- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

First Solar (FSLR) Stock After 79% Yearly Gain Is The Current Price Justified

- If you are wondering whether First Solar stock still offers value after a strong run, this article will walk through what the current price may be implying about the company.

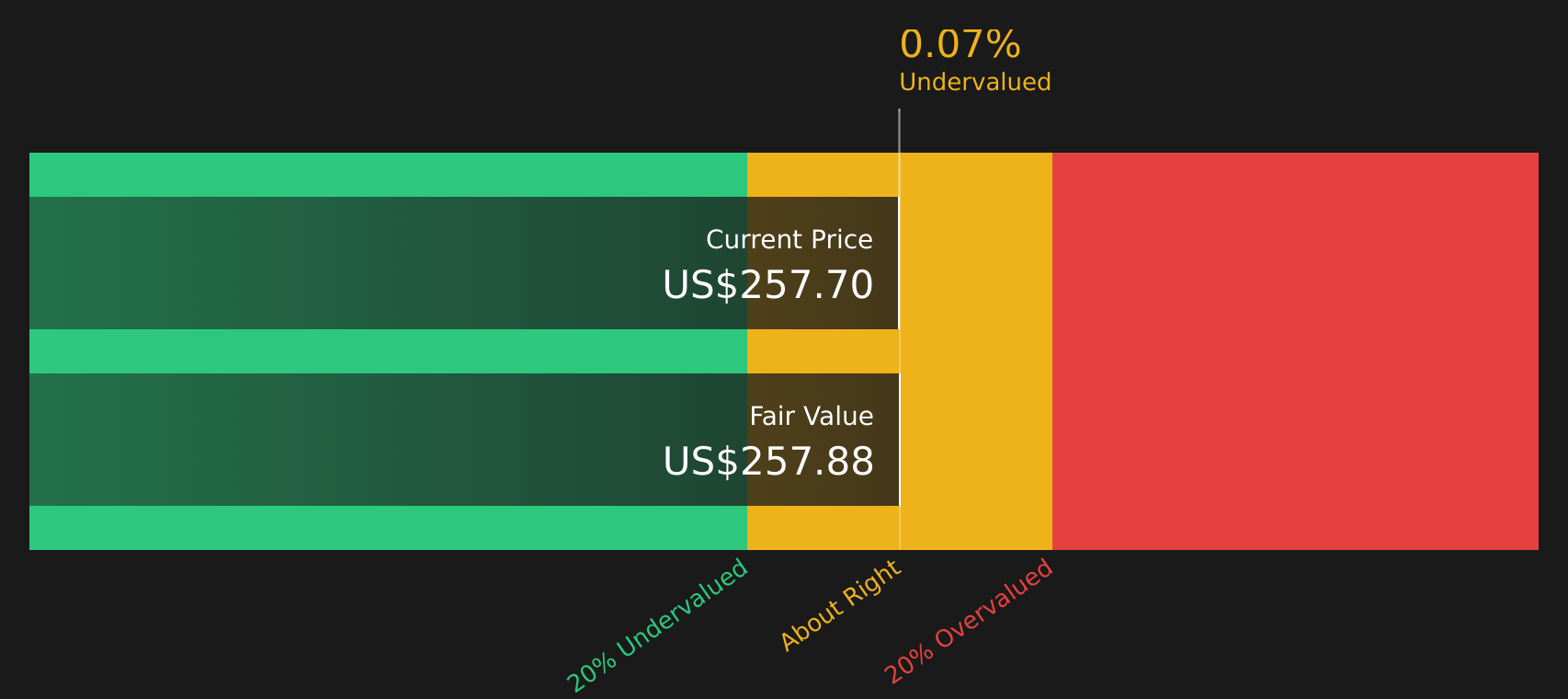

- The stock closed at US$257.70, with the share price declining 5.0% over the last week, rising 16.2% over the last month, declining 6.1% year to date, and gaining 79.4% over the past year, as well as 37.7% over three years and 204.9% over five years.

- These moves have kept First Solar in focus as investors weigh how its position in the solar industry and ongoing project pipeline align with expectations that are already reflected in the share price. Recent coverage has often centered on how policy support for renewables, capacity expansions, and long term demand for solar infrastructure could influence the outlook for the company and help explain the swings in sentiment.

- Against that backdrop, First Solar currently has a valuation score of 4 out of 6, which suggests there are several checks where the stock screens as undervalued. The next sections will unpack how different valuation approaches arrive at that view and point to an even more useful way to think about value at the end of the article.

Find out why First Solar's 79.4% return over the last year is lagging behind its peers.

Approach 1: First Solar Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow, or DCF, approach estimates what First Solar stock could be worth today by projecting future cash flows and then discounting those back to a present value using a required rate of return.

For First Solar, the model used is a 2 Stage Free Cash Flow to Equity framework built on cash flow projections. The company most recently reported trailing free cash flow of about $1.01b. Analyst based projections and subsequent extrapolations by Simply Wall St extend out to 2035, with one of the reference points being projected free cash flow of $3.13b in 2030. These annual figures, from 2026 through 2035, are discounted back to today in dollars and aggregated to arrive at an estimated intrinsic value per share.

On this basis, the DCF fair value for First Solar is calculated at $257.95 per share, very close to the recent share price of $257.70. The implied discount of roughly 0.1% suggests the stock is trading in line with the cash flow based estimate.

Result: ABOUT RIGHT

First Solar is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: First Solar Price vs Earnings

For profitable companies like First Solar, the P/E ratio is a commonly used shorthand for how much investors are paying for each dollar of earnings. It lets you compare what the market is willing to pay for this company against others with similar business models.

What counts as a “normal” P/E depends on how fast earnings are expected to grow and how risky those earnings are seen to be. Higher expected growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually points to a lower one.

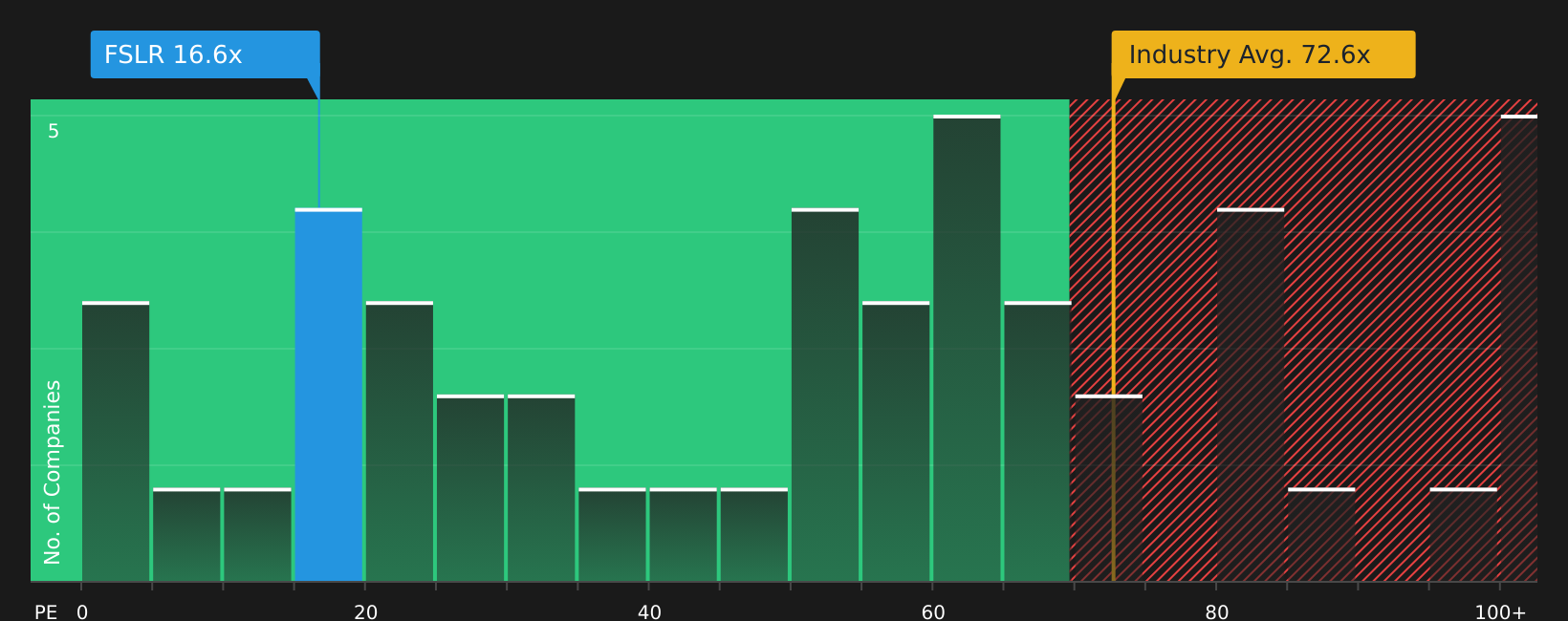

First Solar currently trades on a P/E of 16.63x. This is well below the Semiconductor industry average P/E of 68.29x and the broader peer average of 119.94x. Simply Wall St’s Fair Ratio for First Solar is 41.93x, which is a proprietary estimate of what the P/E might be based on factors such as earnings growth, industry, profit margin, market cap and risk profile.

The Fair Ratio can be more informative than a simple comparison with industry or peers because it adjusts for those company specific factors. With the actual P/E meaningfully below the Fair Ratio, the multiple-based view points to the stock screening as undervalued on earnings.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your First Solar Narrative

Earlier the article mentioned that there is an even better way to understand valuation. This is where Narratives come in for First Solar stock, giving you a simple story that ties your view of the business to a set of numbers like future revenue, earnings, margins and an assumed fair value.

On Simply Wall St’s Community page, a Narrative is your own clear explanation of what you think is happening at First Solar, linked directly to a financial forecast and a fair value estimate. This allows you to compare that fair value to today’s share price and decide whether the stock looks expensive or cheap against your assumptions rather than anyone else’s.

Narratives are updated automatically when new information such as earnings releases, tariff news or guidance changes is added to the platform. This means your story and numbers stay aligned without you needing to rebuild a model every time fresh data appears.

For example, one First Solar Narrative on the platform takes a more cautious view with a fair value around US$167.73, while another more optimistic Narrative sees fair value closer to US$313.00. Both are based on different expectations for revenue growth, profit margins and future P/E, giving you a clear range of perspectives to compare with your own.

For First Solar, however, we will make it really easy for you with previews of two leading First Solar Narratives:

Fair value in this bullish Narrative is set at US$313.00 per share.

At the recent share price of US$257.70, this view implies First Solar is about 17.7% below that fair value anchor using the formula ((fair_value last_close) / fair_value).

The Narrative assumes revenue growth of 18.80% a year.

- Highlights U.S. manufacturing expansion, Section 45X credits, and a non-Chinese supply chain as key supports for margins and pricing power.

- Includes faster growth and higher profitability, with bullish analysts modeling revenue of US$8.8b and earnings of US$4.2b by 2029.

- States that if those earnings are achieved, First Solar could justify trading on an 11.0x P/E in 2029, which is below the current U.S. Semiconductor industry P/E reference of 47.2x used in the Narrative.

Fair value in this more cautious Narrative is set at US$243.59 per share.

At the recent share price of US$257.70, this view implies First Solar is about 5.8% above that fair value anchor using the same ((fair_value last_close) / fair_value) formula.

This Narrative assumes revenue growth of 7.18% a year.

- Emphasizes tariff and policy uncertainty, potential shifts in long-term solar demand, and competition from low-cost Asian manufacturers as key risks.

- Builds a base case where revenue reaches about US$6.7b and earnings reach US$3.1b by 2029, with profit margins improving but from a lower growth base.

- Concludes that to support its fair value, First Solar would trade on an 11.7x P/E in 2029 and that, relative to the current share price in that Narrative, analysts see market expectations as too optimistic.

If you want to see how other investors are framing similar bull and bear stories around the same numbers, it is worth scanning the wider set of community views before making your own call on First Solar stock. See what the community is saying about First Solar

Do you think there's more to the story for First Solar? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com