- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

TIC Solutions (TIC) Stock Could Be 28.6% Undervalued After Loan Repricing

TIC Solutions (TIC) has drawn fresh attention after completing the repricing of about US$1.6b in First Lien Term Loan debt, cutting the margin to SOFR + 250 basis points while keeping the 2031 maturity unchanged.

See our latest analysis for TIC Solutions.

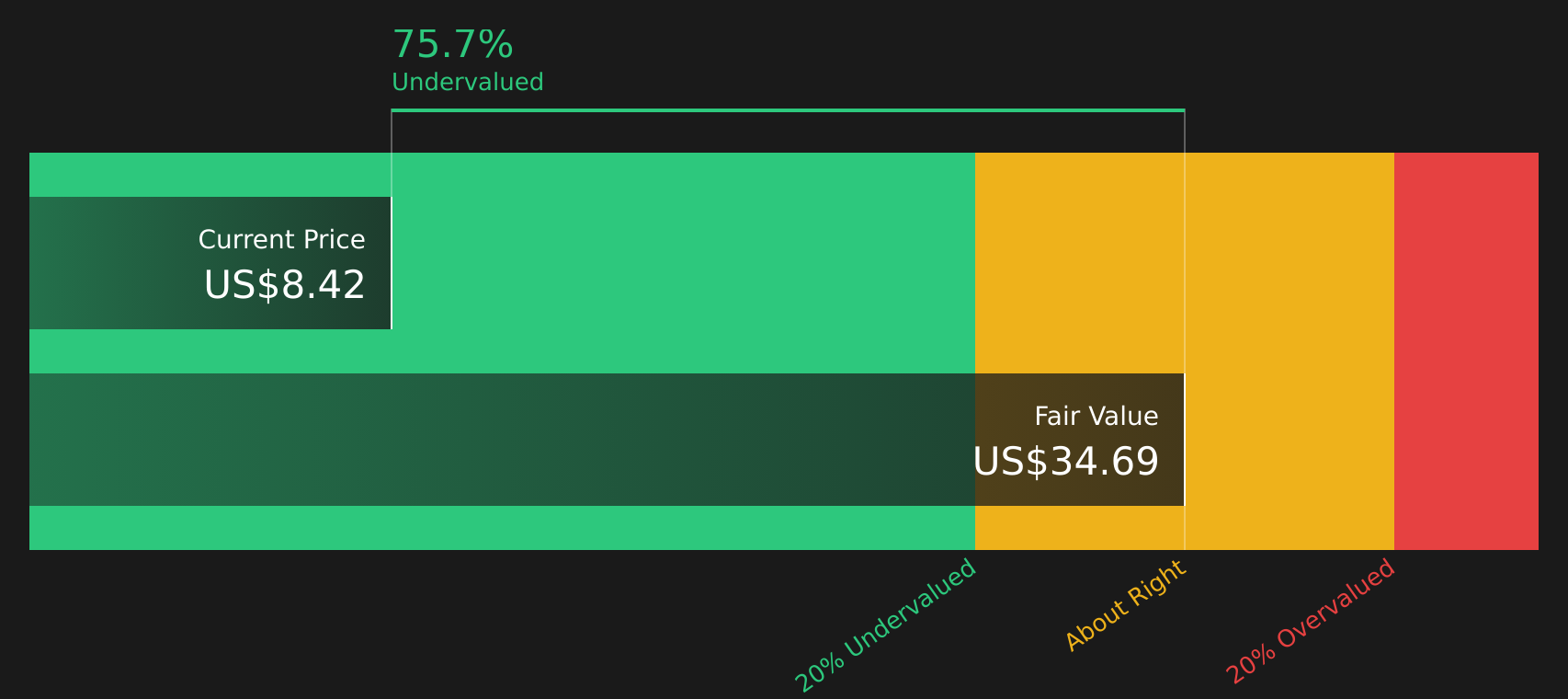

The refinancing news comes after a mixed stretch for TIC Solutions, with the share price currently at US$8.42 and a 90 day share price return of 10.79%. However, the year to date share price return is down 14.86% and the 1 year total shareholder return is down 22.75%. This suggests recent momentum is improving from a weaker longer term patch as investors reassess the company’s risk and growth profile.

If this repricing has you thinking about where else capital might find opportunity in infrastructure and industrial services, it could be a good time to review 34 power grid technology and infrastructure stocks

With TIC Solutions trading at US$8.42 despite a loss of US$102.872m and an implied discount to both analyst targets and intrinsic value, the key question is whether investors are overlooking value or already pricing in future growth.

Most Popular Narrative: 28.6% Undervalued

The most followed narrative on TIC Solutions compares a fair value of $11.79 to the last close at $8.42, framing the recent debt repricing against a much higher long term earnings profile and cash flow outlook.

The combination with NV5 significantly broadens Acuren's end market exposure (including faster growth verticals such as data centers and infrastructure) and enhances cross selling potential for turnkey, integrated inspection and engineering solutions, which is likely to drive higher future revenue and margin expansion.

Want to see what is sitting behind that growth pitch for TIC Solutions? The narrative focuses on faster revenue expansion, higher margins and a premium future earnings multiple that rivals high growth sectors. Curious which assumptions have to hold for that fair value to make sense?

Result: Fair Value of $11.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the TIC Solutions story also hinges on successful NV5 integration and managing higher leverage. Any stumble on synergies or cash generation could quickly challenge this growth pitch.

Find out about the key risks to this TIC Solutions narrative.

Another View: What TIC Solutions Pricing Ratios Are Signalling

While the SWS DCF model suggests TIC Solutions is trading well below an estimated future cash flow value of $34.69, the P/S ratio tells a cooler story. At 1x, TIC looks slightly expensive versus the US Professional Services average of 0.9x. It is, however, far below a peer average of 11.5x and below its own 1.3x fair ratio, which points to both optimism and risk around how sentiment might shift.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Reading this mix of pressure and potential around TIC Solutions, do you want to rely on others, or move fast and size it up yourself using the 2 key rewards and 1 important warning sign?

Looking for more investment ideas beyond TIC Solutions?

If you are serious about building a stronger portfolio, do not stop at TIC Solutions. Use the screener to uncover fresh opportunities that fit your priorities.

- Target potential turnaround stories by scanning for beaten down opportunities using the screener containing 19 high quality undiscovered gems

- Strengthen your income stream by reviewing companies highlighted in the 8 dividend fortresses

- Dial down portfolio risk by focusing on companies picked out in the 66 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com