- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

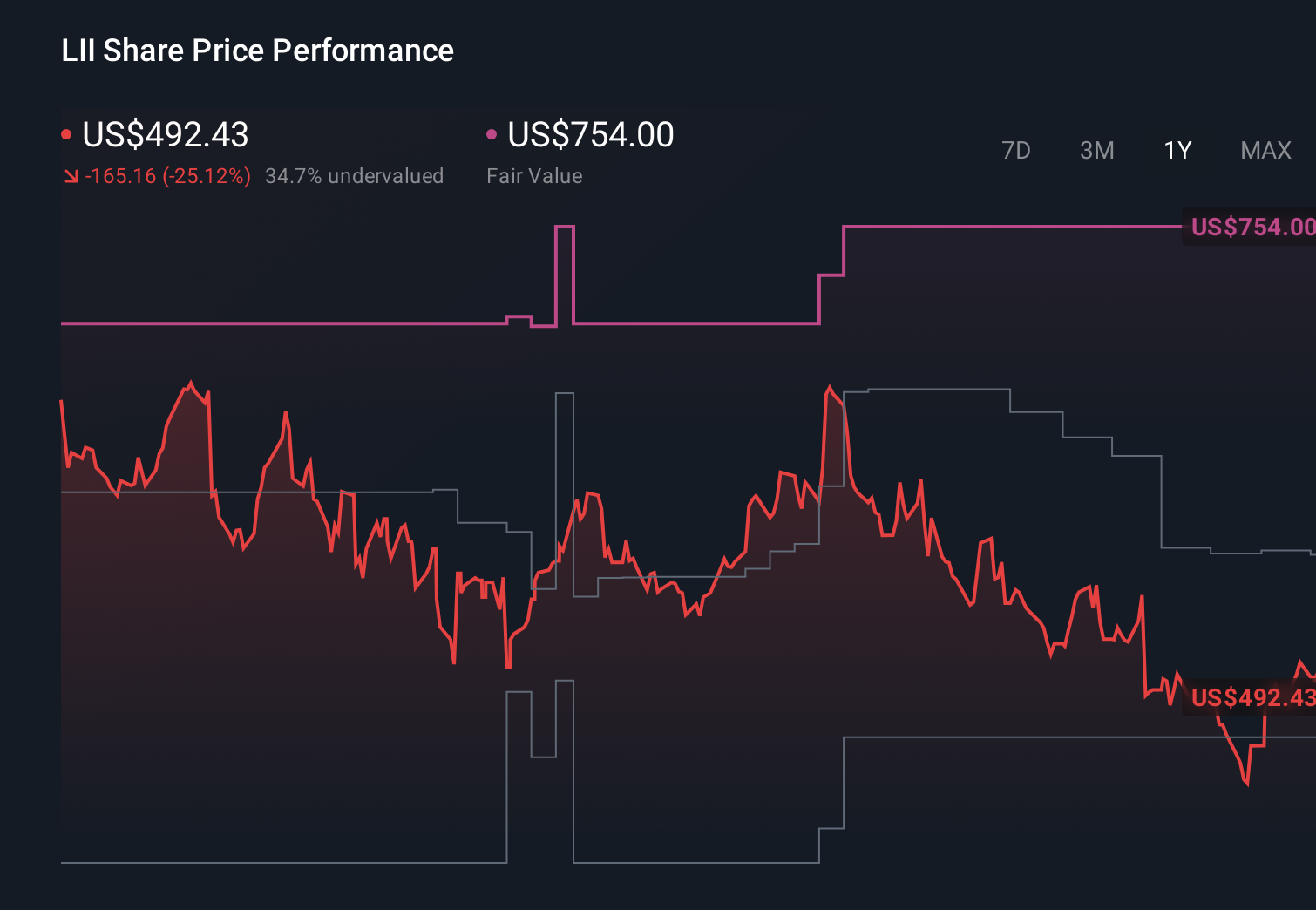

Does Lennox International's (LII) Governance Stability Reinforce Its Underlying Business Quality Story?

- Lennox International recently saw board member Sivasankaran Somasundaram resign in May 2026 and is scheduled to present at the 46th Annual William Blair Growth Stock Conference on June 3, 2026, in Chicago.

- The routine nature of the board change, combined with strong third‑party financial scoring and valuation metrics, has sharpened investor focus on Lennox’s underlying business quality rather than governance concerns.

- Now, we’ll examine how the strong third‑party financial assessment and routine board change affect Lennox International’s existing investment narrative.

The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

Lennox International Investment Narrative Recap

To own Lennox International, you need to believe in its ability to convert a premium HVAC brand, dealer relationships, and product innovation into steady earnings, despite housing softness, refrigerant uncertainty, and cost pressures. The recent board resignation and William Blair conference appearance do not materially change the key near term catalyst, which is execution on product and pricing initiatives, or the biggest risk, which remains potential demand weakness in core North American residential markets.

The most relevant recent announcement here is Lennox’s latest 2026 guidance, which calls for revenue growth supported partly by acquisitions and continued earnings expansion. That backdrop helps frame the board change and conference participation as routine corporate events occurring alongside ongoing operational execution, rather than as new drivers of the story, while the core questions for investors still center on demand resilience, pricing power, and inventory risk.

But even with this constructive setup, investors should be aware of how emerging energy efficient competitors could pressure Lennox’s pricing power and long term margins if ...

Read the full narrative on Lennox International (it's free!)

Lennox International's narrative projects $6.2 billion revenue and $1.1 billion earnings by 2028.

Uncover how Lennox International's forecasts yield a $555.69 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts take a much more cautious view than consensus, even before this news, assuming revenue of about US$5.9 billion and earnings near US$966.6 million by 2029, and worrying that faster moving energy efficient rivals could erode margins despite Lennox’s focus on partnerships and conferences.

Explore 3 other fair value estimates on Lennox International - why the stock might be worth as much as 23% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Lennox International research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Lennox International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lennox International's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com