- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Can Gap (GAP) Turn Its AI Marketing Pivot Into Durable Brand Loyalty And Margin Gains?

- Gap Inc. recently outlined a major AI-driven overhaul of its marketing operations, partnering with Zeta Global, Google Cloud and Publicis Sapient to build real-time, personalized customer engagement on unified data platforms.

- An interesting angle is how Gap’s leadership frames AI as a tool to free marketers for more creative work while supporting longer-term brand loyalty and its broader sustainability-focused repositioning.

- We’ll now examine how this AI-powered personalization push shapes Gap’s investment narrative, particularly around customer engagement quality and marketing efficiency.

Find 44 companies with promising cash flow potential yet trading below their fair value.

What Is Gap's Investment Narrative?

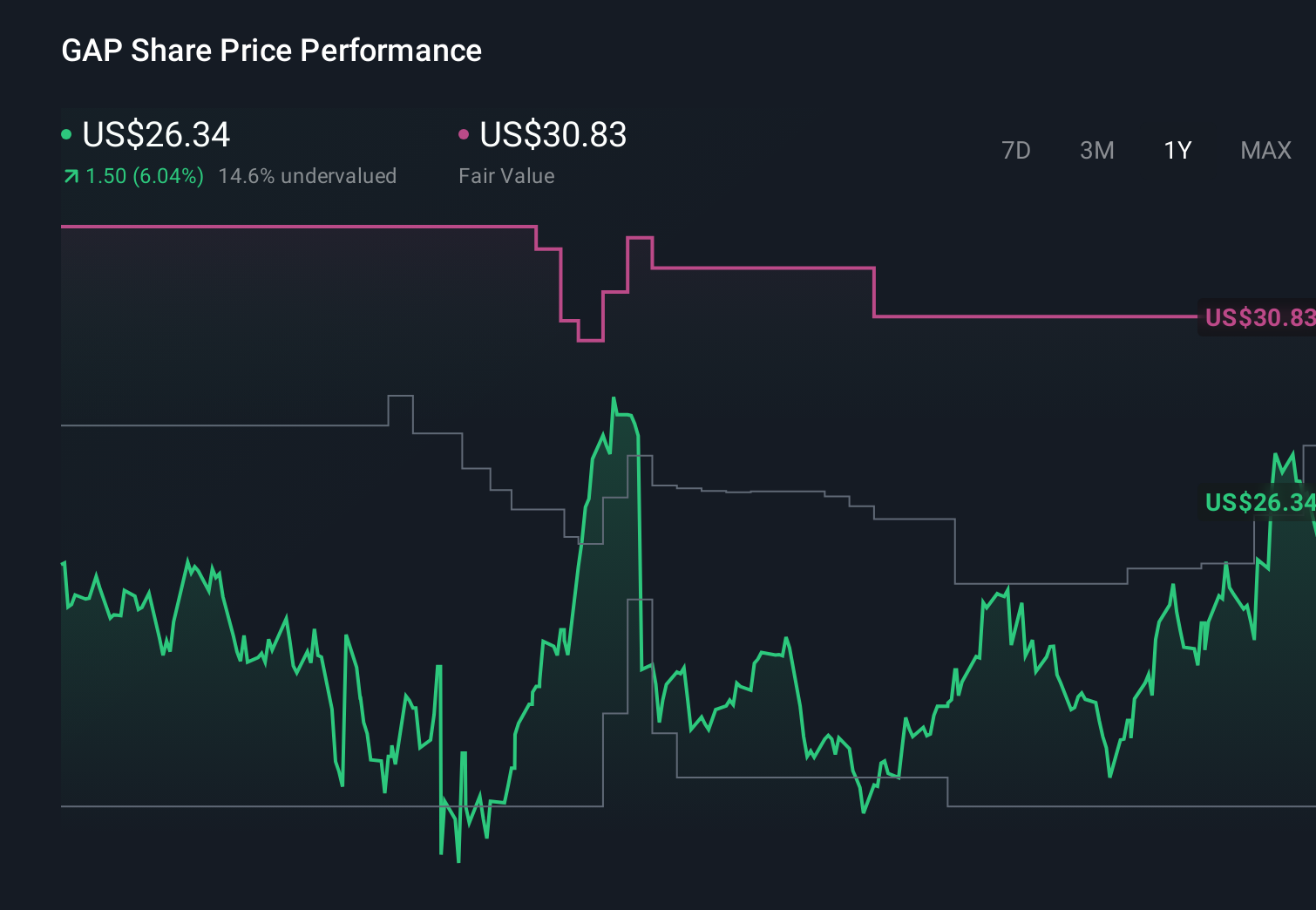

For Gap, the big picture a shareholder has to buy into is a disciplined turnaround story that pairs modest top line growth with tighter operations, high return on equity and active capital returns through dividends and buybacks. Recent AI partnerships with Zeta Global, Google Cloud and Publicis Sapient sit right at the heart of that thesis: if they lift marketing efficiency and deepen customer engagement, they could reinforce current earnings guidance and make the existing valuation gap to analyst targets more interesting, even as the share price has pulled back this year. In the short term, though, the material catalysts still look grounded in execution on merchandise, traffic and margin, while the AI-driven marketing overhaul introduces fresh execution risk and upfront investment before any benefits are clear.

However, investors should be aware of the new execution and data-dependency risks this AI shift introduces. Despite retreating, Gap's shares might still be trading 41% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Seven Simply Wall St Community members see Gap’s fair value between about US$22.60 and US$36.12, showing how far opinions can stretch. Set that against Gap’s AI heavy marketing reset and recent share price weakness, and you can see why many investors are rethinking what could realistically drive or cap the company’s next phase of performance.

Explore 7 other fair value estimates on Gap - why the stock might be worth just $22.60!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Gap research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gap research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gap's overall financial health at a glance.

No Opportunity In Gap?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com