- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At TriMas (TRS) Valuation After Recent Share Price Momentum

Recent performance context

TriMas (TRS) has drawn fresh attention after a solid run, with the stock up about 13% over the past month and roughly 47% over the past 3 months, placing recent returns in clear focus for investors.

See our latest analysis for TriMas.

At a latest share price of $40.93, TriMas has paired a 13.4% 1 month share price return with a 55.9% 1 year total shareholder return. This suggests recent momentum has been building rather than fading as investors reassess growth prospects and risk.

If this kind of move has you thinking about what else might be setting up for a strong run, it could be worth scanning 20 top founder-led companies

With TriMas trading at $40.93 and management estimating an intrinsic value that is around 19% higher, along with analysts setting a $45.00 target, you have to ask: is there still upside here or is the market already pricing in future growth?

Most Popular Narrative: 1% Undervalued

TriMas is trading at $40.93 against a most-followed fair value estimate of $41.50, so the narrative implies only a modest valuation gap right now, built on specific views of growth, margins and risk.

New leadership with significant packaging industry expertise is implementing operational standardization and integration across global manufacturing sites and recent acquisitions. This push is expected to drive margin expansion and improved operating leverage, positively impacting net margins and earnings potential.

Want to see what that kind of margin story actually looks like on paper? The narrative ties revenue, earnings and valuation multiples together in a way that is anything but cautious. The full set of assumptions shows how a relatively small gap to fair value can still rest on very punchy profit and cash flow expectations.

Result: Fair Value of $41.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upbeat story can unravel quickly if packaging integration issues linger or if weaker demand across aerospace and industrial customers hits orders harder than expected.

Find out about the key risks to this TriMas narrative.

Another view on valuation

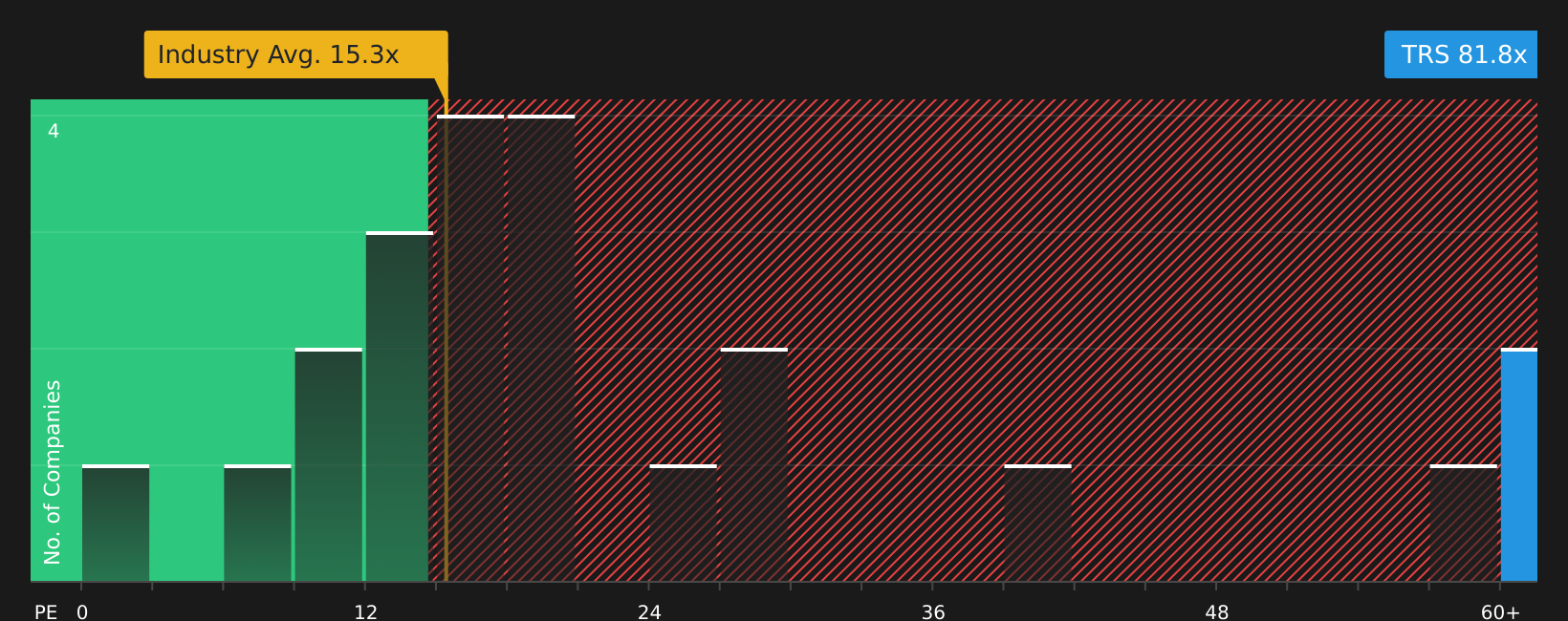

While the narrative points to a fair value of $41.50, the current P/E of 78.8x stands far above the global packaging industry at 15.2x and the peer average of 17.5x, even though the fair ratio model suggests 104.1x. That spread raises a simple question: is this a cushion or a cliff for new buyers?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With all this in mind, are you feeling cautious or optimistic about TriMas? Consider your options while the stock is on your radar and weigh both sides of the story with 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If TriMas has your attention, do not stop here. The real edge often comes from lining up a few strong ideas, not just one headline stock.

- Target quality at a discount by scanning 46 high quality undervalued stocks that combine appealing valuations with solid fundamentals.

- Lock in potential income streams by reviewing 10 dividend fortresses offering higher yields with a focus on resilience.

- Protect your downside first by concentrating on 62 resilient stocks with low risk scores built around stronger balance sheets and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com