- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

What Citigroup (C)'s US$3.15 Billion Note Redemption Means For Shareholders

- In early June 2026, Citigroup Inc. redeemed in full US$2.75 billion of its 1.462% fixed/floating rate notes and US$400 million of its floating rate notes due 2027, paying investors par plus accrued interest as part of its liability management program to streamline funding and capital structure.

- This move, alongside management’s emphasis on cost efficiency, AI-driven automation and a shift from repair to growth, highlights how Citi is reshaping its balance sheet and operations to support a more focused, higher-return business mix.

- Next, we’ll examine how Citi’s early redemption of US$3.15 billion in notes fits into and potentially strengthens its existing investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Citigroup Investment Narrative Recap

To own Citi today, you need to believe the bank can convert its recent operational overhaul and capital discipline into steadier earnings and better returns, despite ongoing regulatory and competitive pressures. The US$3.15 billion early note redemption is incremental to this story rather than a game changer: it reinforces the focus on balance sheet efficiency, but does not materially alter the near term catalysts around execution on cost cuts and AI-driven productivity, or the key risk of lingering regulatory and transformation costs.

The announcement that Citi hit a 52 week high after reporting its strongest quarterly net income in a decade and repurchasing US$6.3 billion of stock is, in my view, the clearest companion to the note redemption. Both moves point to a management team leaning into capital optimization and a “repair to growth” mindset, which ties directly into the current catalyst of improving returns, while keeping the spotlight on whether elevated transformation spending can be contained.

Yet beneath the progress, investors still need to watch how rising transformation and compliance costs could suddenly change the story if...

Read the full narrative on Citigroup (it's free!)

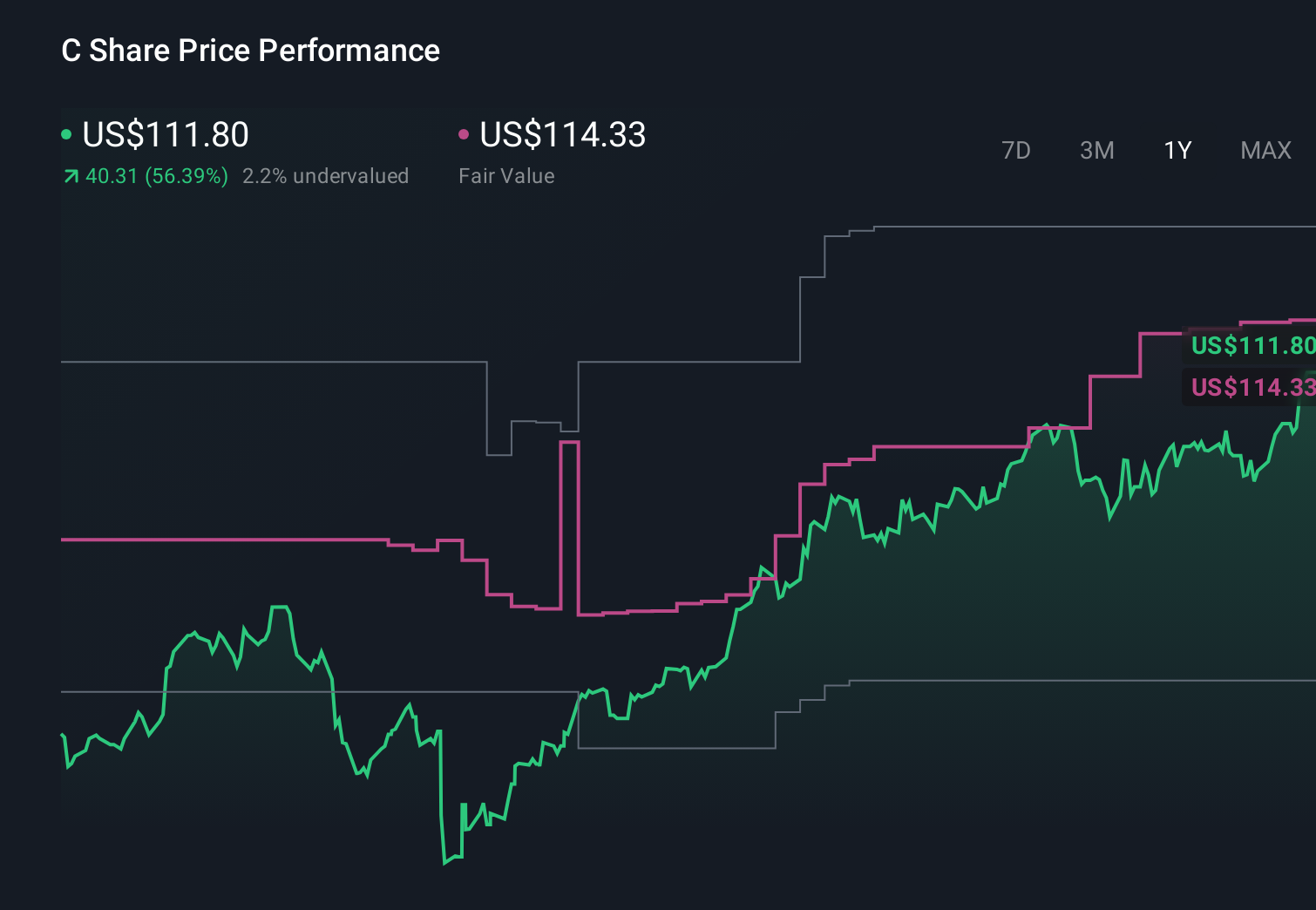

Citigroup's narrative projects $102.4 billion revenue and $21.7 billion earnings by 2029. This requires 9.2% yearly revenue growth and a $7.0 billion earnings increase from $14.7 billion today.

Uncover how Citigroup's forecasts yield a $146.93 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts tell a much harsher story, assuming revenues near US$96.2 billion and earnings of about US$18.9 billion by 2029, so if you are focused on Citi’s recent debt redemption and cost push, it is worth asking whether those more pessimistic forecasts on margins and buybacks still hold after this news or if the gap in expectations could actually widen from here.

Explore 10 other fair value estimates on Citigroup - why the stock might be worth as much as 75% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Citigroup research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Citigroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Citigroup's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com