- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Dave (DAVE) Stock After Buyback Expansion And New Funding Deal Is The Valuation Gap Still There

Dave (DAVE) has drawn fresh attention after expanding its share repurchase authorization to US$300 million and unveiling a new funding arrangement for its ExtraCash receivables with Coastal Community Bank, reshaping its capital and liquidity profile.

See our latest analysis for Dave.

The share price is now US$286.78 after a 7 day share price return of 11.05% and a 90 day share price return of 35.26%, while the 1 year total shareholder return of 37.72% sits against a five year total shareholder return that is slightly down. This suggests that recent momentum has been building from a weaker longer term base.

If you are looking for more ideas beyond Dave, this could be a good moment to scan other financial technology plays through 20 top founder-led companies

With the stock up strongly over the past year, trading at US$286.78 and sitting around 17% below the average analyst price target of US$335.73, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 14.1% Undervalued

With Dave's narrative fair value set at $333.91 against a last close of $286.78, the current price sits below what that framework suggests is reasonable.

Strategic infrastructure shifts, including transitioning ExtraCash receivables off-balance sheet via the Coastal Community Bank partnership (at a reduced cost of funds), are expected to free significant capital, lower funding and operational costs, and increase financial flexibility, positively impacting earnings and net margins.

Want to see what is baked into that fair value gap? Revenue expansion, margin assumptions, and a future earnings multiple all pull in the same direction. The mix may surprise you.

Result: Fair Value of $333.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative can still be knocked off course if tighter regulation hits fee based products, or if rising competition pushes up customer acquisition costs and squeezes margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Angle on Valuation

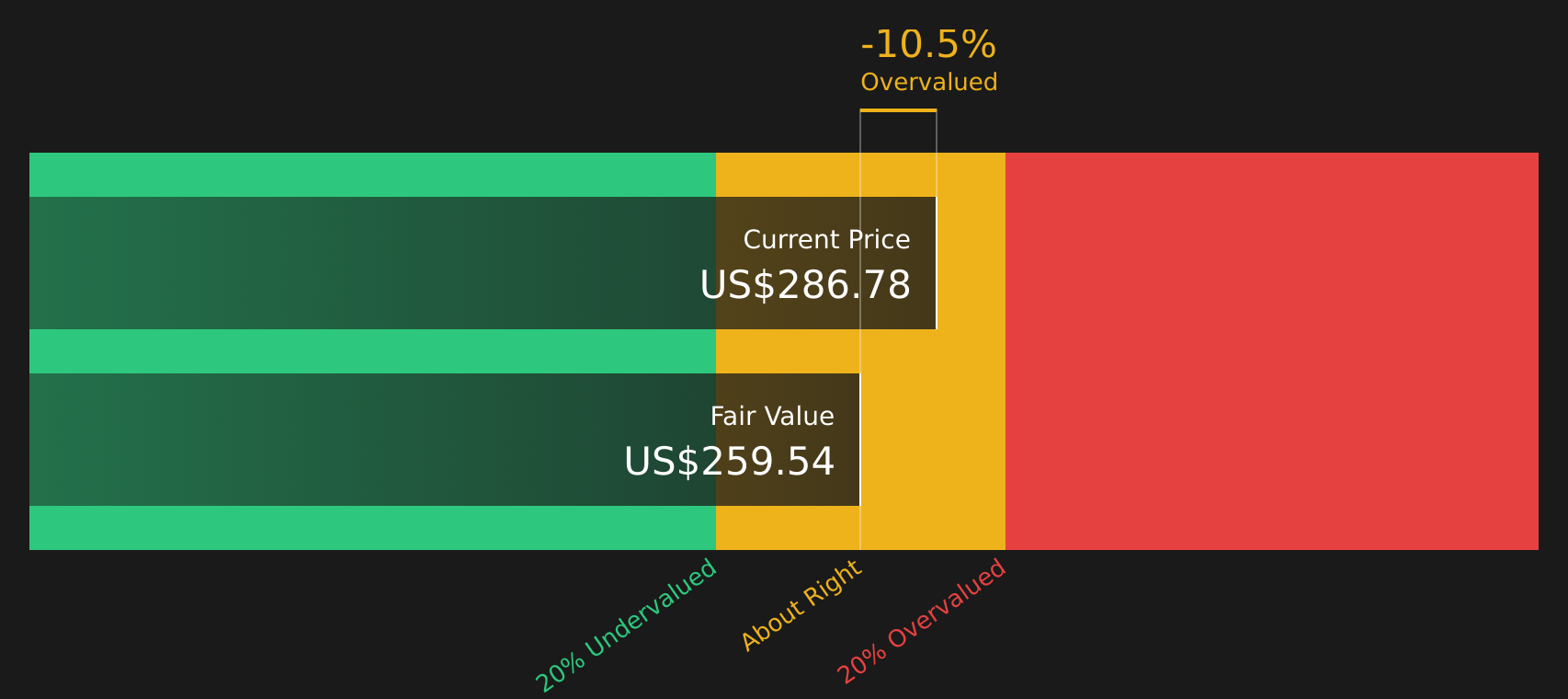

The earlier view leans on analyst earnings forecasts, but the Simply Wall St DCF model tells a different story. On that framework, Dave at $286.78 sits above an estimated future cash flow value of $259.59, suggesting the stock screens as overvalued on this method. Which lens matters more for you?

Before leaning on any one model, it is worth understanding exactly how our DCF model works and where its assumptions might feel tight or conservative for your own thesis, so you can judge whether this gap looks like risk or just a difference in methodology, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dave for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed after weighing both upside potential and open questions, it makes sense to move quickly, review the data yourself, and pressure test where you stand against the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If you stop here, you might miss other stocks that fit your style even better, so use this moment to line up your next candidates thoughtfully.

- Spot potential bargains by scanning companies that screen as 44 high quality undervalued stocks and see which ones line up with your return expectations and risk comfort.

- Prioritise resilience by reviewing 70 resilient stocks with low risk scores so you can focus on businesses where the risk profile may feel more controlled.

- Hunt for fresher opportunities by checking the screener containing 20 high quality undiscovered gems that might not yet be widely followed but still meet your quality bar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com