- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Is NNN REIT’s Term Loan Expansion and Swap Strategy Quietly Recasting Its Risk‑Return Profile (NNN)?

- NNN REIT, Inc. recently exercised a US$200 million incremental term loan option, expanding its senior unsecured term loan facility to US$500 million maturing in 2029, while also amending term loan and revolver pricing grids to slightly reduce SOFR-based borrowing margins.

- By layering in a US$100 million forward starting swap to lock SOFR and modestly lowering its credit facility spreads, NNN REIT is fine‑tuning its funding costs and interest rate profile in a way that could matter for long-term capital planning and balance sheet resilience.

- Next, we’ll examine how this expanded US$500 million term loan and interest-rate swap reshape NNN REIT’s investment narrative and risk profile.

We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

NNN REIT Investment Narrative Recap

To own NNN REIT, you need to be comfortable with a steady, income focused retail REIT that relies on disciplined acquisitions and careful balance sheet management. The new US$200 million term loan and US$100 million swap modestly refine NNN’s near term interest expense rather than transform its biggest catalysts or its key risk around funding costs and tenant stability.

The most relevant recent data point here is NNN’s ongoing use of its 2025 term loan framework, which originally provided US$300 million with an upsizing option to US$500 million. By fully activating that structure and slightly improving SOFR based margins on both the term loan and revolver, NNN is adjusting its capital stack in line with its existing earnings and dividend guidance, rather than changing those targets outright.

Yet while this financing supports balance sheet resilience, investors should still be aware of how persistent or rising interest rates could...

Read the full narrative on NNN REIT (it's free!)

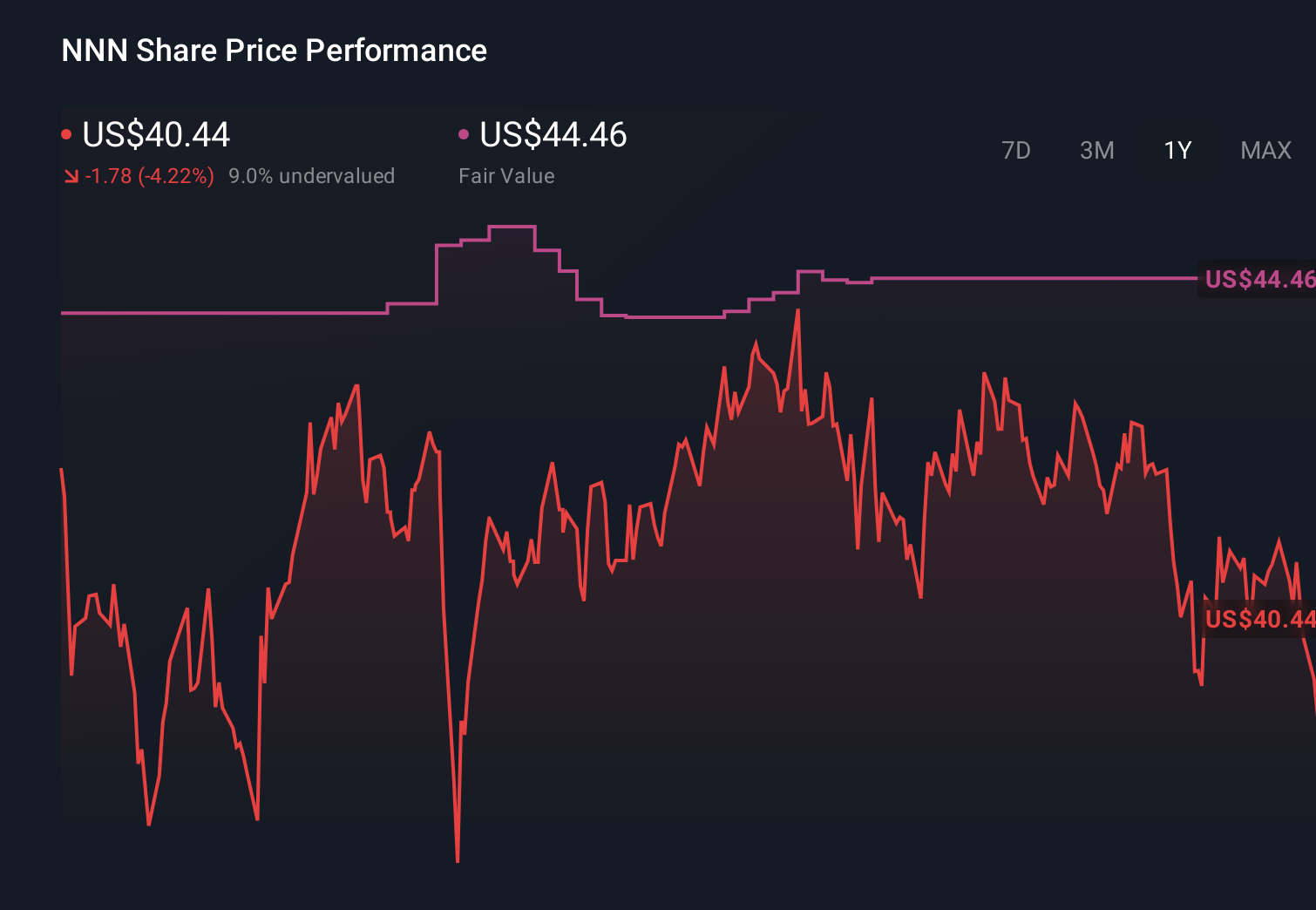

NNN REIT’s narrative projects $1.1 billion revenue and $448.9 million earnings by 2029. This requires 4.7% yearly revenue growth and about a $62.4 million earnings increase from $386.5 million today.

Uncover how NNN REIT's forecasts yield a $46.23 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members currently bracket NNN’s fair value between US$46.23 and US$81.27 across 2 independent views, underlining how far opinions can stretch. You can weigh those against the interest rate and tenant risks around NNN’s growing debt load and decide which set of assumptions you find more convincing.

Explore 2 other fair value estimates on NNN REIT - why the stock might be worth as much as 77% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NNN REIT research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NNN REIT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NNN REIT's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com