- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Unveiling 3 Undiscovered Gems in the US Market

The United States market has experienced a flat performance over the last week but has seen a significant 30% increase over the past year, with earnings projected to grow by 16% annually. In this dynamic environment, identifying stocks that combine strong fundamentals and growth potential can be key to uncovering hidden opportunities in the market.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 68.27% | 1.25% | -3.09% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Bank of the James Financial Group | 10.99% | 5.54% | 3.94% | ★★★★★★ |

| Sound Financial Bancorp | 16.27% | 0.75% | -13.28% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.53% | 11.34% | ★★★★★★ |

| Winchester Bancorp | 121.44% | 49.13% | 3283.33% | ★★★★★★ |

| Seneca Foods | 38.64% | 2.39% | -18.65% | ★★★★★☆ |

| NameSilo Technologies | 12.63% | 14.48% | 3.12% | ★★★★★☆ |

Here we highlight a subset of our preferred stocks from the screener.

Calavo Growers (CVGW)

Simply Wall St Value Rating: ★★★★★★

Overview: Calavo Growers, Inc. is involved in sourcing, packing, and distributing fresh produce like avocados, tomatoes, and papayas while also processing guacamole and other avocado products for various retail and foodservice channels worldwide; it has a market cap of $502.80 million.

Operations: Calavo's revenue primarily comes from its Fresh segment, generating $541.44 million, while the Prepared segment contributes $74.82 million. The company's gross profit margin shows a notable trend at 7%.

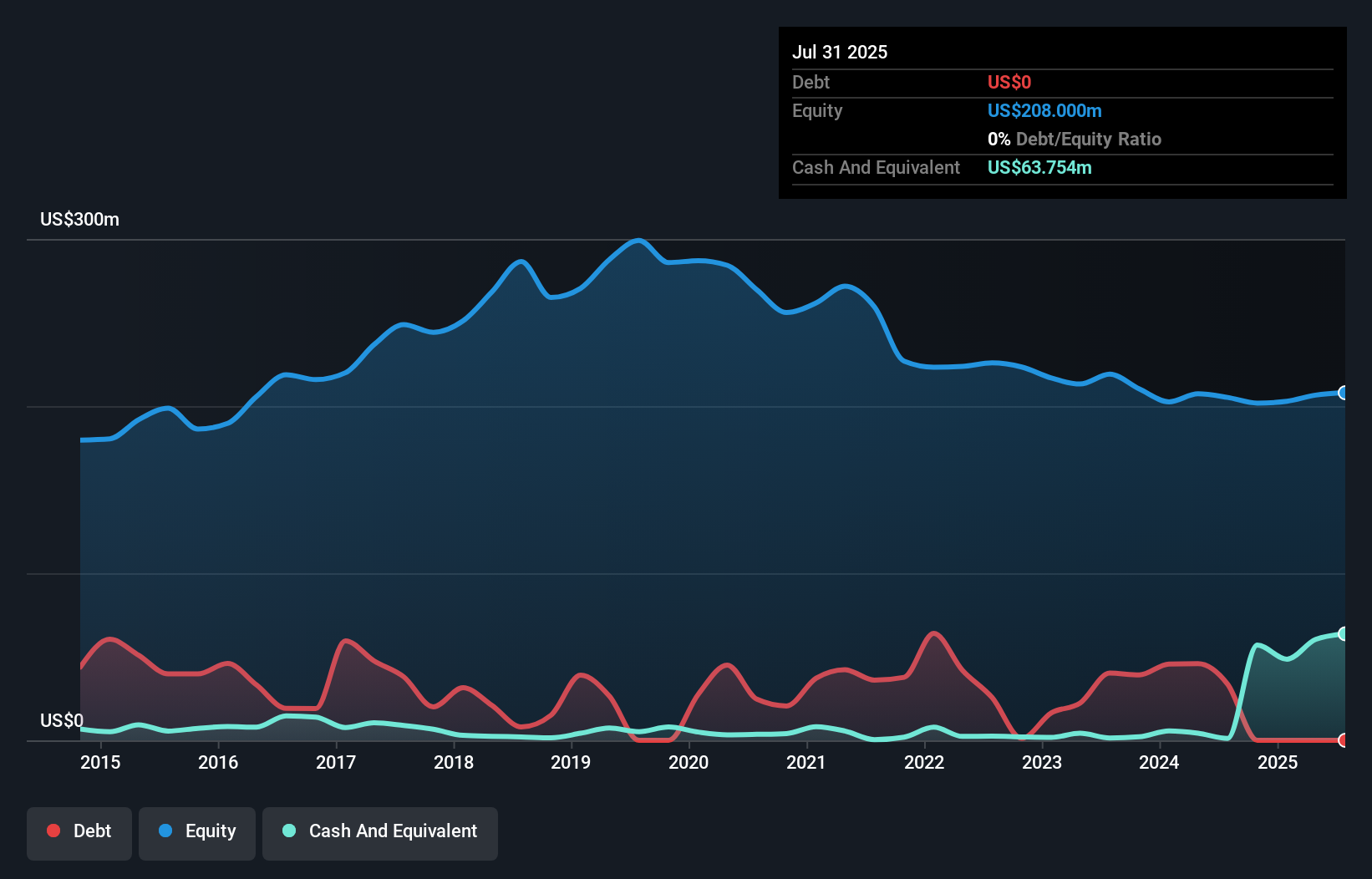

Calavo Growers, a nimble player in the food industry, has demonstrated resilience with earnings growth of 16.8% over the past year, outperforming the sector's -13.9%. Currently trading at 59.7% below its estimated fair value, it presents an intriguing opportunity for investors seeking undervalued prospects. The company is debt-free now compared to a debt-to-equity ratio of 14.2% five years ago, indicating financial discipline and stability. However, recent results show challenges with sales dropping to US$122 million from US$154 million and net income at US$0.73 million versus last year's US$4.42 million due to a one-off loss impacting financials by US$6 million.

- Dive into the specifics of Calavo Growers here with our thorough health report.

Explore historical data to track Calavo Growers' performance over time in our Past section.

Ennis (EBF)

Simply Wall St Value Rating: ★★★★★★

Overview: Ennis, Inc. is a company that produces and sells business forms and other printed products in the United States, with a market cap of $514.20 million.

Operations: The company's primary revenue stream is from its Print segment, generating $392.40 million.

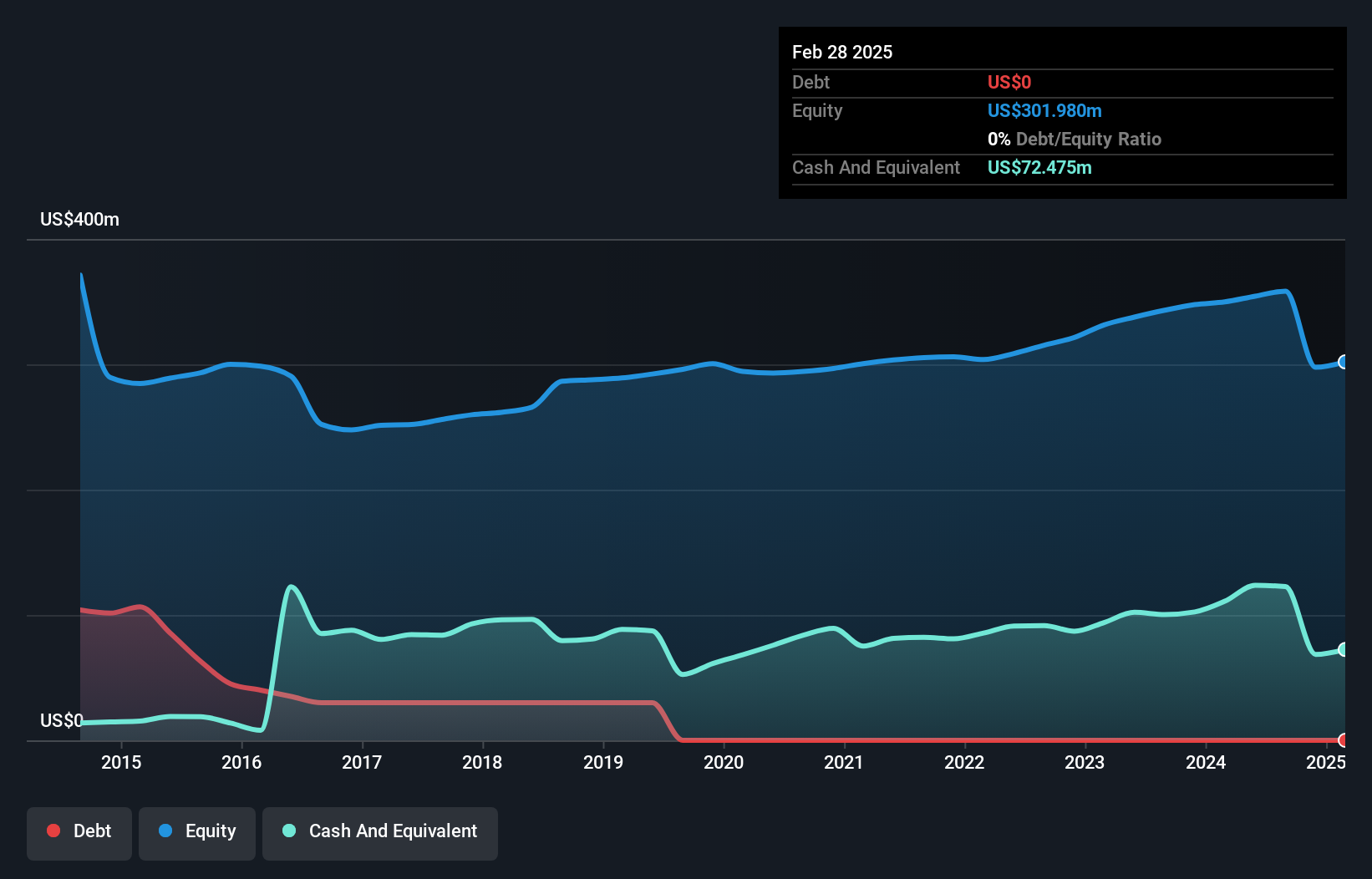

Ennis, a company with a market cap reflecting its smaller size, has been showing steady financial health. Over the past five years, earnings have grown at an average annual rate of 8.5%, demonstrating consistent progress. The firm is debt-free and boasts high-quality earnings, which speaks volumes about its operational efficiency. Recent results highlight stable performance with full-year sales at US$392 million and net income rising to US$42.63 million from the previous year’s US$40.22 million. Trading at 45% below estimated fair value suggests potential upside for investors seeking undervalued opportunities in this space.

Genie Energy (GNE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Genie Energy Ltd. operates through its subsidiaries to provide energy services both in the United States and internationally, with a market capitalization of approximately $366.16 million.

Operations: Genie Energy's primary revenue streams are derived from Genie Retail Energy, excluding Genie Energy Services and GRE International, contributing $462.20 million, while Genie Renewables adds $21.09 million.

Genie Energy seems to be an intriguing player with its earnings surging 118.9% last year, far outpacing the Electric Utilities industry’s 11.5%. The company trades at a discount, approximately 18.8% below estimated fair value, offering potential upside for investors. Despite a rise in debt to equity from 1.6% to 4.7% over five years, it maintains more cash than total debt and has positive free cash flow of US$34.96 million as of April 2026. However, recent delisting concerns due to delayed filings might impact investor confidence despite its promising growth trajectory in renewable energies and advisory services.

Key Takeaways

- Investigate our full lineup of 331 US Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com