- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How Investors May Respond To V2X (VVX) Surging Institutional Ownership And Contract-Driven Earnings Narrative

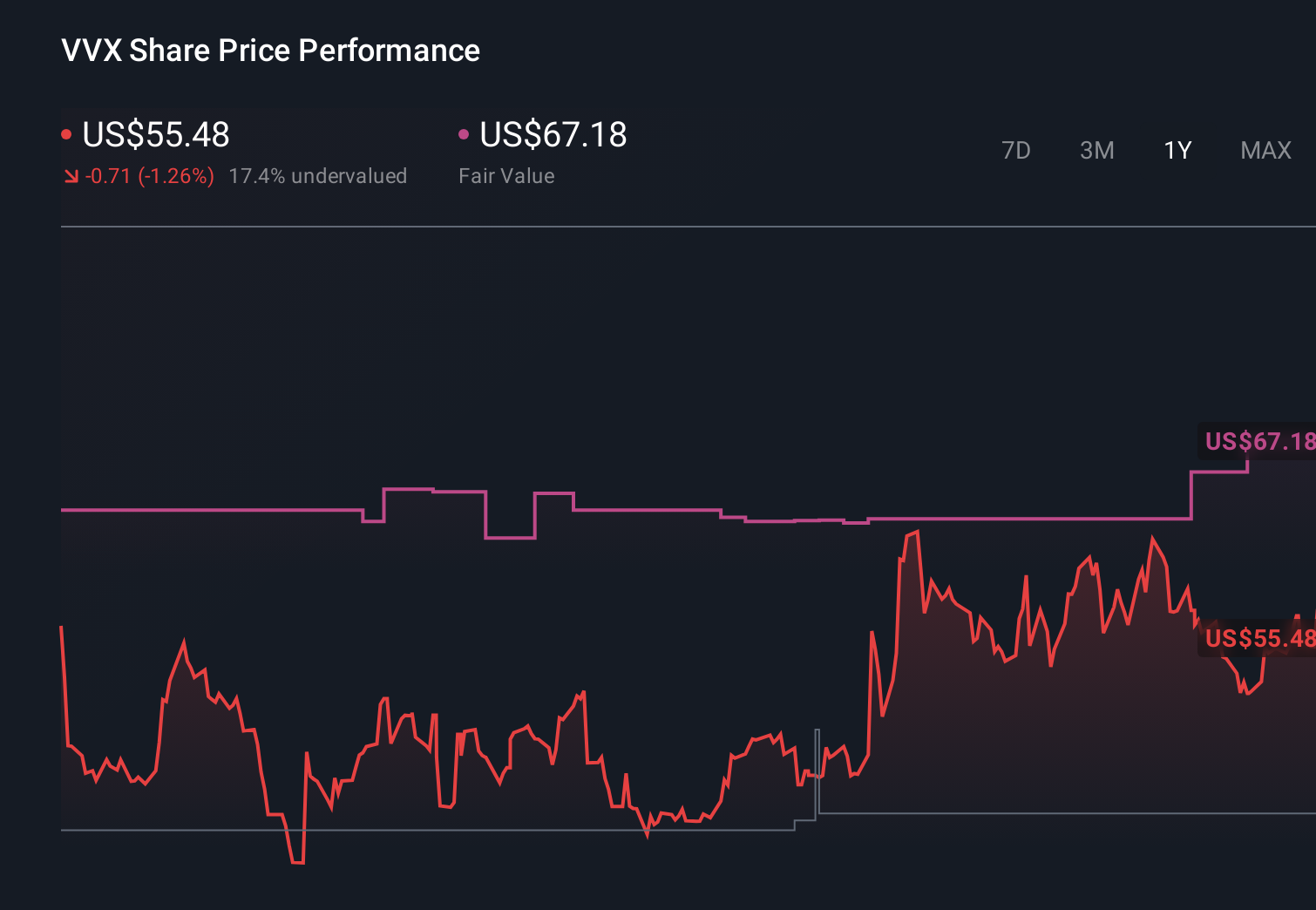

- In recent months, V2X Inc. has seen its institutional ownership rise to 101.86%, ranking first among 74 Aerospace & Defense peers, while its current P/E ratio of 30.36 sits between its recent high and low.

- This very high level of institutional participation, led by ETHSX’s increased holdings, signals strong professional investor engagement with V2X’s equity story.

- We’ll now examine how this surge in institutional ownership interacts with V2X’s contract-driven growth narrative and earnings outlook.

The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

V2X Investment Narrative Recap

To own V2X, you need to believe its contract-driven model can convert a large defense and services pipeline into growing earnings without major execution missteps. The recent jump in institutional ownership above 100% underscores strong professional interest, but does not materially change the core near term catalyst: winning and ramping large contracts like T 6 while managing margins on fixed price work. The biggest current risk remains timing and execution on these episodic awards and their impact on backlog.

Among recent announcements, the resumption of work on the US$4.3 billion T 6 COMBS contract after the protest denial stands out as most relevant. This award directly supports the contract win and execution narrative that institutional investors appear to be leaning into, while also highlighting the ongoing protest and timing risk that can disrupt revenue visibility. How effectively V2X performs on T 6 will likely shape confidence in future awards and earnings quality.

Yet behind the strong institutional buying, investors should be aware that contract protests, timing gaps and backlog trends can quickly change the picture...

Read the full narrative on V2X (it's free!)

V2X's narrative projects $5.5 billion revenue and $196.9 million earnings by 2029. This requires 5.1% yearly revenue growth and about a $108 million earnings increase from $88.7 million today.

Uncover how V2X's forecasts yield a $79.42 fair value, a 7% downside to its current price.

Exploring Other Perspectives

While recent institutional buying suggests confidence, the most pessimistic analysts were still only modeling about US$5.3 billion of revenue and US$142.2 million in earnings by 2029, reminding you that views on automation risk and contract dependence can differ widely and may be revised as this new ownership and valuation data settles in.

Explore 3 other fair value estimates on V2X - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your V2X research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free V2X research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate V2X's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Find 45 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com