- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Can Bruker (BRKR) Turn Ultra‑High‑Field MRI Leadership Into Lasting Competitive Moats?

- Bruker Corporation recently commissioned its BioSpec 18 Tesla preclinical MRI, the world’s highest-field horizontal-bore system, at the Champalimaud Foundation in Lisbon to support advanced cancer and neuroscience research.

- This installation strengthens Bruker’s position in ultra-high-field imaging technologies that underpin cutting-edge biomarker discovery and translational preclinical studies.

- We’ll now examine how commissioning the world’s highest-field preclinical MRI may influence Bruker’s investment narrative and long-term research positioning.

Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Bruker Investment Narrative Recap

To own Bruker, you need to believe that its leadership in advanced research instruments can translate into sustainable, profitable growth despite recent margin pressure and weak organic revenue. The Champalimaud 18T MRI commissioning reinforces Bruker’s technical edge in ultra high field imaging, but it does not directly change the near term catalyst of restoring earnings quality or the key risk that prolonged funding softness in academic and biopharma markets could restrain demand.

The most relevant recent announcement beside the 18T MRI is Bruker’s reiterated quarterly dividend of US$0.05 per share, payable on 7 July 2026. While modest, this regular payout sits against a backdrop of unprofitable results and rising costs, highlighting the tension between rewarding shareholders today and funding continued innovation in high end platforms like the new preclinical MRI, especially if revenue growth remains muted.

Yet behind the appeal of world leading MRI technology, investors should also be aware that prolonged weakness in research funding and book to bill trends could...

Read the full narrative on Bruker (it's free!)

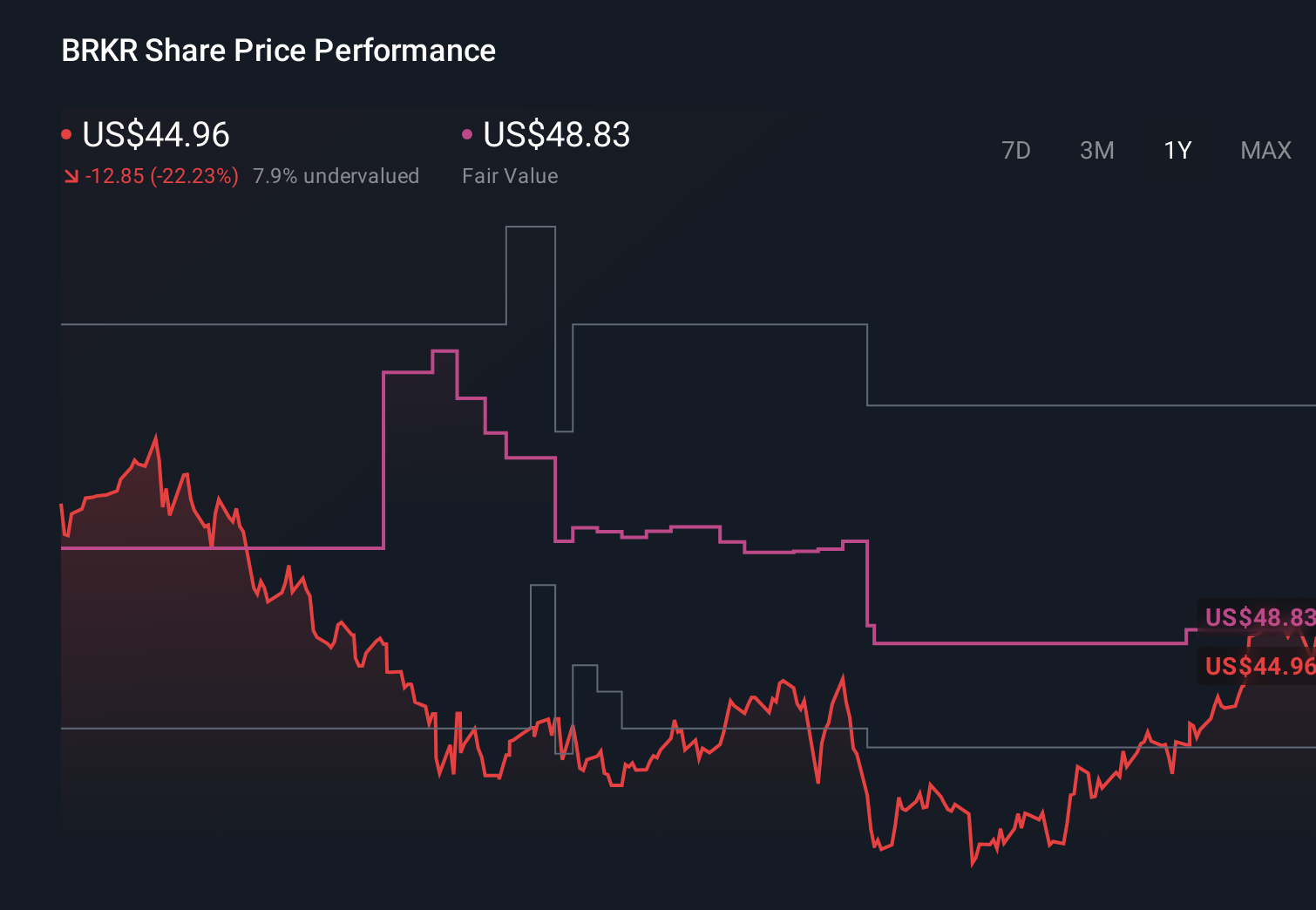

Bruker’s narrative projects $4.0 billion revenue and $332.4 million earnings by 2029.

Uncover how Bruker's forecasts yield a $49.15 fair value, a 8% upside to its current price.

Exploring Other Perspectives

While the 18T MRI showcases Bruker’s innovation, the most bearish analysts still model only about 4 percent annual revenue growth and US$273.2 million earnings by 2029, so you should weigh this more pessimistic path against the upside potential if the funding and cost pressures they worry about begin to ease.

Explore 4 other fair value estimates on Bruker - why the stock might be worth 31% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bruker research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bruker research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bruker's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com