- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

US Undiscovered Gems To Explore In May 2026

The United States market has shown a robust performance, with a 1.1% increase over the last week and an impressive 29% rise over the past year, while earnings are projected to grow by 17% annually. In such a dynamic environment, identifying undiscovered gems involves seeking stocks that not only align with these growth trends but also offer unique value propositions and potential for long-term appreciation.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| First Bancorp | 69.86% | 1.25% | -3.09% | ★★★★★★ |

| Cashmere Valley Bank | 31.63% | 5.07% | 1.43% | ★★★★★★ |

| Oakworth Capital | 51.38% | 15.89% | 14.04% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| Teekay | 2.14% | 10.67% | 57.58% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| NameSilo Technologies | 3.13% | 14.25% | 15.06% | ★★★★★☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

ScanSource (SCSC)

Simply Wall St Value Rating: ★★★★★★

Overview: ScanSource, Inc. operates as a distributor of technology products and solutions both in the United States and internationally, with a market cap of approximately $896.11 million.

Operations: Revenue is primarily derived from Specialty Technology Solutions at $2.99 billion and Intelisys & Advisory at $99.38 million.

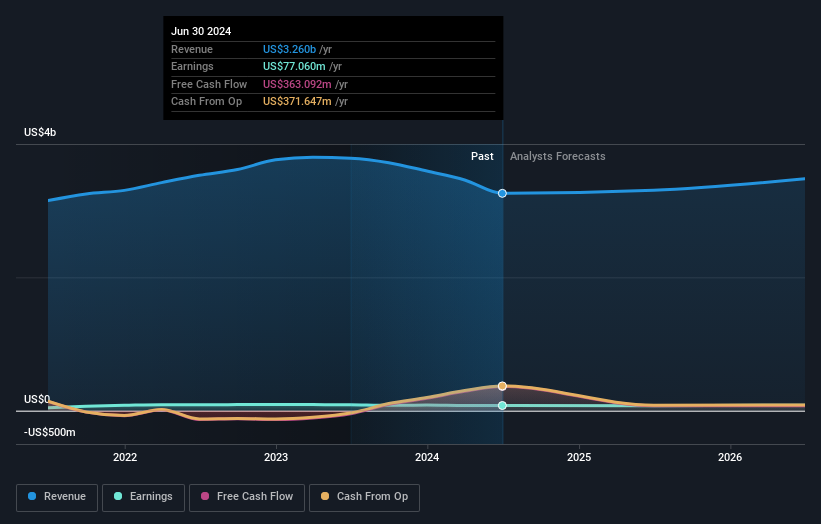

ScanSource, a tech distributor with a knack for strategic growth, has seen its debt to equity ratio drop from 29.7% to 11.3% over five years, highlighting financial discipline. The company repurchased 6.33% of its shares for US$53.61 million, signaling confidence in its valuation, which is currently trading at 16.7% below estimated fair value. Earnings have grown annually by 9.6%, though last year's growth of 8.6% lagged behind the broader electronic industry's pace of 13%. With US$766 million in quarterly sales and ongoing acquisition pursuits, ScanSource is poised for further expansion and recurring revenue enhancement through strategic partnerships and technology integration initiatives.

- Click here to discover the nuances of ScanSource with our detailed analytical health report.

Review our historical performance report to gain insights into ScanSource's's past performance.

Enerpac Tool Group (EPAC)

Simply Wall St Value Rating: ★★★★★★

Overview: Enerpac Tool Group Corp. is a company that manufactures and sells industrial products and solutions globally, with a market capitalization of approximately $1.78 billion.

Operations: Enerpac Tool Group generates its revenue primarily through its Industrial Tool & Services Segment, which accounts for $601.42 million.

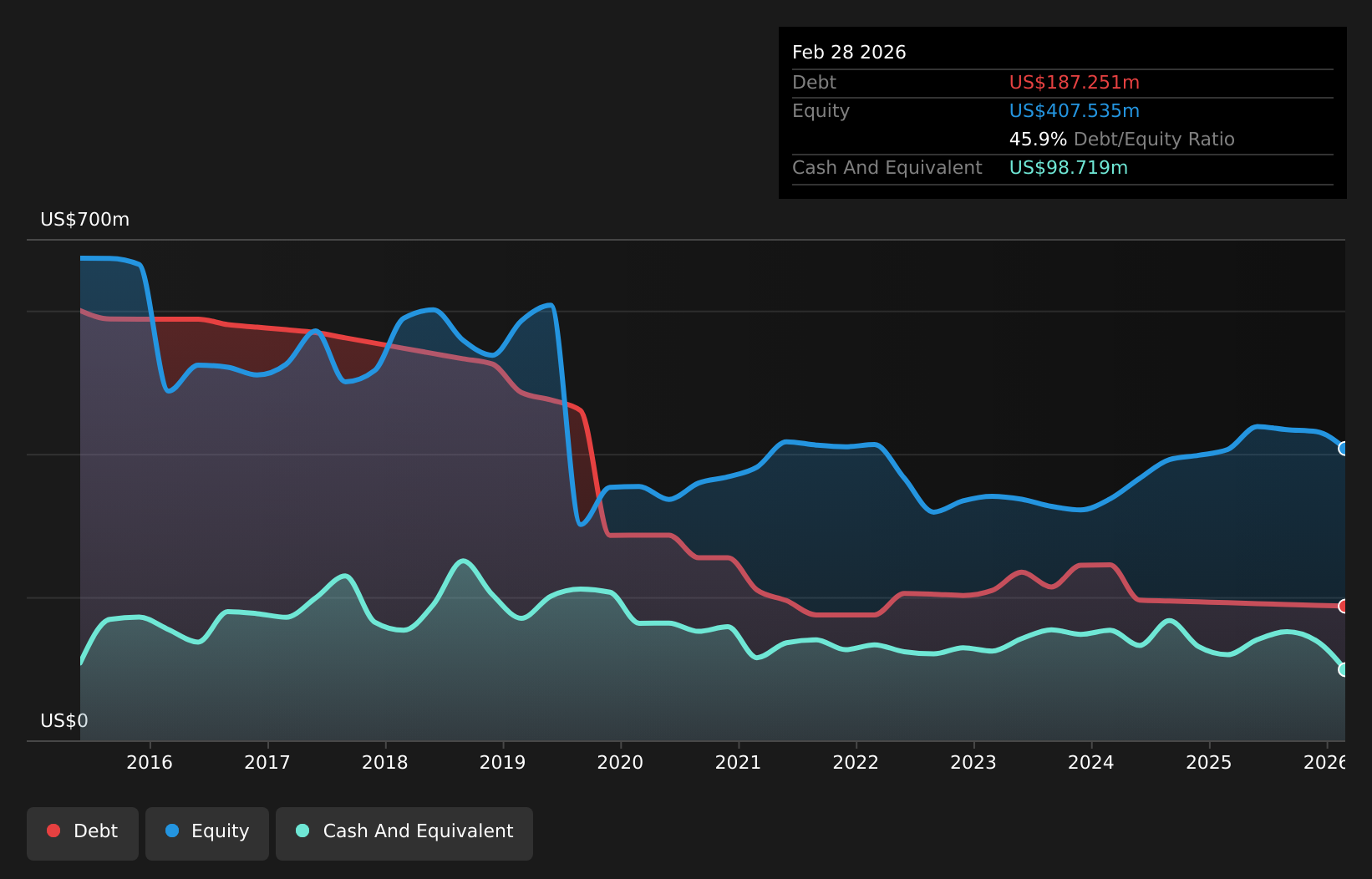

Enerpac Tool Group, a nimble player in the industrial tools sector, offers promising value with its shares trading 36.6% below estimated fair value. The company has shown robust financial health with a net debt to equity ratio of 21.7%, which is deemed satisfactory, and it remains free cash flow positive. Despite facing a slight earnings contraction of 3.5% last year against the industry growth of 1.6%, Enerpac's strategic focus on mergers and acquisitions could bolster future prospects. Recent leadership changes aim to enhance global operations, while share repurchases amounting to $65 million reflect confidence in its growth trajectory.

Global Industrial (GIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Global Industrial Company operates as an industrial distributor of various industrial and MRO products in the United States and Canada, with a market cap of approximately $1.14 billion.

Operations: Global Industrial generates revenue primarily through its Industrial Products Group, which reported $1.41 billion in sales. The company's financial performance is characterized by a focus on distributing industrial and MRO products across the U.S. and Canada.

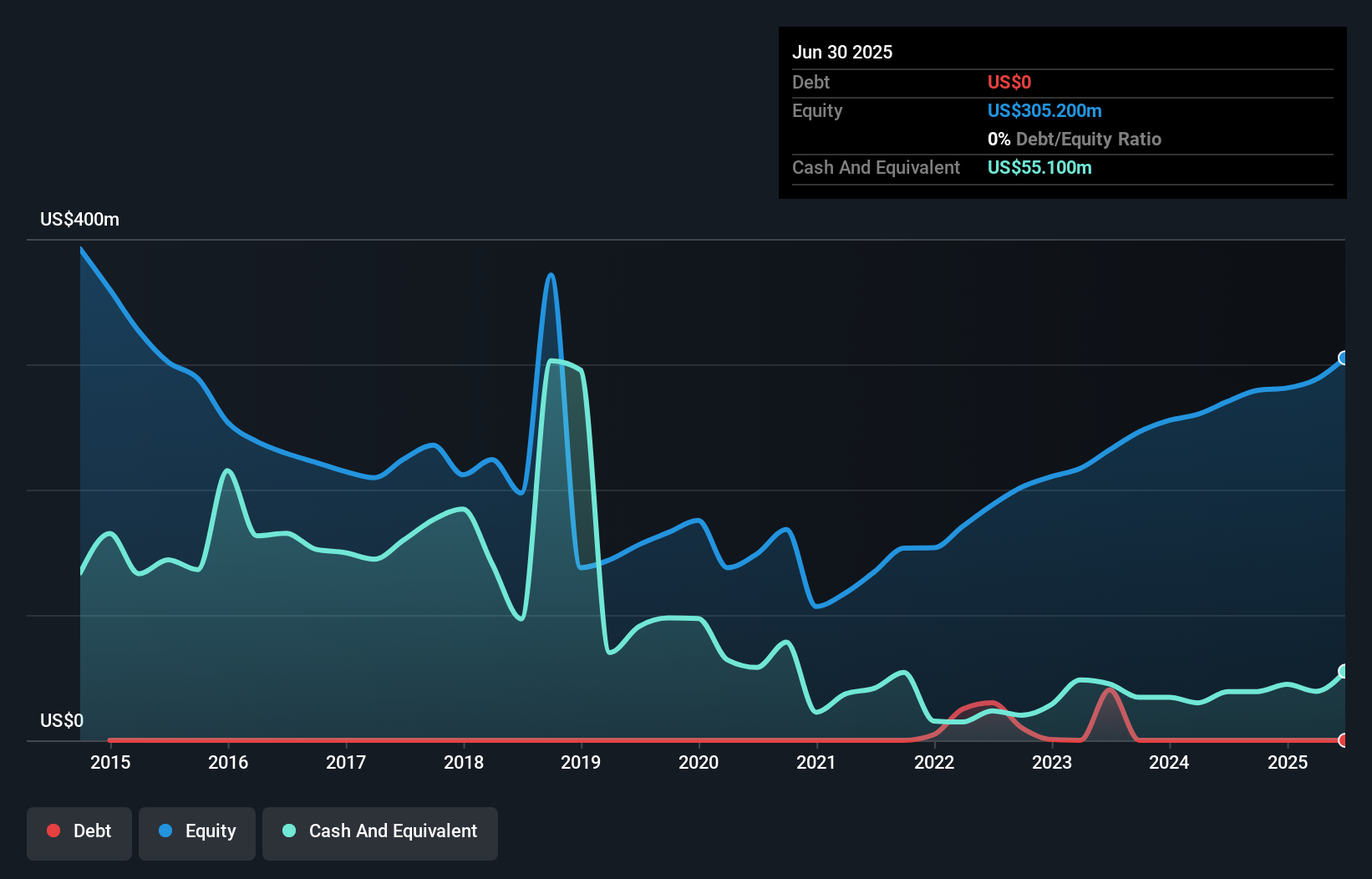

Global Industrial, a nimble player in the distribution sector, has been making waves with its strategic focus on high-value accounts and digital transformation. The company reported first-quarter sales of US$350.4 million, up from US$321 million the previous year, with net income rising to US$16.6 million from US$13.6 million. It boasts no debt and strong free cash flow of US$124.7 million as of September 2023, highlighting financial resilience and operational efficiency. Recent product showcases at industry events reinforce its commitment to expanding market presence despite challenges like tariff costs and e-commerce competition impacting margins.

Summing It All Up

- Unlock our comprehensive list of 338 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com