- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Clover Health Investments (CLOV) Could Be 61% Overvalued Following Q1 Profitability

Clover Health Investments (CLOV) is back in focus after reporting solid quarterly results, achieving GAAP profitability in Q1 2026, guiding toward full-year profitability, and securing a 4.5-Star Medicare rating following a favorable court ruling.

See our latest analysis for Clover Health Investments.

Clover Health Investments’ recent Q1 2026 profitability, stronger Medicare rating, and leadership reshuffle around Clover Care Services have arrived alongside sharp share price momentum. The company has reported a 30 day share price return of 42.5% and a 3 year total shareholder return above 4x, even though the 5 year total shareholder return is still down 62.1%. This suggests sentiment has improved, while the longer term picture remains mixed.

If Clover Health’s swing in sentiment has your attention, it may be a good time to see what else is moving in healthcare focused AI, starting with 38 healthcare AI stocks.

With Clover Health Investments now profitable in Q1 2026 and the stock up strongly over the past year, the key question is whether recent gains leave it undervalued or whether the market is already pricing in future growth.

Most Popular Narrative: 60.6% Overvalued

The most followed narrative puts Clover Health Investments' fair value at $3.15 per share, well below the recent $5.06 close. This sets up a clear tension between narrative models and market pricing.

With the U.S. population aging and Medicare Advantage enrollment experiencing double-digit growth industry-wide, Clover's focus on this expanding demographic and its above-market 32% membership growth provide a strong foundation for sustained long-term revenue and earnings expansion.

Want to understand why this growth story still leads to a lower fair value than today’s price? The narrative leans heavily on rapid revenue expansion, a sharp earnings swing, and a rich future profit multiple that assumes investors keep paying up for that progress.

Result: Fair Value of $3.15 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Clover Health’s story still depends on keeping medical costs in check and managing Medicare Advantage policy shifts, which could pressure margins and cash flow.

Find out about the key risks to this Clover Health Investments narrative.

Another View on Clover Health Investments' Valuation

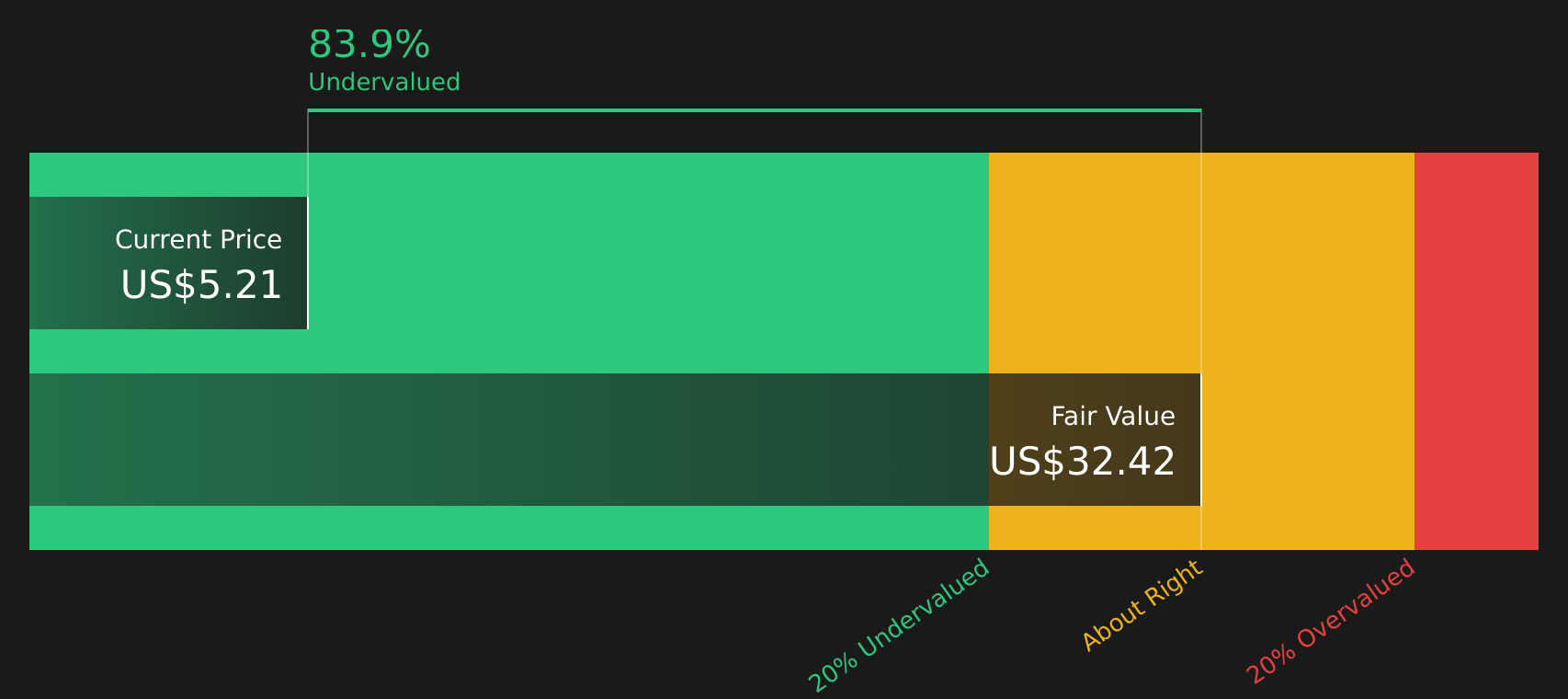

While the narrative model points to Clover Health Investments being 60.6% overvalued at $5.06 versus a $3.15 fair value, the SWS DCF model paints a very different picture, with an estimated future cash flow value of $32.42. That gap is large, so which story do you rely on more: the earnings narrative or the cash flow model?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If the mixed sentiment around Clover Health Investments leaves you uncertain, consider reviewing the key details now and weigh both sides by checking the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Clover Health Investments?

If Clover Health Investments has sharpened your focus, do not stop here. Fresh ideas across sectors could help you build a stronger, more balanced portfolio.

- Target potential bargains by scanning companies that combine quality and value using the 44 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies offering robust yields and payout histories via the 7 dividend fortresses.

- Prioritise resilience by filtering for companies with healthier balance sheets and fundamentals through the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com