- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Emerson Electric (EMR) Draws Fresh Analyst Attention, Is It Still 11% Undervalued?

Analyst coverage sparks fresh attention on Emerson Electric

Recent coverage initiations from DA Davidson and Bernstein have pulled Emerson Electric (EMR) into sharper focus, as investors weigh its exposure to power generation and liquefied natural gas projects against highlighted project and trade risks.

See our latest analysis for Emerson Electric.

Emerson Electric’s share price has been firming, with a 15.90% 90 day share price return and 7.01% year to date share price return, while its 1 year total shareholder return of 11.28% points to momentum that still reflects both recent analyst coverage and expectations for upcoming earnings.

If you are looking beyond Emerson Electric for other ways to position around power and grid themes, this could be a useful moment to check 34 power grid technology and infrastructure stocks

With Emerson Electric trading at $145.34 against an average analyst price target of $163.47, and with mixed views on future projects and earnings, readers need to ask whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 11.1% Undervalued

The most followed narrative on Emerson Electric puts fair value at $163.47 versus the recent $145.34 share price, framing a modest undervaluation that investors are weighing against execution and project risks.

The accelerating adoption of digital automation and artificial intelligence solutions in global industrial markets is fueling strong demand for Emerson's advanced software platforms and AI-enabled products, such as Ovation 4.0 and Nigel AI adviser, which is resulting in robust order growth and positions the company for sustained revenue expansion.

Want to see how this demand story turns into a fair value of over $160 per share? The narrative leans heavily on compounded revenue growth, higher margins, and a richer profit mix. Curious which specific earnings path and valuation multiple underpin that conclusion and how long they are assumed to hold?

Result: Fair Value of $163.47 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Emerson Electric’s story can be knocked off course if large projects are delayed, or if tariffs and currency swings continue to pressure Intelligent Devices margins.

Find out about the key risks to this Emerson Electric narrative.

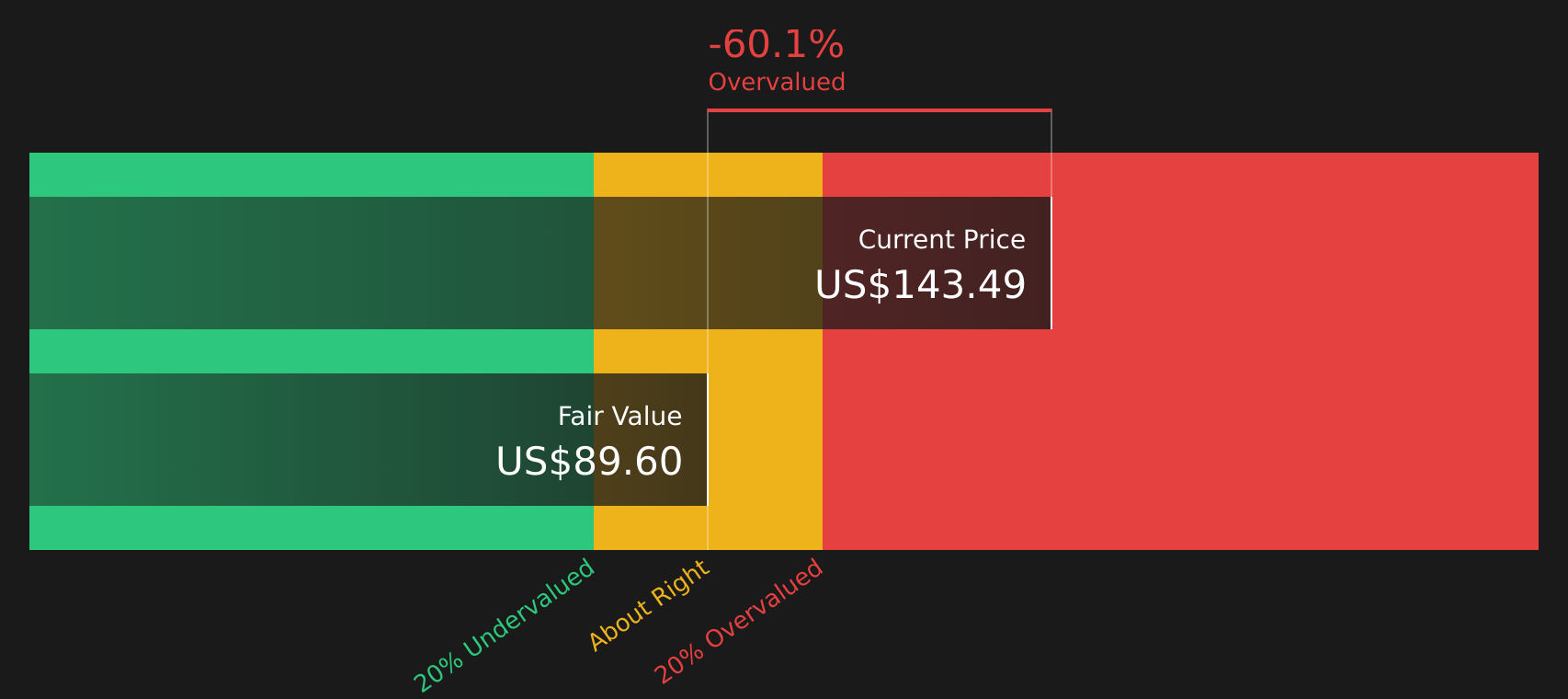

Another angle on Emerson Electric’s valuation

While many investors focus on analyst fair value of $163.47, the Simply Wall St DCF model paints a different picture, with an estimate of future cash flow value at $88.74. That gap implies Emerson Electric could be priced well ahead of its modeled cash generation, so which story do you trust?

For a closer look at how those long term cash forecasts are built and stressed, take a moment with the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Emerson Electric for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After weighing both the upbeat and cautious signals around Emerson Electric, are you ready to move quickly and test the data against your own expectations? To see a concise breakdown of the concerns investors are flagging alongside the potential rewards that keep them interested, take a closer look at the 5 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Emerson Electric?

If Emerson Electric has sharpened your thinking, do not stop here. Broader ideas from the Simply Wall St screener could help you spot opportunities before others.

- Target steadier candidates by reviewing 67 resilient stocks with low risk scores that may suit investors who want fewer surprises from their portfolio.

- Hunt for value by scanning screener containing 19 high quality undiscovered gems that are not yet widely followed but still show solid fundamentals.

- Strengthen your core holdings with the solid balance sheet and fundamentals stocks screener (48 results) to focus on companies with healthier financial positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com