- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Investors May Respond To WisdomTree (WT) Upbeat Analyst Upgrade And Earnings Outlook Reassessment

- Recently, Zacks Equity Research highlighted WisdomTree, Inc. as a strong growth stock, citing its favorable Growth Score, Zacks Rank #2, and earnings estimate revisions that point to earnings per share expected to grow faster than the industry average.

- This endorsement underscores how analyst upgrades and improving earnings expectations can reinforce confidence in WisdomTree’s growth profile and business momentum.

- We’ll now explore how this upbeat reassessment of WisdomTree’s earnings outlook may influence the company’s broader investment narrative.

Find 45 companies with promising cash flow potential yet trading below their fair value.

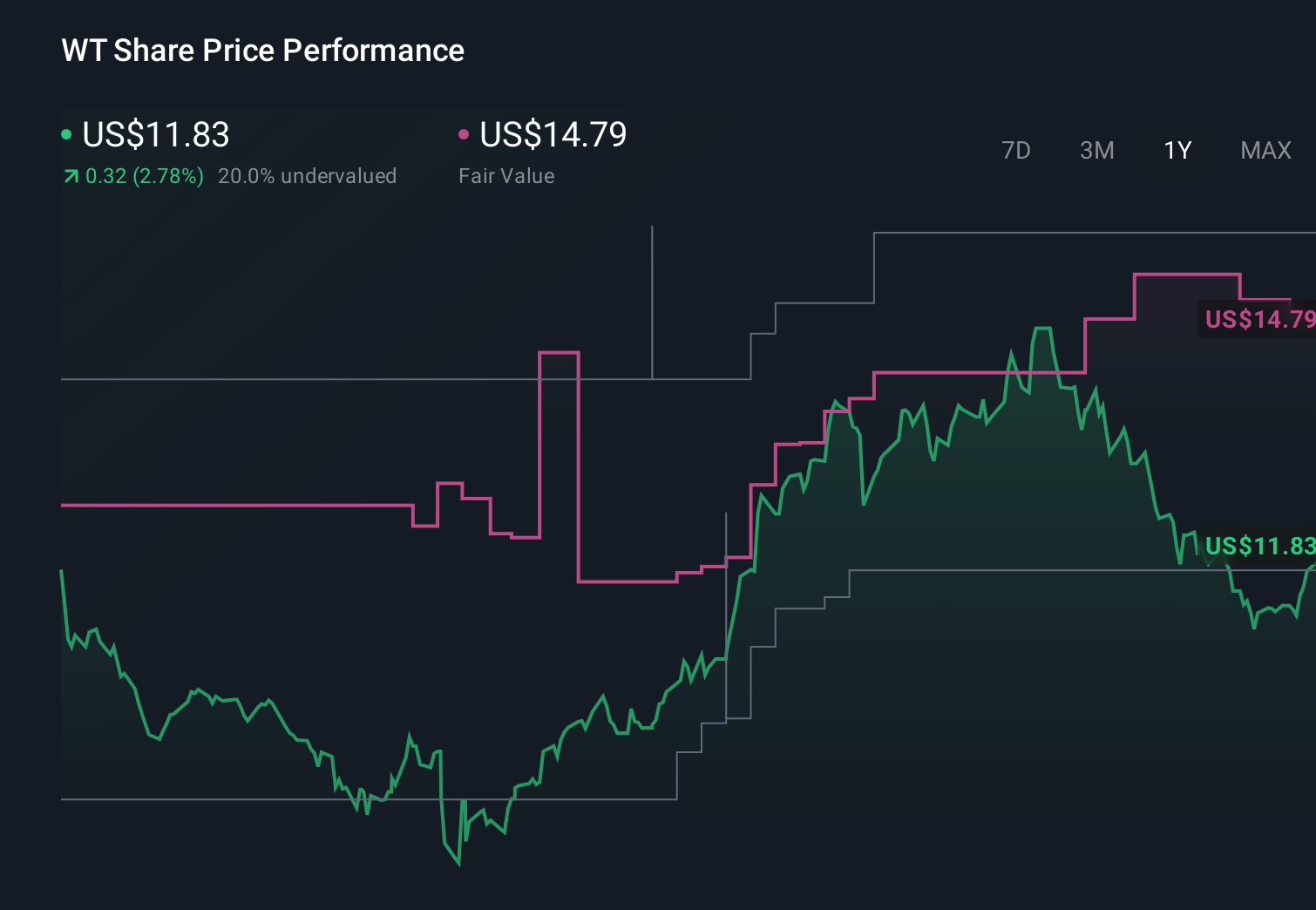

WisdomTree Investment Narrative Recap

To own WisdomTree, you need to believe it can keep turning product innovation, digital assets and alternative exposures like farmland into durable fee growth, despite industry-wide fee pressure and competition from larger managers. The recent Zacks upgrade, pointing to faster expected EPS growth than the industry, reinforces the near term earnings momentum catalyst but does not materially change the key risk that higher spending and volatile performance fees could still unsettle profits.

Among recent developments, the launch of several “efficient” and thematic ETFs, such as WDIG and WDRN, looks most relevant. These funds align with the earnings focused story behind the Zacks upgrade, since they aim to broaden WisdomTree’s product set and fee pool, but they also add complexity and execution risk around scaling new strategies in already crowded ETF categories.

Yet beneath the upbeat earnings outlook, investors should be aware that growing exposure to illiquid farmland and fast evolving digital asset regulation could...

Read the full narrative on WisdomTree (it's free!)

WisdomTree's narrative projects $905.2 million revenue and $303.1 million earnings by 2029.

Uncover how WisdomTree's forecasts yield a $19.97 fair value, a 9% upside to its current price.

Exploring Other Perspectives

While Zacks highlights improving EPS expectations, the most cautious analysts were assuming roughly US$758,000,000 in revenue and US$248,000,000 in earnings by 2029, showing how sharply opinions can differ and why it is worth weighing both the fee pressure and digital asset risks alongside this more pessimistic view.

Explore 3 other fair value estimates on WisdomTree - why the stock might be worth as much as 9% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your WisdomTree research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free WisdomTree research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate WisdomTree's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com