- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

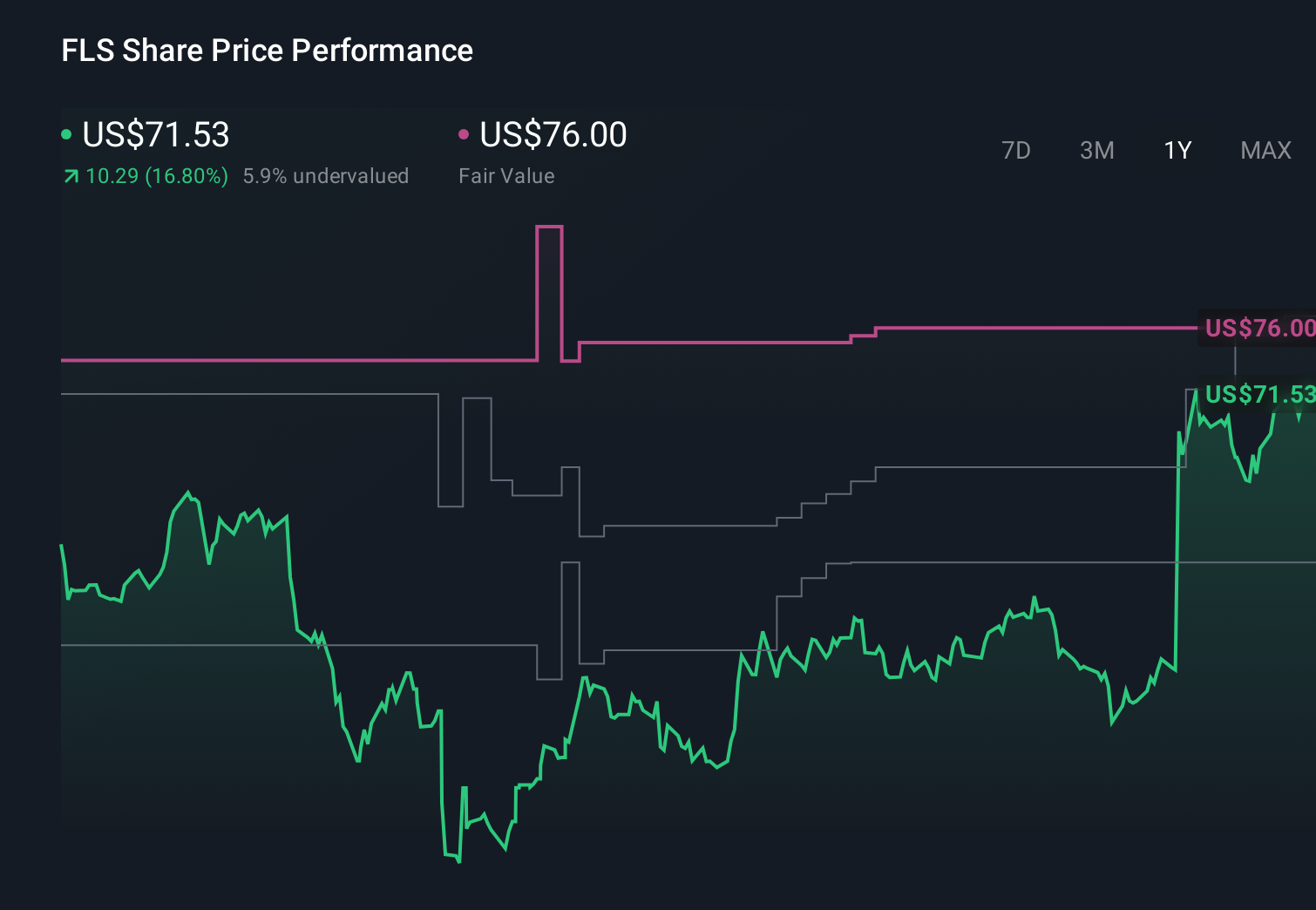

Flowserve (FLS) Is Down 8.2% After TD Cowen Downgrade On Iran Disruption Risks - What's Changed

- Earlier this week, TD Cowen downgraded Flowserve to Hold from Buy, citing geopolitical and operational disruptions linked to the Iran conflict that could force a recalibration of the company’s near-term outlook.

- The broker also suggested that a potential guidance reset, while unsettling in the short term, might ultimately support investor confidence by better aligning expectations with current operating realities.

- We’ll now examine how TD Cowen’s downgrade and the risk of lower guidance may influence Flowserve’s existing investment narrative and assumptions.

Find 43 companies with promising cash flow potential yet trading below their fair value.

Flowserve Investment Narrative Recap

To own Flowserve, you need to believe in its role as a key supplier to energy and industrial projects and its ability to convert a strong backlog into earnings without major disruption. TD Cowen’s downgrade highlights that geopolitical issues around Iran could weigh on near term execution, making earnings guidance and order timing the key near term catalyst and also the most immediate risk if disruptions deepen or persist.

The most relevant recent development here is Flowserve’s April 29 decision to narrow 2026 sales growth guidance to 3% to 6%. That move already acknowledged some pressure on near term growth expectations, so TD Cowen’s concern about a further guidance reset essentially questions whether even this tighter range fully reflects operational and geopolitical headwinds, especially for large, complex projects.

Yet behind the improved margins and solid recent returns, investors also need to be aware of the risk that...

Read the full narrative on Flowserve (it's free!)

Flowserve's narrative projects $5.5 billion revenue and $718.3 million earnings by 2029. This requires 5.9% yearly revenue growth and a $364.3 million earnings increase from $354.0 million today.

Uncover how Flowserve's forecasts yield a $90.00 fair value, a 20% upside to its current price.

Exploring Other Perspectives

The most cautious analysts were already assuming revenue of about US$5.5 billion and earnings of roughly US$691 million by 2029, so TD Cowen’s downgrade and fresh geopolitical risks could prompt them to revisit those expectations, particularly around tariff and supply chain pressures that might further squeeze margins.

Explore 5 other fair value estimates on Flowserve - why the stock might be worth as much as 36% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Flowserve research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flowserve research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flowserve's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com