- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Launching an International Leaders ETF Sharpen Federated Hermes’ Active Identity or Blur It (FHI)?

- Earlier this month, Federated Hermes, Inc. launched the Federated Hermes International Leaders ETF (FHIL), an actively managed fund focused on developed-market equities of high-quality foreign companies trading below estimated intrinsic value, managed by the firm’s long-tenured International Core/Value team.

- The ETF extends Federated Hermes’ international equity capabilities into the ETF wrapper, aiming to couple active value-oriented stock selection with the structural benefits of tax efficiency, transparency, and exchange trading.

- Next, we’ll examine how this new international leaders ETF, leveraging an existing mutual fund track record, affects Federated Hermes’ investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you need to believe in its ability to defend active-management fees while growing across cash, fixed income, and now ETFs. The new International Leaders ETF modestly reinforces the growth catalyst around expanding product breadth, but does not materially change the key short term risk of fee pressure and competition from low cost passive products.

Among recent developments, the Q1 2026 results, with revenue of US$478.96 million and EPS of US$1.27, matter most here because they show the firm adding products like FHIL from a position of financial strength, including continued dividends and buybacks, which can support confidence as it tests investor appetite for higher fee active ETFs.

Yet, investors should also be aware that growing regulatory complexity, particularly around ESG and digital assets, could...

Read the full narrative on Federated Hermes (it's free!)

Federated Hermes’ narrative projects $2.0 billion revenue and $422.1 million earnings by 2029.

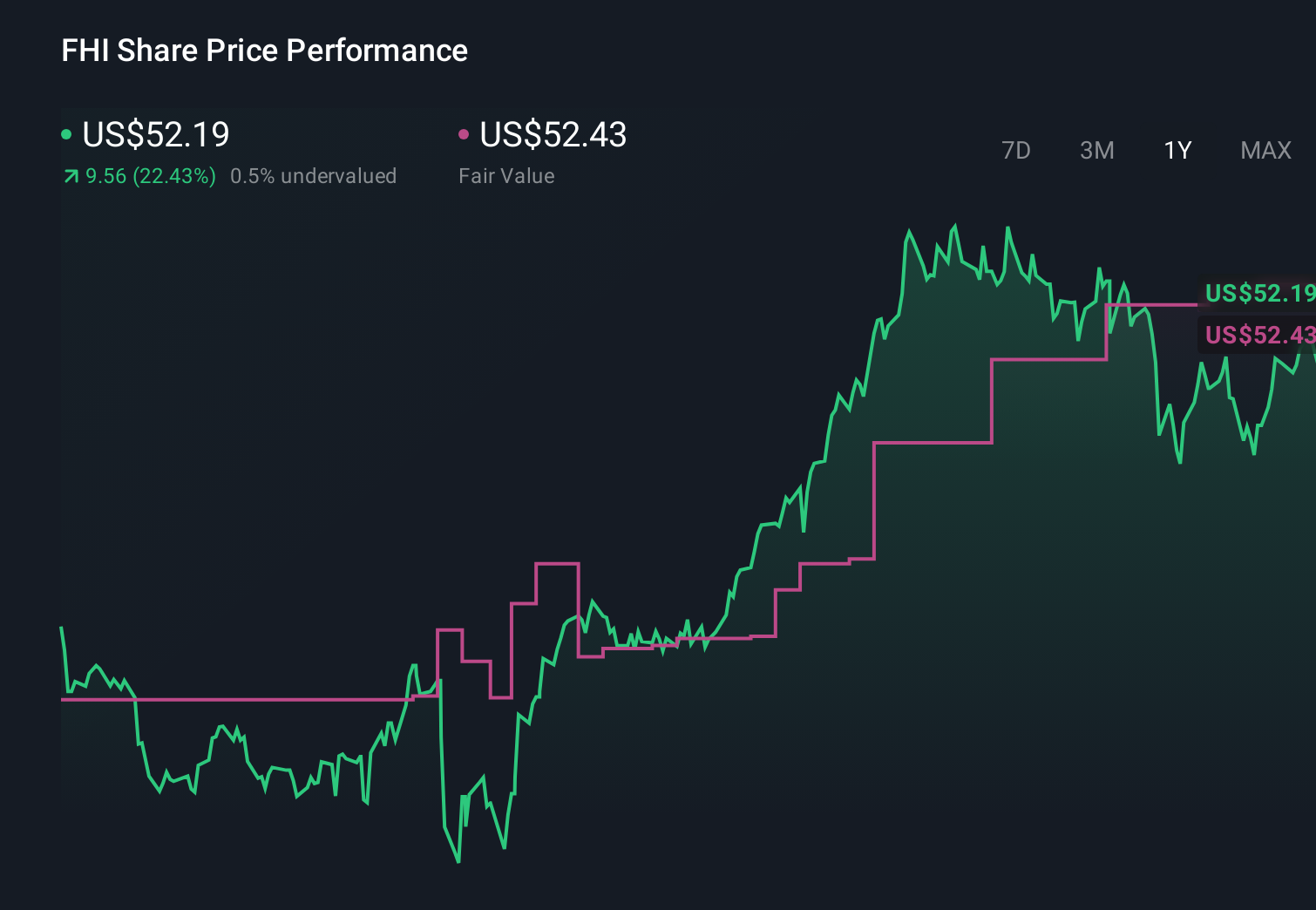

Uncover how Federated Hermes' forecasts yield a $54.71 fair value, a 7% downside to its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for Federated Hermes span roughly US$52 to US$69, underlining how far apart individual views can be. When you weigh those against growing money market and ETF franchises, it becomes even more important to compare several perspectives on how sustainable the business mix really is.

Explore 3 other fair value estimates on Federated Hermes - why the stock might be worth 11% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com