- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Republic Services (RSG) Stock Valuation Check After Recent Weak Momentum And Long Term Gains

Recent share performance and business scale

Republic Services (RSG) has moved in a tight range recently, with the stock up roughly 0.9% over the past day and close to flat over the past month.

Over the past 3 months, the share price is down about 6.3%, and the 1 year total return has declined 15.5%. Over the same period, the company reports annual revenue of about US$16.7b and net income of roughly US$2.2b.

See our latest analysis for Republic Services.

Putting this in context, Republic Services’ short term share price momentum has softened, while the 3 year and 5 year total shareholder returns of 49.2% and 110.1% highlight a much stronger longer term record.

If you want to see what else is moving in essential infrastructure, this is a good moment to scan 34 power grid technology and infrastructure stocks

With Republic Services posting revenue of about US$16.7b and net income of roughly US$2.2b, alongside softer recent returns but stronger multi year gains, the key question is whether the current share price offers value or whether the market is already pricing in future growth.

Most Popular Narrative: 13.8% Undervalued

Republic Services last closed at $209.91, while the most followed narrative sets fair value at $243.58, using a 7.22% discount rate to frame that gap.

Sustainability efforts such as the development of Polymer Centers and the Blue Polymers joint venture could drive future revenue growth by enhancing plastic circularity and decarbonization. These operations are expected to contribute to earnings starting in the second half of 2025.

Want to understand why a waste and recycling business commands a premium valuation narrative? Typically that hinges on measured revenue growth, improving margins, and a richer earnings multiple baked into the model.

Result: Fair Value of $243.58 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative can come under pressure if softer construction and manufacturing volumes persist, or if the planned US$1b acquisition program proves hard to integrate.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another angle on valuation: pricing versus peers

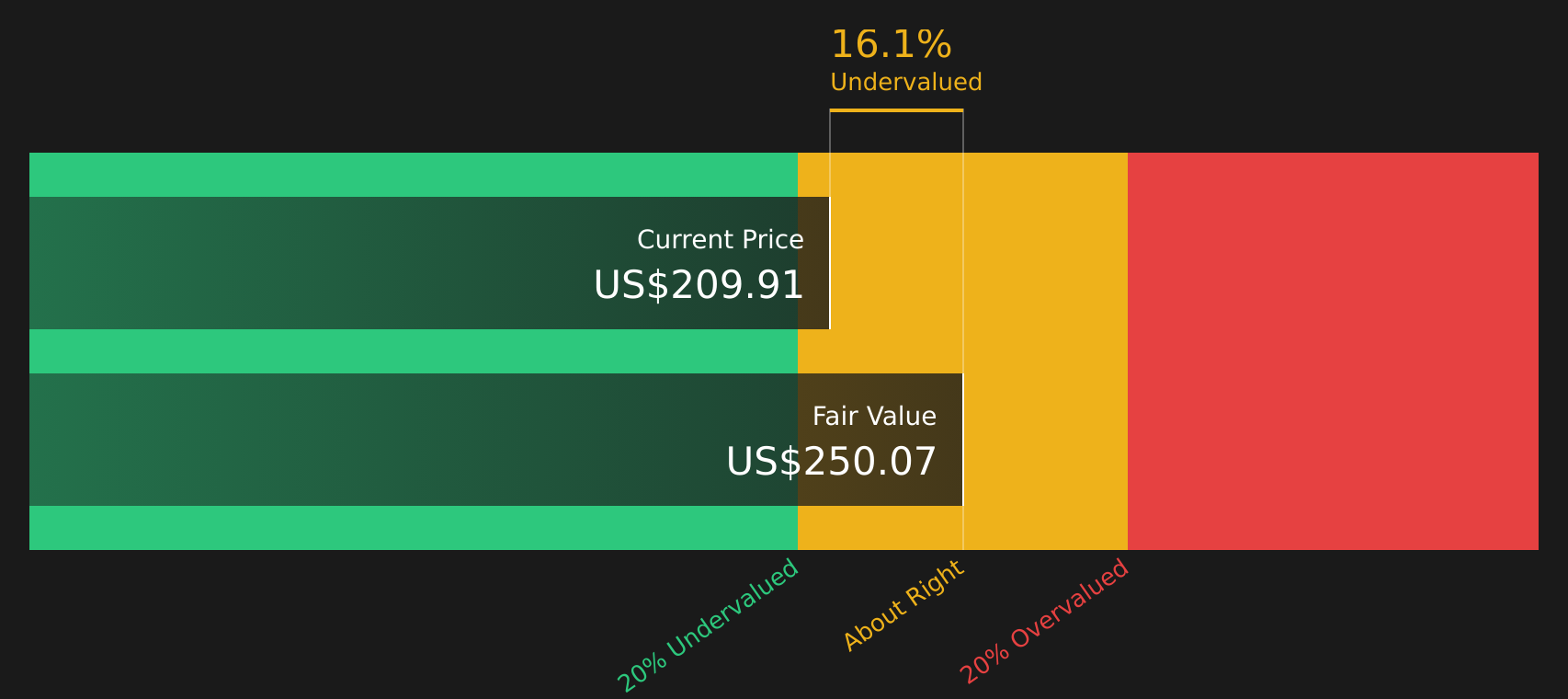

While the SWS DCF model suggests Republic Services is trading about 16.1% below fair value at $209.91 versus an estimated $250.07, its P/E of 29.8x is higher than both the US Commercial Services industry at 21.2x and its own fair ratio of 22.6x. This raises the question of whether the market is offering a discount on cash flows or charging a premium on earnings.

Look into how the SWS DCF model arrives at its fair value.

Next Steps

If this mix of optimism and concern feels familiar, treat it as a prompt to look closer at the data and timing, and shape your own view with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop your research here. Broaden your watchlist with a few targeted screens that surface opportunities you might otherwise miss.

- Target consistency by checking out companies highlighted in the 71 resilient stocks with low risk scores that aim to keep volatility and risk scores in check.

- Spot potential mispricings by scanning the 44 high quality undervalued stocks where solid fundamentals and attractive valuations are the focus.

- Get ahead of the crowd by reviewing the screener containing 20 high quality undiscovered gems and see which under followed stocks have financial profiles that stand out.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com