- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is IQVIA (IQV) Balancing Slower Revenue Momentum With Its Latest Debt Refinancing Move?

- In recent weeks, IQVIA Holdings has come under renewed scrutiny as commentary highlighted its slower revenue growth relative to peers and ongoing softness in demand, alongside a May 2026 move to issue about US$950 million in new senior notes to refinance existing debt.

- This combination of growth headwinds and balance sheet refinancing has sharpened attention on how effectively IQVIA can turn its scale in clinical research and healthcare data into stronger business momentum.

- Now we’ll examine how IQVIA’s recent refinancing amid slower revenue momentum reshapes the company’s investment narrative and risk balance.

Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

IQVIA Holdings Investment Narrative Recap

To own IQVIA, you need to believe its scale in clinical research, data, and AI can translate into steadily improving earnings despite slower recent revenue growth and share price volatility. The key near term catalyst remains execution on its AI and data platforms and converting record backlogs into revenue. The US$950 million senior notes refinancing primarily reframes balance sheet risk rather than the operating story, keeping leverage and interest costs in sharper focus but not changing the core thesis.

The June 2026 decision to issue US$950 million of senior notes due 2033 is the announcement most relevant here, given existing concerns about leverage and refinancing. It sits alongside an enlarged US$15,725 million buyback authorization and recent earnings growth, and together these moves highlight how IQVIA is trying to balance shareholder returns with debt management at a time when revenue growth trails some peers and demand signals appear softer.

Yet against this, investors should be aware that IQVIA's elevated debt and ongoing refinancing needs could...

Read the full narrative on IQVIA Holdings (it's free!)

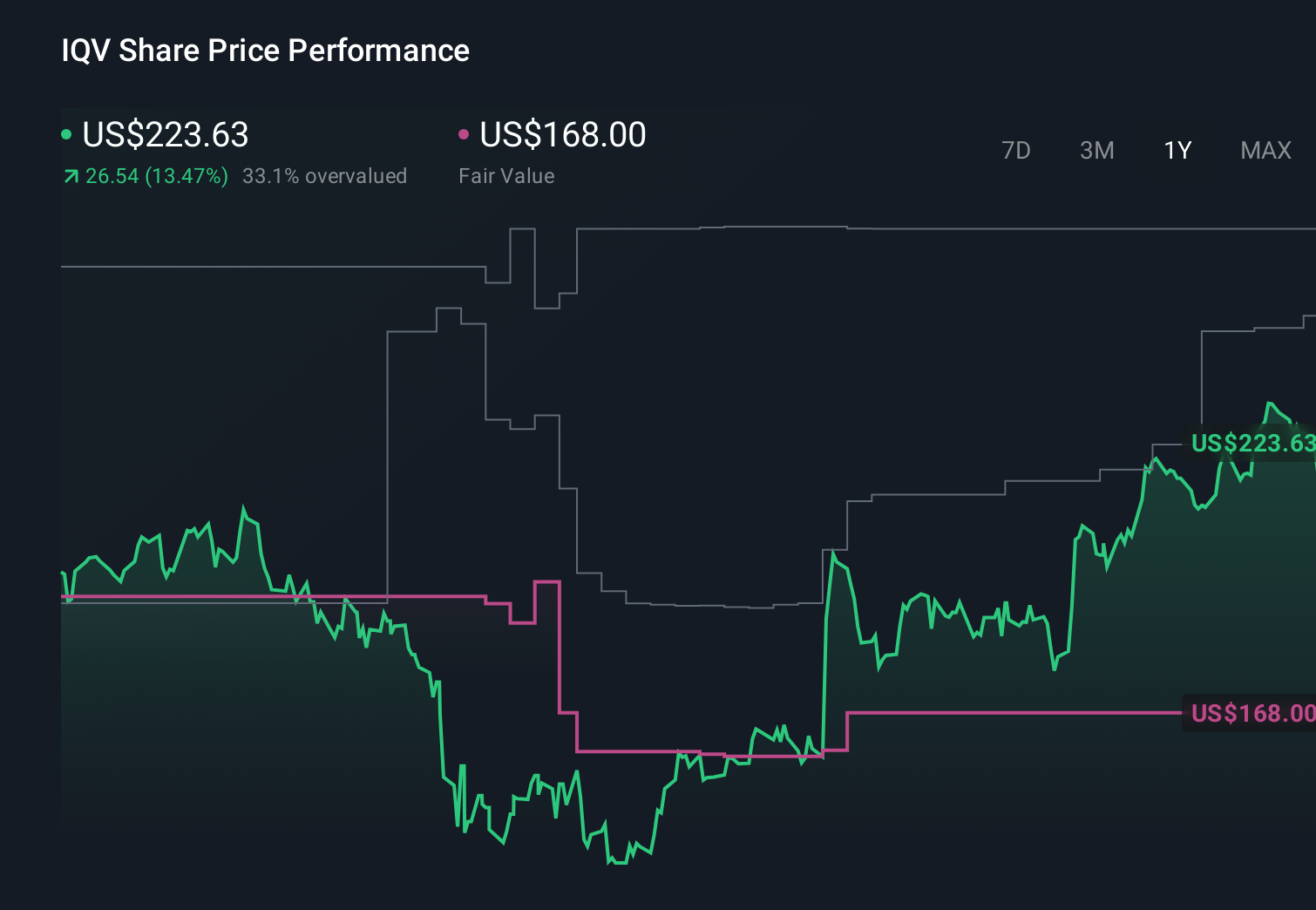

IQVIA Holdings' narrative projects $19.7 billion revenue and $2.0 billion earnings by 2029. This requires 5.8% yearly revenue growth and about a $0.6 billion earnings increase from $1.4 billion today.

Uncover how IQVIA Holdings' forecasts yield a $226.95 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting IQVIA to reach about US$19.1 billion in revenue and US$2.3 billion in earnings by 2028, which is a far more upbeat view than the consensus that already worried about debt and pricing pressure, so this latest refinancing could be exactly the kind of event that pushes you to compare those differing narratives more closely.

Explore 3 other fair value estimates on IQVIA Holdings - why the stock might be worth just $226.95!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your IQVIA Holdings research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free IQVIA Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IQVIA Holdings' overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com