- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing NCR Atleos (NATL) Valuation After Colombia Cashzone Expansion With Bancoomeva

NCR Atleos (NATL) is expanding its Cashzone ATM network into Colombia through a collaboration with Bancoomeva, highlighting an effort to widen access to cash and financial services across Latin America.

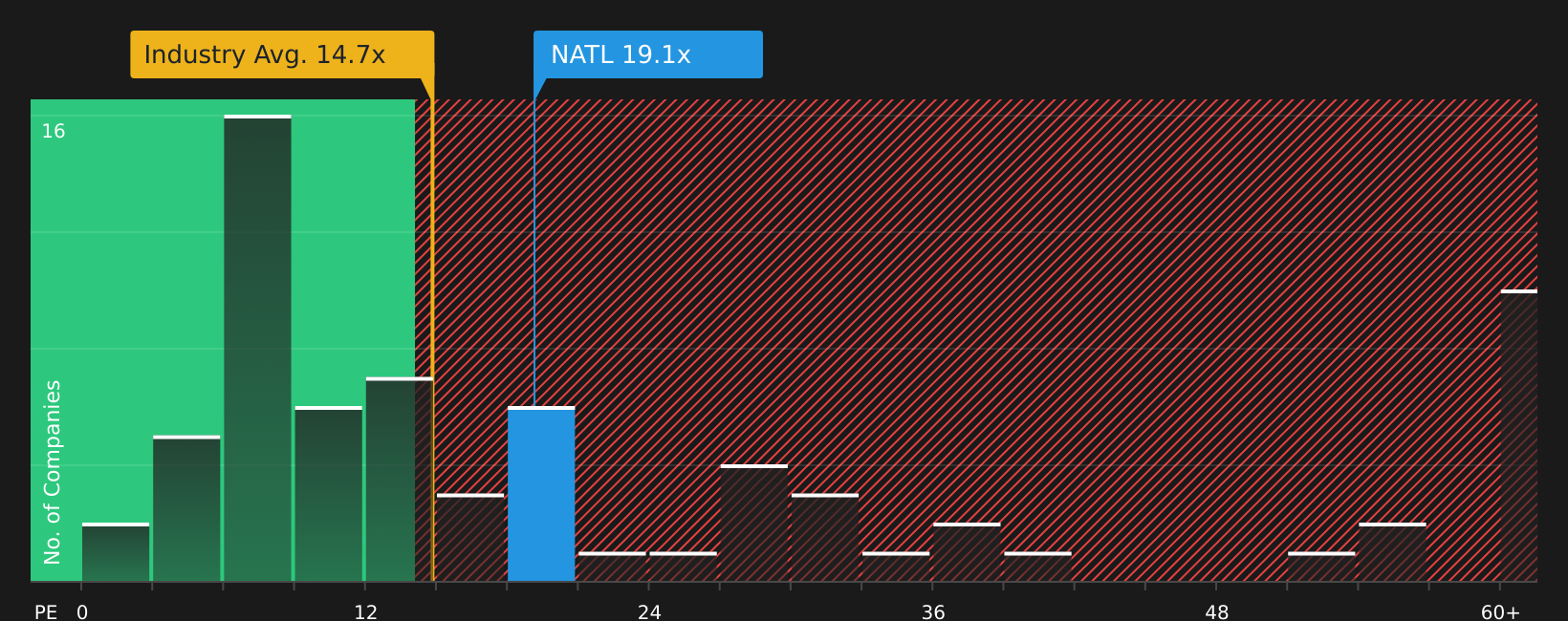

See our latest analysis for NCR Atleos.

The Colombia Cashzone launch comes after a solid run in the stock, with a 90 day share price return of 11.31% and a year to date share price return of 21.30%. The 1 year total shareholder return is 68.63%, which suggests that momentum has been building around the story.

If this kind of international expansion has your attention, it could be a good time to broaden your search and check out 20 top founder-led companies

With NCR Atleos trading at US$45.16 and an average analyst price target of US$50.27, the stock sits at an 11% discount. This raises the question: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 10.2% Undervalued

Analysts see NCR Atleos as worth $50.27 per share, compared with the last close at $45.16, which has shaped a widely followed narrative around the stock.

High recurring revenue mix (over 70% in Q2), significant productivity gains through AI-driven service optimization, and a rapidly scaling backlog are associated with strong margin expansion and robust free cash flow. These factors underpin announced share buybacks and sustained EPS growth and suggest the current valuation does not reflect enhanced long-term earnings power.

Want to see how steady revenue assumptions, rising margins, and a reset earnings multiple work together here? The narrative connects them in a way the share price does not fully spell out.

Result: Fair Value of $50.27 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change quickly if cash usage falls faster than expected or if fintech competition squeezes ATM and payment service margins.

Find out about the key risks to this NCR Atleos narrative.

Another View: Earnings Multiple Sends a Different Signal

That 10.2% gap to fair value is built around analyst earnings forecasts, yet the current 19.6x P/E is higher than both peer companies at 6x and the US Diversified Financial industry at 17.9x, while sitting just below a 20.7x fair ratio. For you, does that tilt this story toward opportunity or valuation risk?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages in the story so far? Take a moment to weigh the upside against the concerns, then move quickly to check the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If NCR Atleos has sparked fresh thinking, do not stop here. Broaden your options now so you are not relying on a single story.

- Target potential upside in quality at a discount by running your own search using the 46 high quality undervalued stocks.

- Shield your portfolio from shocks by focusing on companies that stand out in the 65 resilient stocks with low risk scores.

- Get ahead of the crowd by scanning the screener containing 22 high quality undiscovered gems before others catch on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com