- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Cavco Industries (CVCO) Stock Could Be 4% Undervalued After Strong Quarterly Results

Cavco Industries (CVCO) has drawn fresh attention after reporting year-over-year increases in quarterly revenue and net profit, alongside a strong financial score and technical buy signals that together highlight shifting sentiment around the stock.

See our latest analysis for Cavco Industries.

Cavco Industries’ recent trading action has been strong, with a 30-day share price return of 18.14% and a 90-day share price return of 26.57%, while the 1-year total shareholder return sits at 46.81%. This suggests momentum has been building over both shorter and longer horizons.

If Cavco’s recent move has you thinking about where else growth stories might be emerging, it could be a good time to scan 20 top founder-led companies

With Cavco Industries trading near US$601 and sitting only about 4% below one analyst price target, yet at an indicated 22% discount to an intrinsic value estimate, you have to ask whether there is still a buying opportunity here or whether the market is already pricing in future growth.

Most Popular Narrative: 4% Undervalued

The most followed narrative for Cavco Industries puts fair value at $625, slightly above the last close of $601.51. This frames the stock as modestly discounted rather than deeply mispriced.

The ongoing housing affordability crisis continues to drive significantly higher demand for manufactured homes, with Cavco reporting strong volume growth and sequential increases in both shipments and pricing. This points to durable revenue expansion as affordability constraints persist for traditional housing.

Want to see what is built into that view on Cavco Industries? The narrative leans on steady top line compounding, firm margins and a richer earnings multiple, and then connects those pieces to reach a higher present value.

Result: Fair Value of $625 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this Cavco Industries narrative can be challenged if higher tariffs lift component costs faster than pricing can adjust, or if regional housing demand remains uneven.

Find out about the key risks to this Cavco Industries narrative.

Another View on Cavco Industries Valuation

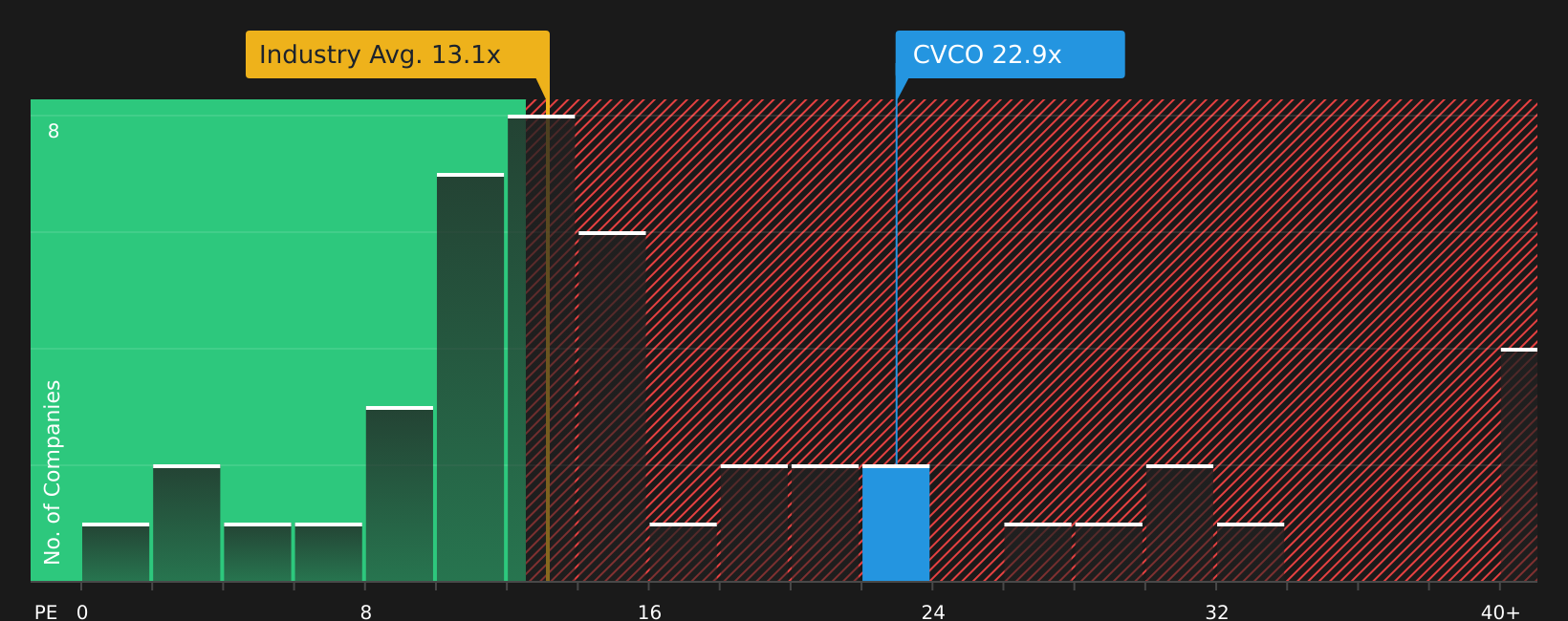

The first narrative paints Cavco Industries as modestly undervalued, but the current P/E of 24.3x tells a different story. That multiple sits well above peers at 17.2x and even above a fair ratio of 19.2x, which hints at less valuation cushion if growth expectations are tested.

For an investor comparing Cavco with other consumer durables stocks, a P/E this far above both peers and a fair ratio can mean paying up for quality or simply paying too much. The key question is whether the earnings path ahead really justifies that premium.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mixed signals on Cavco Industries leave you undecided, take a closer look at the underlying data and move quickly to form your own stance by reviewing the 3 key rewards

Looking for more investment ideas beyond Cavco Industries?

Do not stop with Cavco Industries. If you want a broader view of potential opportunities, use the Simply Wall Street Screener to quickly surface stocks that fit your criteria.

- Target higher yield potential by checking out companies that feature 8 dividend fortresses and see which payouts currently stand out.

- Strengthen your downside protection by focusing on businesses highlighted in the 66 resilient stocks with low risk scores and compare how their risk profiles stack up.

- Spot tomorrow's potential standouts early by reviewing the screener containing 19 high quality undiscovered gems before everyone else starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com