- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

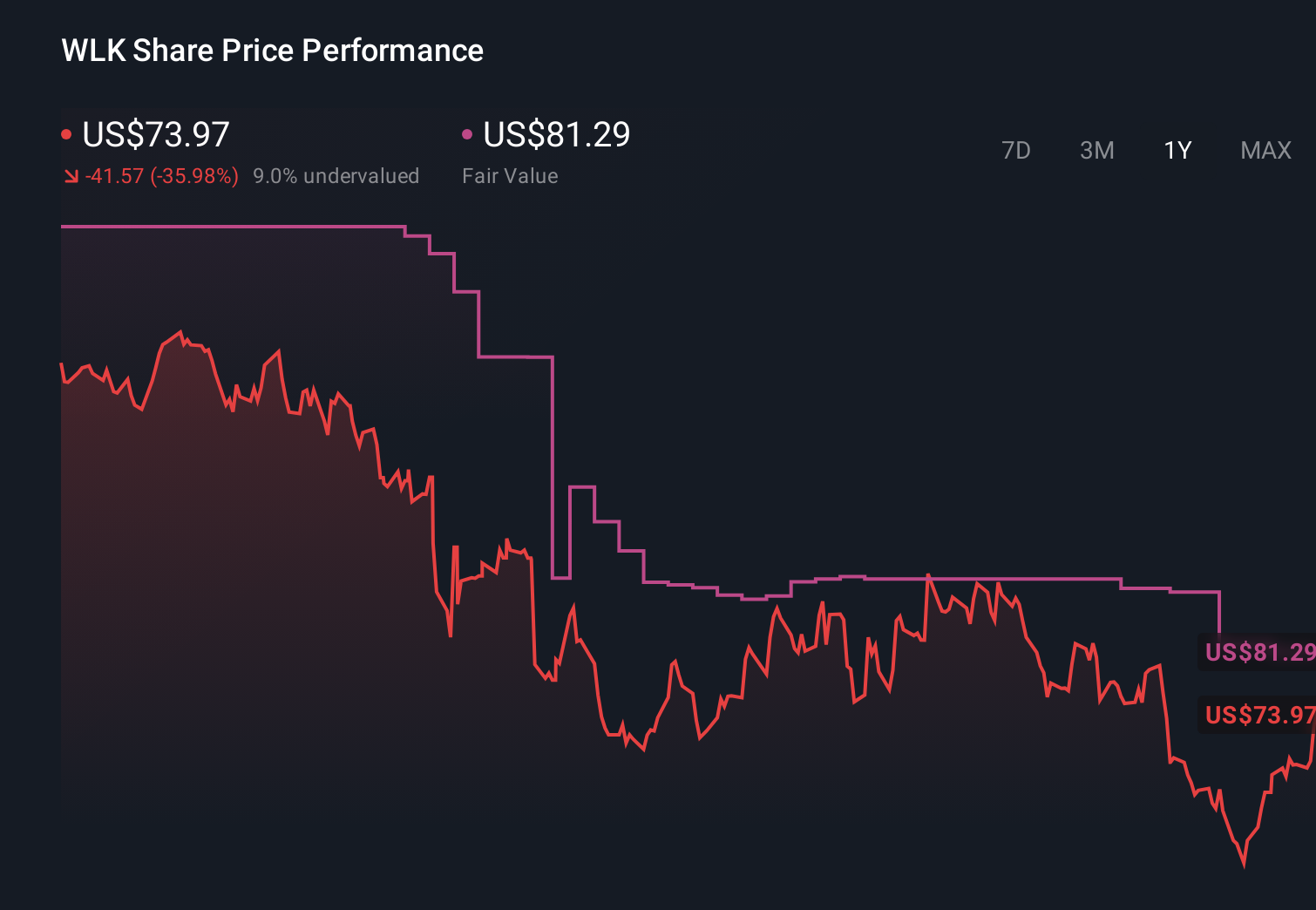

How PVC Price Pressures and Housing Weakness Will Impact Westlake (WLK) Investors

- Recently, Citi and JPMorgan downgraded Westlake Corporation to Neutral, citing fading momentum in polyvinyl chloride pricing, normalizing Asian PVC markets amid weak construction activity and ample supply, and a slower-than-expected recovery in housing.

- The downgrades highlight how sensitive Westlake’s chemicals and building-products earnings can be to shifts in global construction demand and regional PVC pricing.

- Next, we’ll examine how concerns about softening PVC prices and sluggish housing demand may reshape Westlake’s previously optimistic investment narrative.

Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

Westlake Investment Narrative Recap

To own Westlake, you need to believe that its mix of commodity chemicals and building products can still create value despite earnings cyclicality. The Citi and JPMorgan downgrades sharpen the focus on PVC pricing and housing as the key near term swing factors. Softer Asian PVC prices and a slower housing recovery directly pressure what looks like the most important short term catalyst, a rebound in PEM and HIP margins, while reinforcing the risk of prolonged construction and pricing weakness.

Against this backdrop, Westlake’s recent Q1 2026 results, which showed lower sales and a wider net loss, look particularly relevant. They already reflect weaker pricing and demand, so the new concerns from Citi and JPMorgan may reinforce questions about how quickly earnings can improve. For investors, the latest numbers and the downgrades together make it harder to lean on a near term earnings recovery as the core part of the thesis.

Yet investors should also be aware of how prolonged global oversupply in key chemical chains could…

Read the full narrative on Westlake (it's free!)

Westlake's narrative projects $12.9 billion revenue and $764.4 million earnings by 2029. This requires 5.5% yearly revenue growth and about a $2.4 billion earnings increase from -$1.6 billion today.

Uncover how Westlake's forecasts yield a $114.29 fair value, a 34% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue of about US$13.3 billion and earnings near US$546 million by 2029, which sits in clear tension with today’s PVC and housing worries and shows just how far views can differ before this new information is fully reflected.

Explore 3 other fair value estimates on Westlake - why the stock might be worth 20% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Westlake research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Westlake research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Westlake's overall financial health at a glance.

Curious About Other Options?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com