- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Do Everus Construction Group’s New IT and HR Chiefs Reveal a Sharper Strategic Focus for ECG?

- Everus Construction Group, Inc. recently elevated Jason A. Behring to vice president and chief information officer and Britney A. Hendricks to vice president and chief human resources officer, formalizing leadership in IT and HR that they have built over years with the company.

- These internal promotions underscore how Everus is consolidating its core technology and people functions as it continues operating as a stand-alone public construction services company.

- Next, we will examine how Everus’ leadership changes in technology and human resources may influence its existing investment narrative and outlook.

Find 47 companies with promising cash flow potential yet trading below their fair value.

Everus Construction Group Investment Narrative Recap

To own Everus today, you need to believe its exposure to power infrastructure, data centers and complex commercial projects can support durable earnings, even as sector sentiment remains volatile. The key near term catalyst is converting its signed backlog into revenue without eroding margins, while the biggest risk is a cooling in large scale build programs or order intake. The latest IT and HR promotions mainly reinforce organizational depth and do not materially change these immediate drivers.

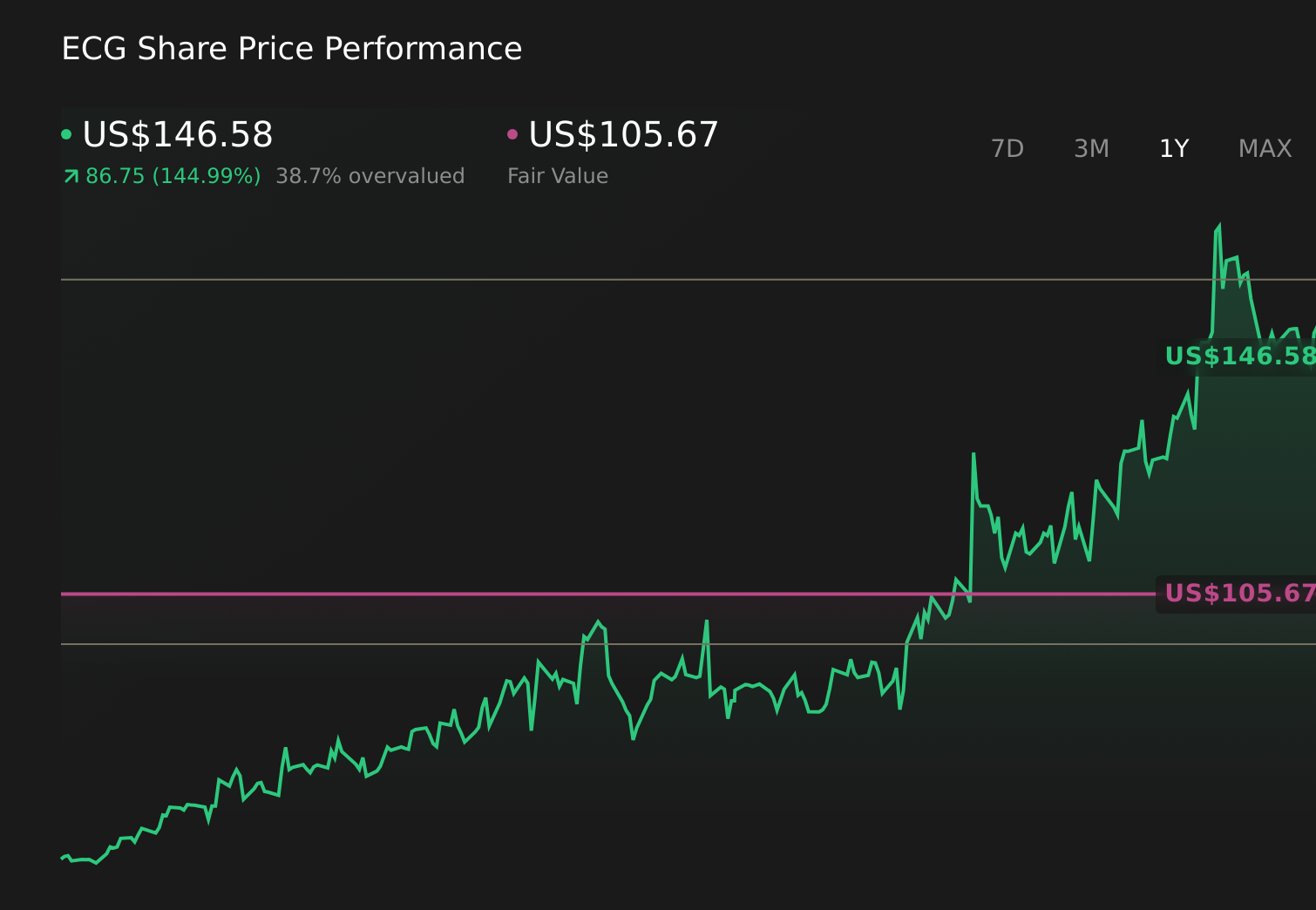

Among recent developments, the share price’s strong run to about US$150.76, alongside a 150% one year total shareholder return, stands out as most relevant. That performance, versus a consensus fair value near US$105.67, frames how investors weigh execution strengths and the upgraded 2026 revenue guidance of US$4.3 billion to US$4.4 billion against the risk of paying up if data center and infrastructure demand, or margins, prove less durable than expected.

Yet beneath the momentum, investors should be aware of how quickly sentiment could shift if large project demand or backlog trends begin to...

Read the full narrative on Everus Construction Group (it's free!)

Everus Construction Group's narrative projects $4.3 billion revenue and $220.5 million earnings by 2028. This requires 7.2% yearly revenue growth and about a $39.5 million earnings increase from $181.0 million today.

Uncover how Everus Construction Group's forecasts yield a $105.67 fair value, a 30% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting Everus to reach about US$5.3 billion in revenue and nearly US$297 million in earnings, which is far more bullish than consensus, and highlights how views on whether investments in areas like prefabrication will pay off can differ sharply and may need revisiting after leadership changes in IT and HR.

Explore 4 other fair value estimates on Everus Construction Group - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Everus Construction Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Everus Construction Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Everus Construction Group's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com