- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

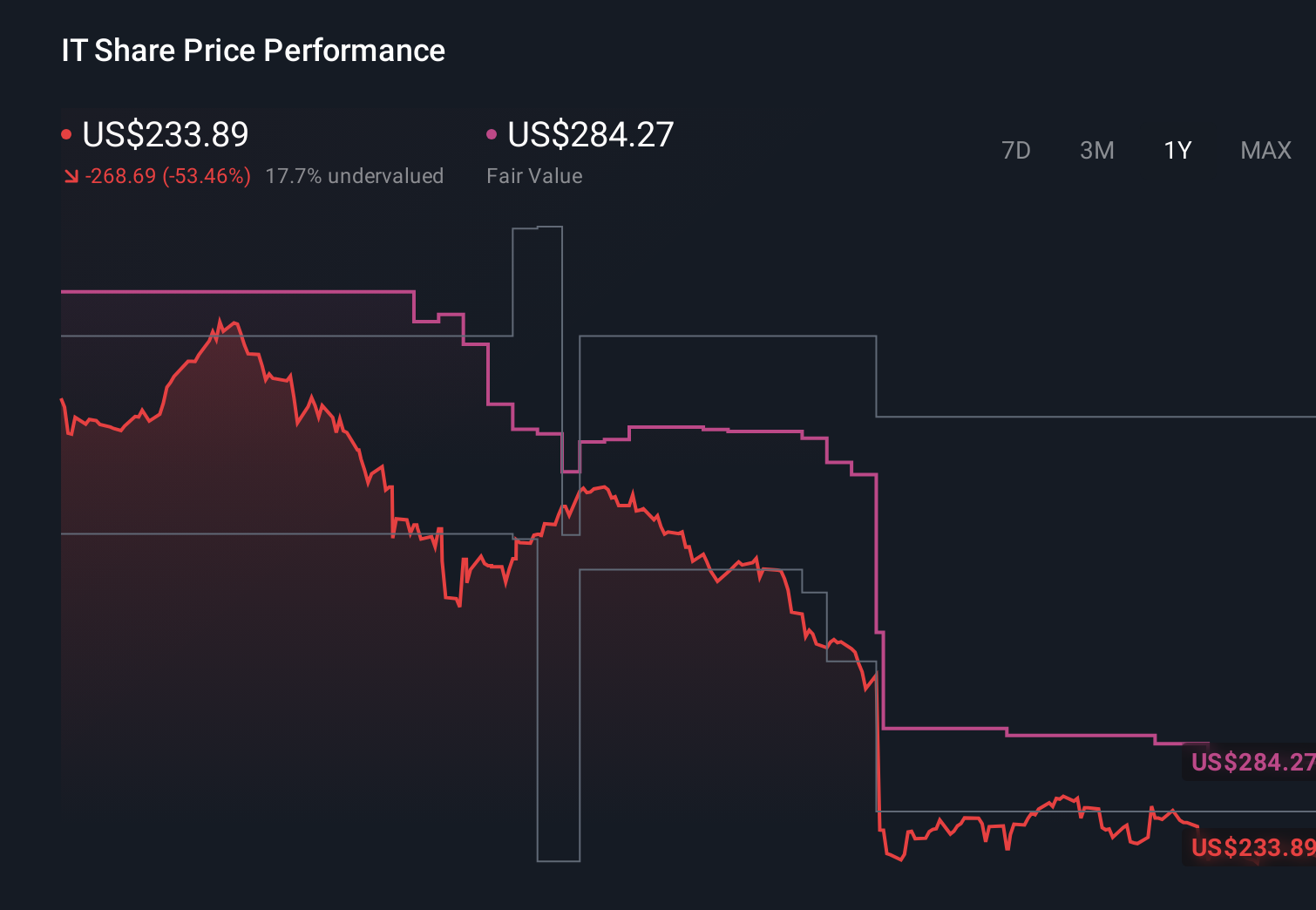

Why Gartner (IT) Is Down 14.3% After Institutional Investors Exit On Weaker Results And AI Demand Concerns

- In recent weeks, several institutional investors exited their positions in Gartner, Inc. after a series of weaker operating results and concerns about slowing demand for its research and advisory services as clients reassess technology plans amid AI adoption.

- These investor departures have coincided with broader worries that tighter financial conditions could curb discretionary IT budgets, intensifying scrutiny of Gartner’s growth priorities and business mix.

- With institutional investors citing moderating demand and priority misalignment, we’ll now examine how this shift affects Gartner’s broader investment narrative.

Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

Gartner Investment Narrative Recap

To own Gartner today, you need to believe its subscription research and advisory model can keep delivering differentiated value even as AI tools proliferate and IT budgets tighten. The key short term catalyst remains whether Gartner can stabilize contract value and subscription growth, while the biggest current risk is that moderating demand and client budget scrutiny, amplified by recent institutional selling and weaker operating results, signal a deeper reset rather than a temporary slowdown.

Against that backdrop, Gartner’s decision in late April to increase its share repurchase authorization by US$600 million, followed by more than US$507 million of Q1 2026 buybacks, stands out. This capital return is occurring alongside softer subscription trends and a sharp share price pullback, and it sharpens the question of whether management’s confidence in long term cash generation can offset investor concerns about slowing contract value growth and AI related disruption.

Yet behind this buyback story lies a less obvious risk investors should be aware of, especially if AI driven alternatives start to seriously challenge Gartner’s pricing power and...

Read the full narrative on Gartner (it's free!)

Gartner's narrative projects $7.2 billion revenue and $963.3 million earnings by 2029. This requires 3.7% yearly revenue growth and a $234.1 million earnings increase from $729.2 million today.

Uncover how Gartner's forecasts yield a $183.69 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting Gartner to reach about US$7.4 billion of revenue and US$1.1 billion of earnings by 2029, which contrasts sharply with today’s AI disruption worries and reminds you that even the most confident narratives can shift as new information comes in.

Explore 5 other fair value estimates on Gartner - why the stock might be worth just $140.00!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Gartner research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gartner research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gartner's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com