- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

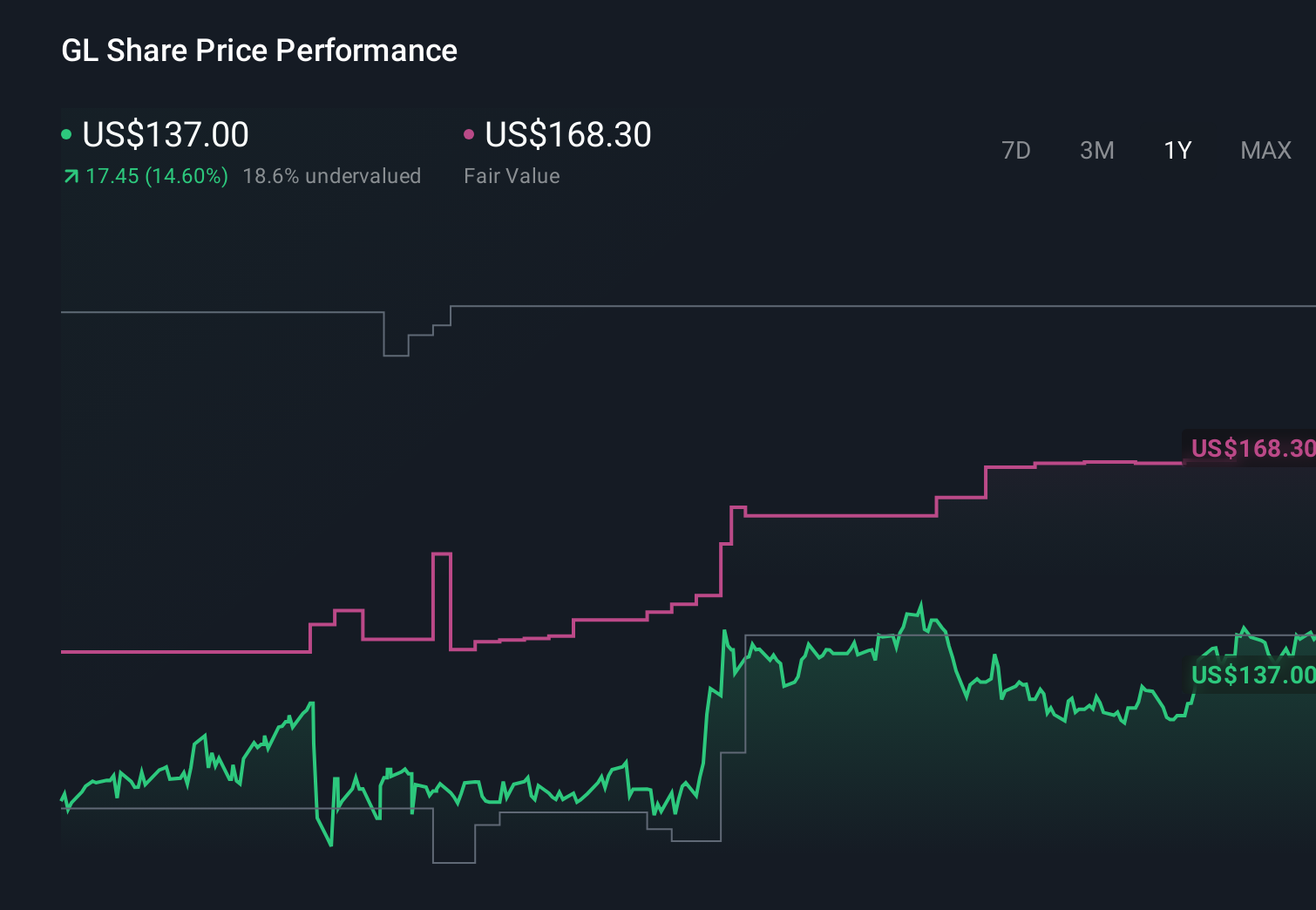

Stronger 2026 Outlook And Analyst Downgrade Could Be A Game Changer For Globe Life (GL)

- In the first quarter of 2026, Globe Life Inc. reported 11.7% year-over-year growth in net operating income but slightly missed earnings estimates due to elevated expenses, while also raising its full-year 2026 net operating income guidance to US$15.40–US$15.90 per diluted share.

- An interesting wrinkle is that this stronger full-year outlook coincided with an analyst downgrade, highlighting a gap between Globe Life’s improved guidance and more cautious external sentiment.

- Next, we’ll explore how Globe Life’s higher full-year operating income guidance reshapes the existing investment narrative built around efficiency gains and capital returns.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 28 companies in the world exploring or producing it. Find the list for free.

Globe Life Investment Narrative Recap

To own Globe Life, you need to be comfortable with a story built around steady insurance demand, agent-led distribution, and disciplined capital returns. The latest quarter’s higher full-year net operating income guidance supports that thesis, while the earnings miss and analyst downgrade underscore how higher expenses and ongoing regulatory scrutiny remain the key near term risk rather than a thesis-changing event.

The recent decision to again raise full year 2026 net operating income guidance to US$15.40–US$15.90 per diluted share is particularly relevant here, because it directly reflects management’s view of earnings power even as buybacks and dividend increases continue to return capital. For investors focused on catalysts, this combination of higher guidance and ongoing repurchases offers a clearer yardstick against which to weigh concerns about costs, investigations, and distribution shifts.

Yet, while guidance is moving up, the risk tied to ongoing DOJ and SEC investigations is something investors should be acutely aware of as...

Read the full narrative on Globe Life (it's free!)

Globe Life's narrative projects $6.8 billion revenue and $1.3 billion earnings by 2028. This requires 5.1% yearly revenue growth and about a $0.2 billion earnings increase from $1.1 billion today.

Uncover how Globe Life's forecasts yield a $172.10 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Before this report, the most cautious analysts expected Globe Life to reach about US$7.2 billion in revenue and US$1.3 billion in earnings by 2029, which is far less upbeat than narratives that lean on agent growth and technology gains, so this new guidance may push you to reassess where you sit between those views.

Explore 3 other fair value estimates on Globe Life - why the stock might be worth just $172.10!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Globe Life research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Globe Life research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Globe Life's overall financial health at a glance.

No Opportunity In Globe Life?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com