- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Manhattan Associates (MANH) Stock After Supply Chain Reassessment Is The Pullback Enough

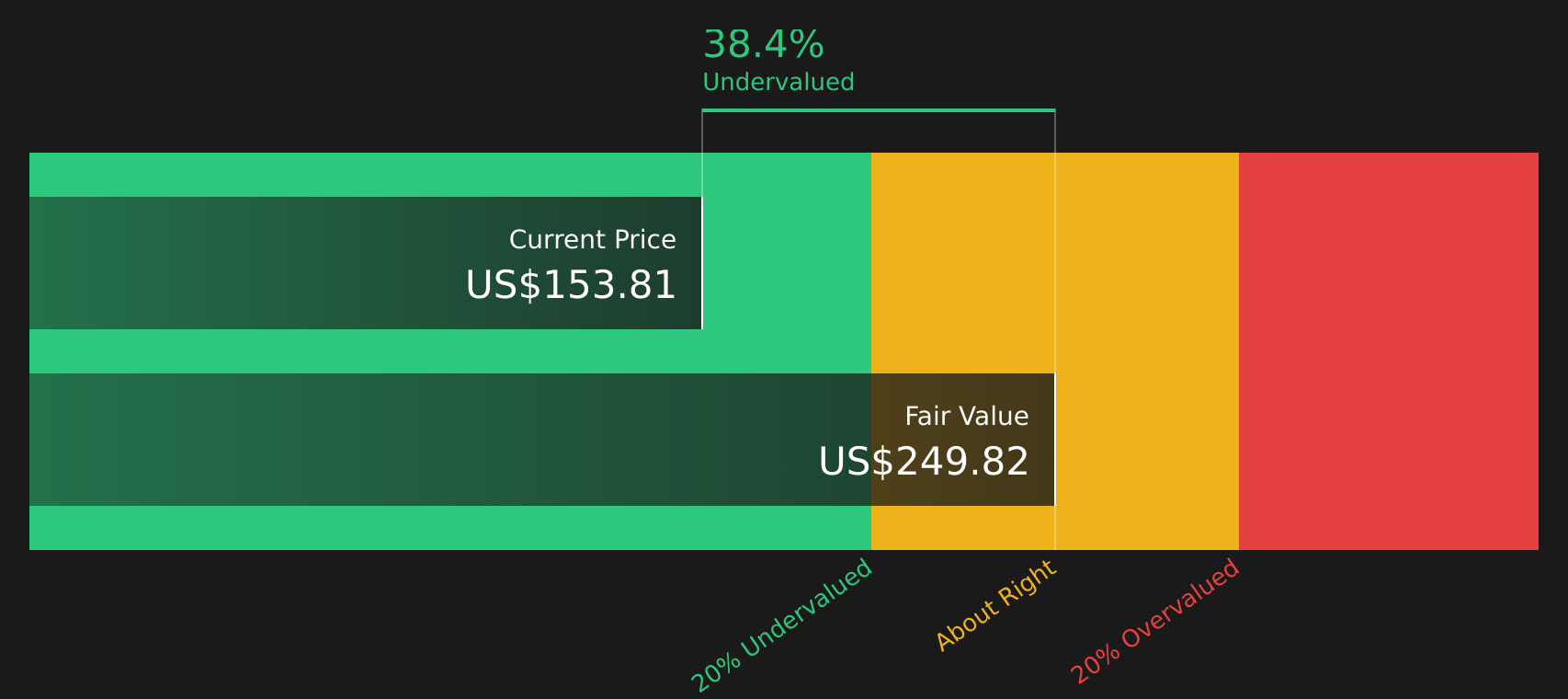

- For investors wondering whether Manhattan Associates at US$140.29 is starting to look appealing or still feels expensive, this article focuses squarely on what the current price might imply about value.

- The stock has been volatile recently, with a share price that rose about 4.0% over the last month but is still down about 16.1% year to date and about 27.3% over the past year.

- Recent headlines have focused on how supply chain software providers are being reassessed by investors as expectations adjust across the software sector. For Manhattan Associates, that has sparked fresh attention on how much of the past enthusiasm is already reflected in the current share price and what risks the market may now be pricing in.

- Manhattan Associates currently has a valuation score of 4 out of 6. The rest of this article will unpack what different valuation methods say about that score, before finishing with a framework that can help you judge whether those numbers really line up with your own view of the stock.

Find out why Manhattan Associates's -27.3% return over the last year is lagging behind its peers.

Approach 1: Manhattan Associates Discounted Cash Flow (DCF) Analysis

A DCF model estimates what a stock could be worth by projecting the cash the company may generate in the future and discounting those cash flows back to today using a required rate of return.

For Manhattan Associates, the model uses a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $386.8 million. Analyst forecasts and subsequent extrapolations point to projected free cash flow of $723.4 million in 2030, with a full set of ten year projections running from 2026 through 2035, all in dollars.

When these projected cash flows are discounted back, the model arrives at an estimated intrinsic value of $234.60 per share. Compared with the current share price of $140.29, this implies the stock is trading at a 40.2% discount to that DCF estimate, which the model interprets as undervalued.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Manhattan Associates is undervalued by 40.2%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

Approach 2: Manhattan Associates Price vs Earnings

For profitable companies, the P/E ratio is a useful shorthand for how many dollars investors are currently paying for each dollar of earnings, which makes it a common check on whether a stock looks expensive or reasonable.

What counts as a normal or fair P/E ratio usually reflects how the market views a company’s growth potential and risk profile. Higher expected growth or lower perceived risk can justify a higher P/E, while lower growth or higher risk tends to point to a lower multiple.

Manhattan Associates currently trades on a P/E of 38.31x. That sits below the average of its selected peer group at 40.53x and above the broader Software industry average P/E of 27.86x.

Simply Wall St’s Fair Ratio is a proprietary estimate of what P/E might make sense for Manhattan Associates, given factors such as earnings growth, profit margins, market cap, risks and its Software industry membership. This tailored yardstick can be more informative than a simple comparison with peers or the industry, because it aims to line up the multiple with the company’s own fundamentals rather than broad group averages.

The Fair Ratio for Manhattan Associates is 26.90x, which is below the current P/E of 38.31x. This suggests the stock screens as overvalued on this measure.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Manhattan Associates Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so here is Narratives, a simple tool on Simply Wall St's Community page that lets you connect your view of Manhattan Associates' story to explicit forecasts for revenue, earnings and margins. These then roll up into a Fair Value you can compare with the current price to decide whether the stock looks attractive or stretched. The tool automatically refreshes as new news or earnings arrive. One investor might back a higher Fair Value of around US$235 based on expectations for stronger AI driven supply chain adoption and buybacks. Another might lean toward a lower Fair Value near US$160 if more cautious about macro risks and cloud transitions. Both perspectives can sit side by side so you can see which story and set of numbers you find more reasonable.

Do you think there's more to the story for Manhattan Associates? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com