- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Exploring Undervalued Small Caps With Insider Activity In June 2026

Over the last 7 days, the United States market has experienced a 2.7% drop, yet it remains up by 23% over the past year with projected annual earnings growth of 17%. In this fluctuating environment, identifying small-cap stocks that are undervalued and exhibit insider activity can present unique opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Betterware de MéxicoP.I. de | 9.9x | 0.8x | 44.29% | ★★★★★★ |

| Ferroglobe | NA | 0.5x | 28.64% | ★★★★★☆ |

| Appian | 2026.5x | 2.4x | 30.14% | ★★★★★☆ |

| First Bancorp | 9.2x | 3.5x | 29.80% | ★★★★☆☆ |

| Shore Bancshares | 11.4x | 3.2x | 49.98% | ★★★★☆☆ |

| Union Bankshares | 9.3x | 2.0x | 20.56% | ★★★★☆☆ |

| Similarweb | NA | 1.3x | 33.91% | ★★★★☆☆ |

| German American Bancorp | 12.3x | 4.5x | 43.39% | ★★★☆☆☆ |

| Bank of Marin Bancorp | NA | 11.7x | 34.16% | ★★★☆☆☆ |

| Bank of the James Financial Group | 10.1x | 2.2x | 21.15% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

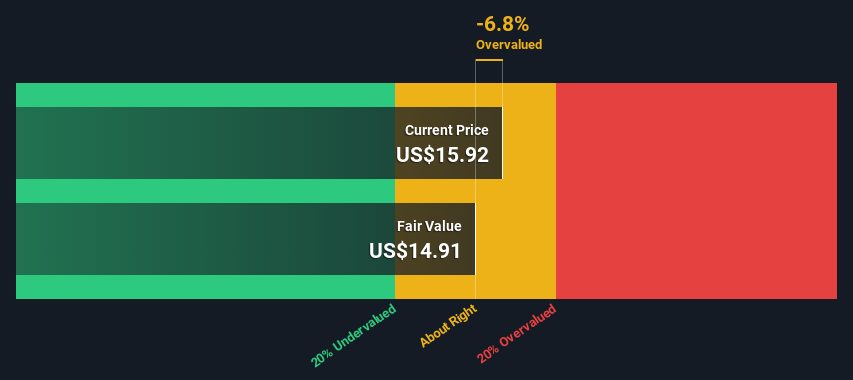

Community Trust Bancorp (CTBI)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Community Trust Bancorp operates primarily in community banking services and has a market capitalization of approximately $0.71 billion.

Operations: Community Trust Bancorp generates revenue primarily from its Community Banking Services, with significant contributions from its Holding Company segment. The company's net income margin has shown a notable trend, reaching 36.96% as of March 2026. Operating expenses are predominantly driven by general and administrative costs, which accounted for $117.93 million in the latest period analyzed.

PE: 12.0x

Community Trust Bancorp, a smaller player in the financial sector, is showing signs of potential growth. Their earnings for Q1 2026 increased to US$27.19 million from US$21.97 million year-over-year, with net interest income rising to US$58.78 million. Insider confidence is evident as executives have been purchasing shares recently, reflecting belief in its prospects despite upcoming retirements like that of their Executive VP by February 2027. Earnings are projected to grow at 5% annually, suggesting steady progress ahead.

Krispy Kreme (DNUT)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Krispy Kreme is a global doughnut company and coffeehouse chain known for its fresh, hot doughnuts and operates across various segments with a market capitalization of approximately $2.28 billion.

Operations: The company generates revenue primarily from its U.S. segment, followed by international operations and market development. Over recent periods, the gross profit margin has shown variability, with a notable decline to 23.35% in mid-2025 from 28.25% at the end of 2023. Operating expenses have consistently been a significant part of costs, with general and administrative expenses being a substantial component within operating costs.

PE: -1.2x

Krispy Kreme, a notable player in the doughnut industry, is currently unprofitable and not expected to turn a profit within the next three years. The company's funding relies entirely on external borrowing, which poses higher risks compared to customer deposits. Despite these challenges, Krispy Kreme continues to innovate with limited-time offerings like their Masters of the Universe Collection and expansion plans into new markets such as the Netherlands. Although revenue dipped slightly in Q1 2026 to US$367 million from US$375 million a year earlier, net losses narrowed significantly from US$33 million to US$23 million. As they aim for annual revenues between US$1.25 billion and US$1.35 billion this year, insiders have shown confidence by purchasing shares recently, hinting at potential future growth opportunities despite current financial hurdles.

- Click to explore a detailed breakdown of our findings in Krispy Kreme's valuation report.

Gain insights into Krispy Kreme's past trends and performance with our Past report.

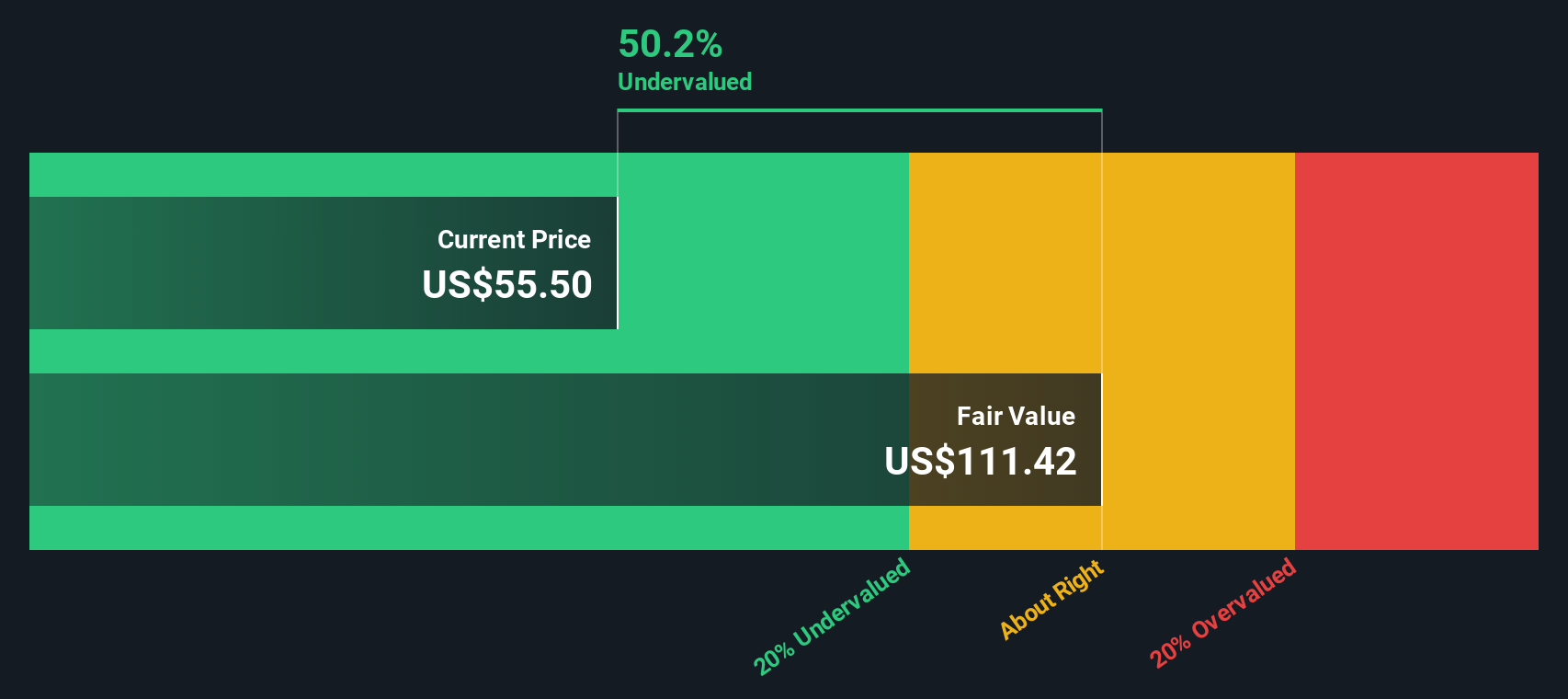

Shore Bancshares (SHBI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shore Bancshares operates as a community banking organization providing financial services, with a market capitalization of $0.22 billion.

Operations: The company generates revenue primarily through community banking services, with recent figures showing $224.40 million in revenue. Operating expenses have been a significant component of the cost structure, reaching $128.93 million in the latest period. The net income margin has shown variability, with a recent figure of 27.99%.

PE: 11.4x

Shore Bancshares, a smaller player in the financial industry, recently announced a share repurchase program worth up to US$30 million, reflecting insider confidence. The company reported strong first-quarter results with net interest income rising to US$52.56 million from US$45.9 million last year and net income climbing to US$17.09 million from US$13.76 million. Despite low allowance for bad loans at 90%, earnings are projected to grow 9% annually, indicating potential value for investors seeking growth opportunities in this segment.

- Delve into the full analysis valuation report here for a deeper understanding of Shore Bancshares.

Assess Shore Bancshares' past performance with our detailed historical performance reports.

Summing It All Up

- Get an in-depth perspective on all 71 Undervalued US Small Caps With Insider Buying by using our screener here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com