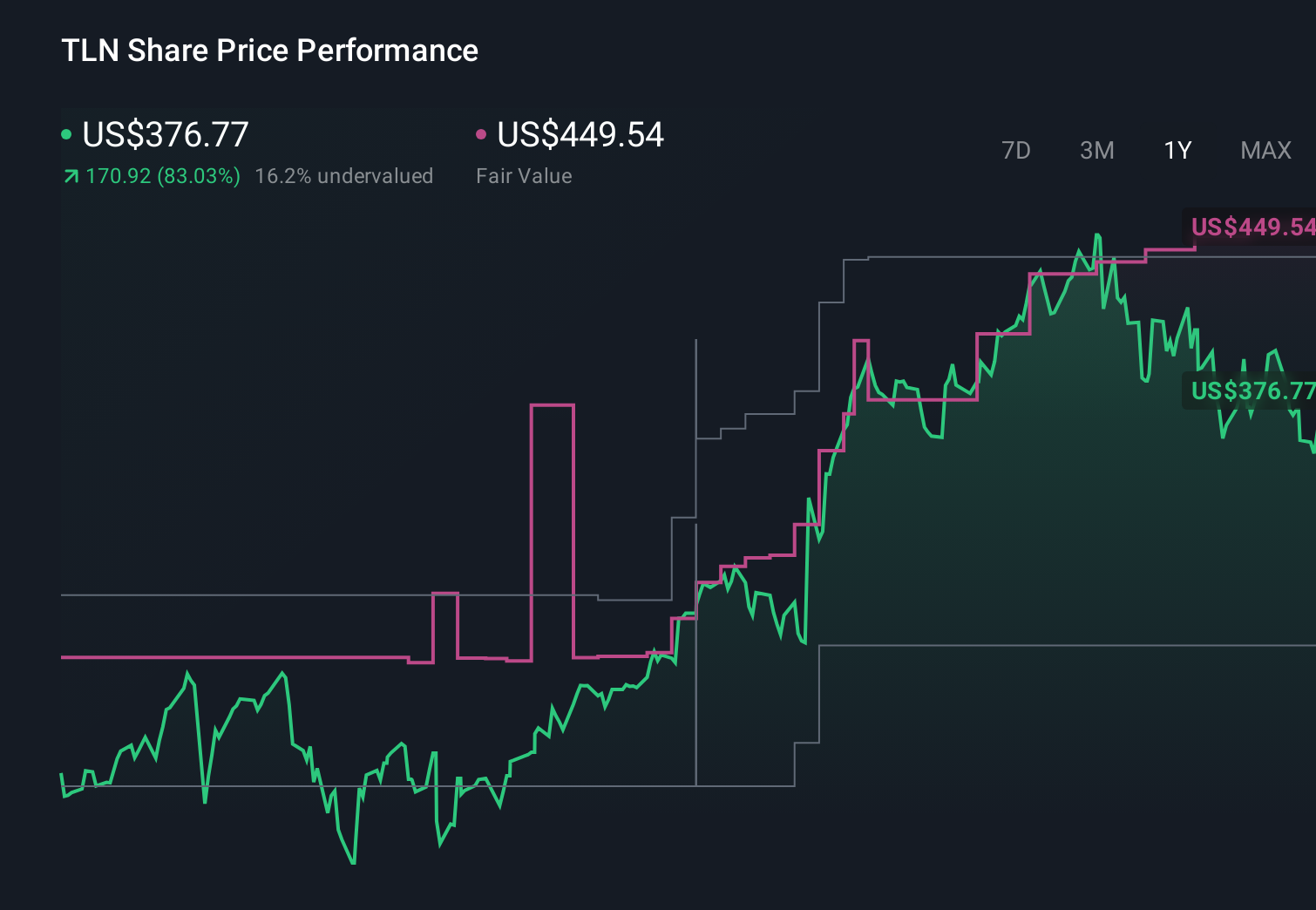

Talen Energy's narrative projects $4.9 billion revenue and $1.4 billion earnings by 2029.

Uncover how Talen Energy's forecasts yield a $469.57 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in roughly US$6.2 billion of revenue and US$2.1 billion of earnings by 2029, so if you are weighing that bullish outlook against concerns about centralized generation and fossil exposure, this new shelf filing is exactly the kind of development that could shift those expectations in different directions.

Explore 5 other fair value estimates on Talen Energy - why the stock might be worth 7% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Talen Energy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Talen Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Talen Energy's overall financial health at a glance.

Want Some Alternatives?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com