- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Does Trane Technologies' (TT) New COO and Steady Dividend Reset Its Profitability Playbook?

- In early June 2026, Trane Technologies plc appointed 25-year company veteran Donald E. Simmons as Executive Vice President and Chief Operating Officer, while its Board reaffirmed a quarterly dividend of US$1.05 per share payable on 30 September 2026, extending a dividend record that dates back to 1910.

- The combination of promoting an experienced internal leader to a broader operations role and maintaining a long-running dividend stream reinforces management’s focus on execution and capital returns for shareholders.

- Against this backdrop, we’ll explore how Simmons’ expanded COO role may influence Trane Technologies’ existing investment narrative around growth and profitability.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

Trane Technologies Investment Narrative Recap

To own Trane Technologies, you generally need to believe its commercial HVAC and refrigeration franchises can keep converting strong demand into resilient earnings, while pricing and costs stay under control. Simmons’ promotion to COO and the continued dividend reinforce operational continuity, but they do not fundamentally change the near term risk that weakness in transport refrigeration or key commercial verticals could pressure growth and margins.

The most relevant recent announcement is the Board’s decision to maintain a quarterly dividend of US$1.05 per share. For many shareholders, that long-standing dividend stream is a tangible part of the Trane story, sitting alongside the main catalyst of expected growth in commercial HVAC and services. The combination of an expanded COO role and continued capital returns may influence how investors weigh upside from execution against ongoing exposure to sector specific slowdowns.

Yet even with these positives, investors should still be aware of the risk that a sharp slowdown in data center and healthcare related HVAC demand could...

Read the full narrative on Trane Technologies (it's free!)

Trane Technologies' narrative projects $28.3 billion revenue and $4.5 billion earnings by 2029. This requires 9.5% yearly revenue growth and about a $1.6 billion earnings increase from $2.9 billion today.

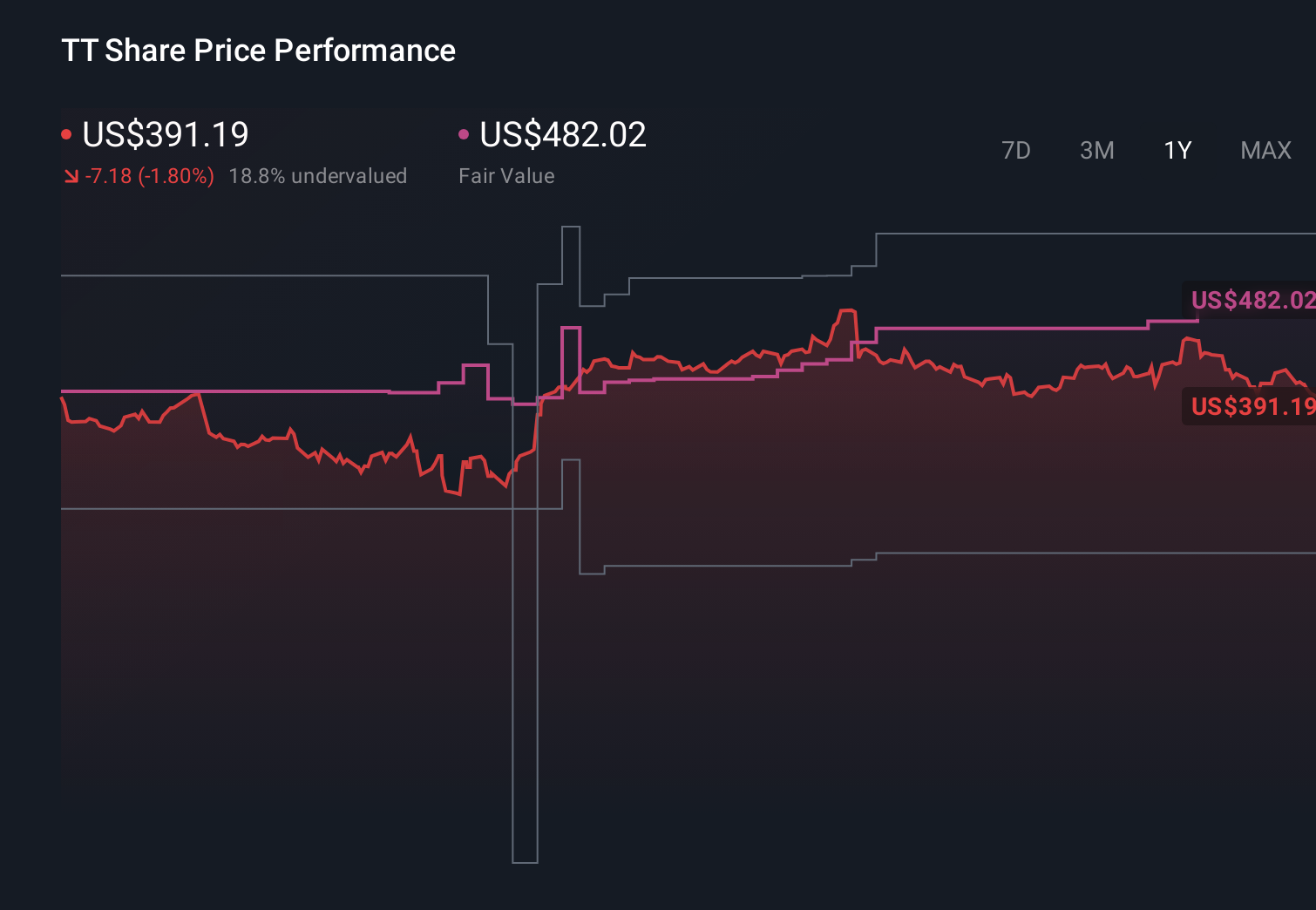

Uncover how Trane Technologies' forecasts yield a $518.30 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a more cautious view than the consensus, even before this news, assuming revenue of about US$27.5 billion and earnings around US$4.3 billion by 2029, so you may want to compare that more pessimistic path with your own expectations in light of Simmons’ new role and decide which version of Trane’s future feels more realistic.

Explore 3 other fair value estimates on Trane Technologies - why the stock might be worth 21% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Trane Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Trane Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Trane Technologies' overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com