- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How IQVIA’s €950 Million Debt Refinancing and 2026 Outlook Update Will Impact IQVIA Holdings (IQV) Investors

- IQVIA Holdings’ subsidiary recently announced a €950 million senior notes offering due 2033 to refinance existing debt and cover related fees, with the notes privately placed under Rule 144A and Regulation S.

- Alongside this refinancing move, IQVIA raised its adjusted earnings outlook for 2026, underlining management’s confidence in the company’s underlying operations and balance sheet flexibility.

- Next, we’ll assess how IQVIA’s €950 million debt refinancing reshapes its investment narrative, particularly around leverage, margins, and capital flexibility.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

IQVIA Holdings Investment Narrative Recap

To own IQVIA, you need to believe in steady demand for outsourced clinical research and data-driven services, supported by AI and real-world evidence platforms. The €950 million senior notes refinancing looks incremental to that thesis, with limited impact on the near term catalyst around execution on AI initiatives, while the biggest risk remains high leverage and the potential for debt costs to eat into earnings if conditions become less favorable.

The most relevant recent announcement here is IQVIA’s higher adjusted earnings outlook for 2026, which sits alongside the new notes issue. Together, they put a spotlight on how well the company can balance growth investments, AI rollouts, and buybacks against its sizeable debt load, a balance that is central to both the upside catalysts and the key financial risk in the story.

But beneath the refinancing headlines, investors should be aware of how IQVIA’s high leverage could...

Read the full narrative on IQVIA Holdings (it's free!)

IQVIA Holdings' narrative projects $19.7 billion revenue and $2.0 billion earnings by 2029. This requires 5.8% yearly revenue growth and about a $0.6 billion earnings increase from $1.4 billion.

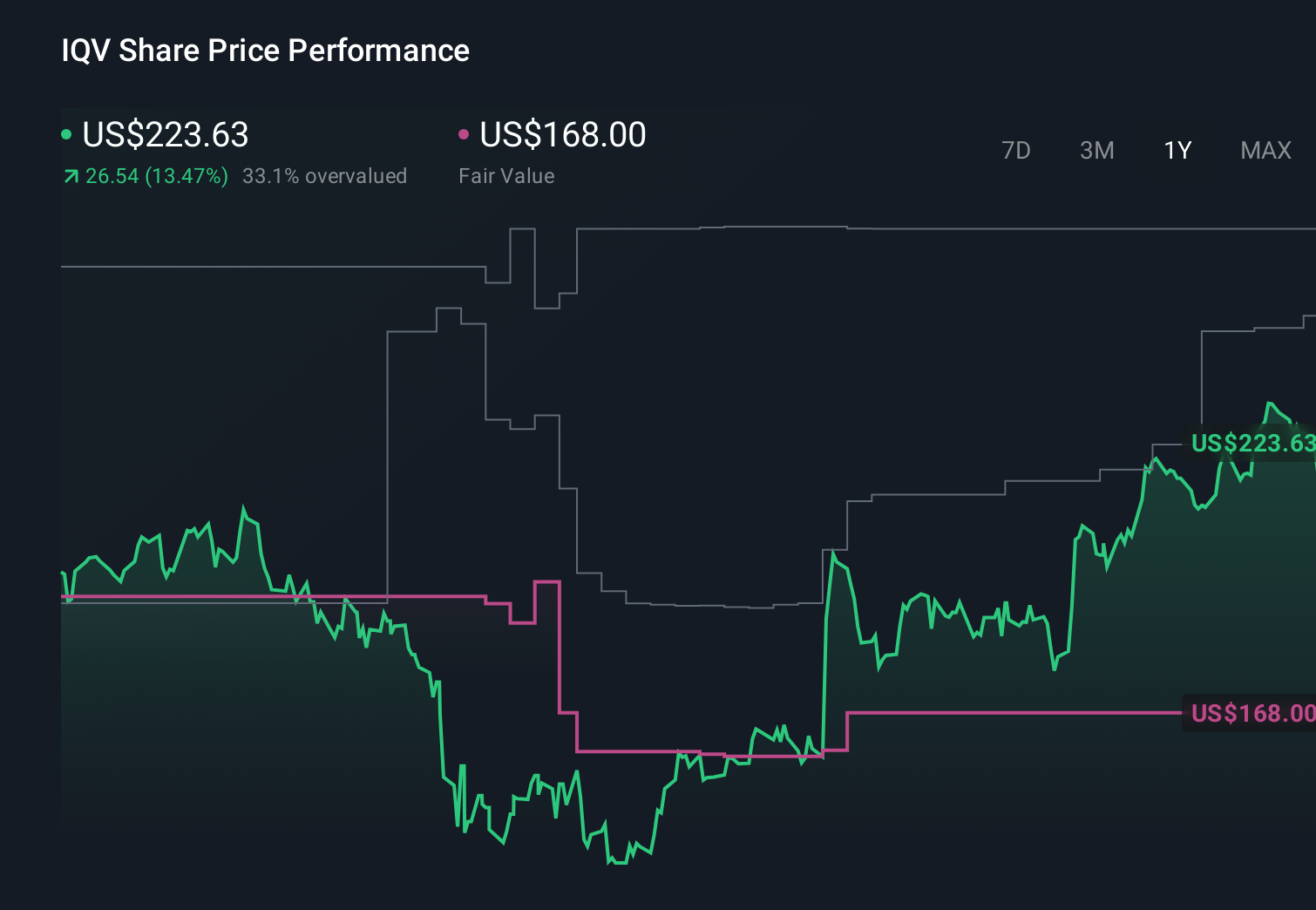

Uncover how IQVIA Holdings' forecasts yield a $228.60 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming only about 5.4 percent annual revenue growth to roughly US$19.5 billion by 2029, and the new €950 million refinancing could either reinforce those worries about leverage or soften them if it improves costs, so it is worth comparing this more pessimistic view on debt constraints with the backlog driven growth story before deciding which narrative you find more convincing.

Explore 4 other fair value estimates on IQVIA Holdings - why the stock might be worth just $228.60!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your IQVIA Holdings research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free IQVIA Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate IQVIA Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com