- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Custom Truck One Source (CTOS) Valuation After Sourcewell Contract Win And Upbeat Earnings Guidance

Custom Truck One Source (CTOS) is back on investors’ radar after two key developments: a cooperative purchasing contract award from Sourcewell and stronger than expected quarterly results paired with a raised full year outlook.

See our latest analysis for Custom Truck One Source.

Despite the recent 1-day share price return slipping 3.2% to close at US$9.68, Custom Truck One Source has built strong momentum, with a 90-day share price return of 51.01% and a 1-year total shareholder return of 107.73% reflecting how investors are reassessing its growth potential and risk profile after the Sourcewell contract and upbeat guidance.

If you are looking beyond this equipment rental and infrastructure story, it is a good time to see what else is moving across 33 power grid technology and infrastructure stocks

With the stock up sharply over the past year and trading at US$9.68 against an analyst price target of US$11.50, and with analysts viewing it as above their fair value estimates, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 26% Overvalued

Custom Truck One Source's most followed narrative pegs fair value at $7.67, which sits below the last close of $9.68 and underpins an overvaluation view built on detailed growth and margin assumptions.

Analysts are assuming Custom Truck One Source's revenue will grow by 4.3% annually over the next 3 years.

Analysts assume that profit margins will increase from 1.6% loss today to 1.7% profit in 3 years time.

Want to see what sits behind that shift from losses to profits and the valuation that comes with it? The narrative leans heavily on steady top line expansion, a gradual margin swing into positive territory, and a future earnings multiple more commonly linked to faster growth stories. The full set of assumptions shows exactly how those pieces combine into the current fair value call.

Result: Fair Value of $7.67 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points to watch, including relatively high leverage and softer TES backlog trends that could challenge the current fair value story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Way To Look At Valuation

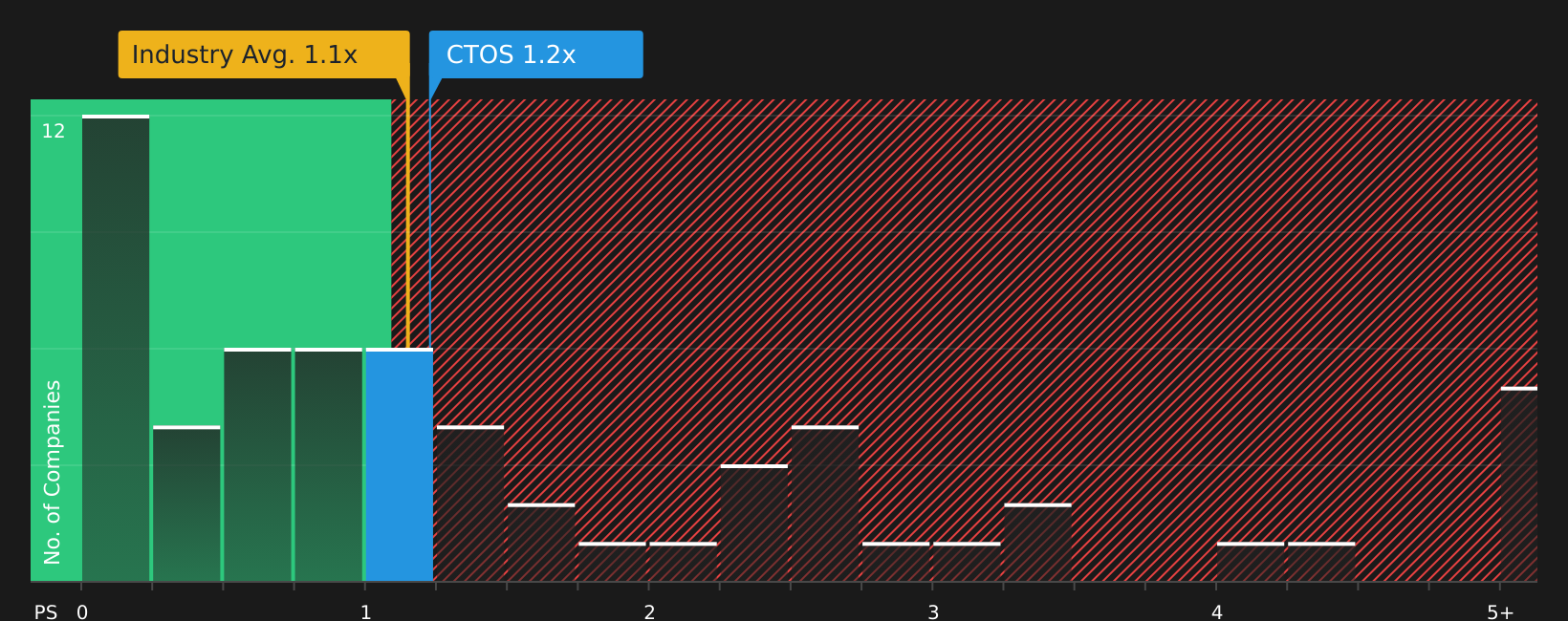

Analysts see Custom Truck One Source as overvalued at $9.68 versus their $7.67 fair value. However, the stock trades on a P/S of 1.1x, which is in line with the US Trade Distributors industry at 1.1x and slightly below its own 1.2x fair ratio. This points to a more balanced picture. Which signal do you put more weight on?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between overvaluation concerns and more neutral P/S signals, it makes sense to move quickly and check the underlying facts yourself. To see what investors are optimistic about and how those positives stack up against the risks, review the 3 key rewards

Looking for more investment ideas?

If you stop with just one stock, you could miss other opportunities that suit your goals, so keep scanning for ideas that fit how you like to invest.

- Target potential mispricings by checking stocks highlighted in the 49 high quality undervalued stocks for attractive quality at reasonable prices.

- Strengthen your income stream by reviewing companies in the 9 dividend fortresses that pair higher yields with a focus on resilience.

- Protect your downside first by focusing on companies inside the 64 resilient stocks with low risk scores that score well on financial strength and risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com