- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

The Bull Case For Fiserv (FISV) Could Change Following New AI Partnerships And Integrations – Learn Why

- In late May and early June 2026, Fiserv’s technology profile shifted as Experian announced a new real-time debit verification integration using Fiserv’s VerifyNow Advantage, and Fiserv disclosed a partnership with Cognition to deploy its Devin AI software engineer for core banking modernization while presenting these innovations at the Snowflake Summit in San Francisco.

- Together, these moves highlight Fiserv’s push to embed advanced AI and real-time data capabilities deeper into its platforms, aiming to speed product delivery for financial institutions while tightening governance and security around AI-assisted development.

- We’ll now examine how Fiserv’s deployment of Devin for core banking modernization could reshape the company’s investment narrative and future execution risks.

Find 46 companies with promising cash flow potential yet trading below their fair value.

Fiserv Investment Narrative Recap

To own Fiserv today, you generally need to believe that its broad payments and banking technology footprint can still convert modernization projects into consistent, profitable growth, despite slowing organic revenue momentum and recent earnings pressure. The Devin partnership and Experian’s real-time debit verification integration speak directly to the key short term catalyst of faster product delivery, but they do not yet clearly offset the core risk of execution delays in large modernization efforts.

Of the recent announcements, the Cognition partnership around Devin is the most directly tied to execution risk, because it targets one of Fiserv’s slowest and most complex areas: core banking modernization. If Devin materially shortens release cycles and strengthens testing at scale, it could help counter concerns about delayed launches and margin strain from heavy investment. At the same time, expanding AI across mission critical codebases may introduce new operational and governance risks if results fall short of expectations.

Yet behind the appeal of AI accelerated modernization, investors should also be aware of the risk that...

Read the full narrative on Fiserv (it's free!)

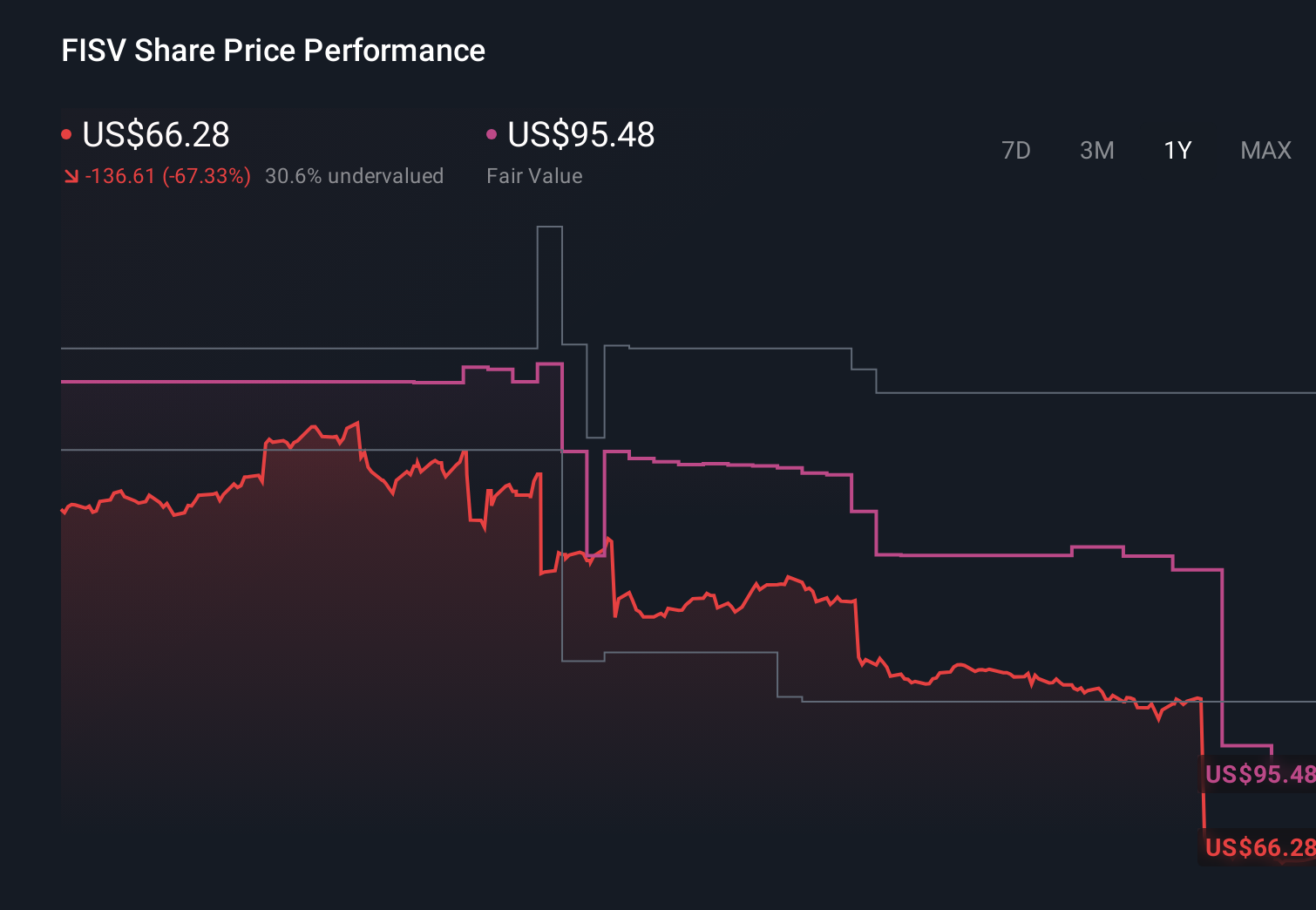

Fiserv’s narrative projects $21.9 billion revenue and $3.7 billion earnings by 2029. This requires 1.3% yearly revenue growth and a $0.5 billion earnings increase from $3.2 billion today.

Uncover how Fiserv's forecasts yield a $69.96 fair value, a 29% upside to its current price.

Exploring Other Perspectives

While consensus focuses on modernization as a potential tailwind, the most pessimistic analysts were already assuming roughly flat revenue near US$21.2 billion and slightly lower earnings of about US$3.3 billion by 2029, reminding you that expectations for how much technology like Devin can really change Fiserv’s earnings path can differ widely across thoughtful investors.

Explore 17 other fair value estimates on Fiserv - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Fiserv research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Fiserv research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Fiserv's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com