- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

The Bull Case For First Advantage (FA) Could Change Following Q1 Turnaround And Barclays Upgrade - Learn Why

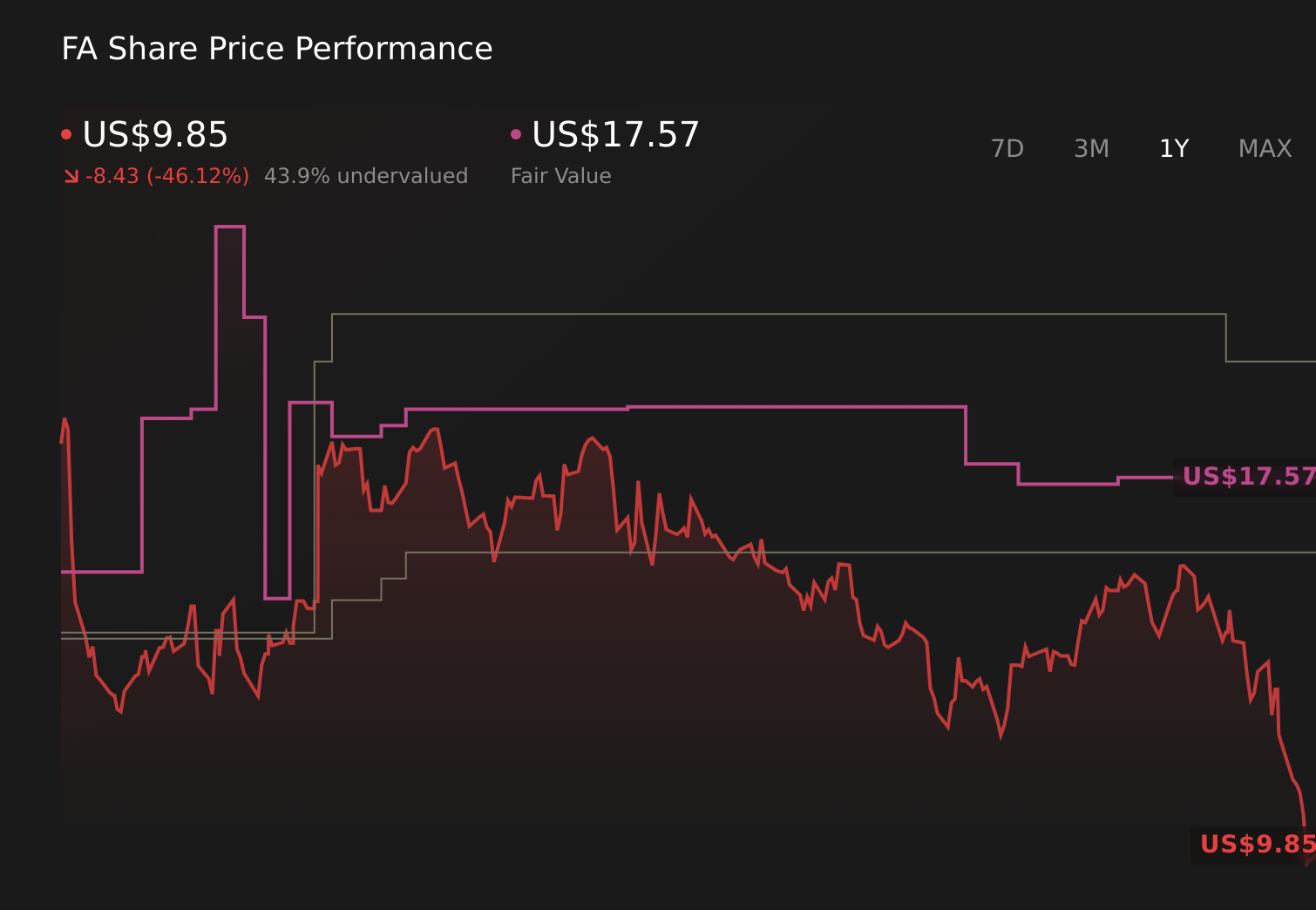

- In recent months, First Advantage reported Q1 2026 results showing 8.6% revenue growth, expanding margins, and a move from loss-making to positive earnings per share, followed by an analyst upgrade from Barclays citing stronger operational execution.

- An interesting aspect of this development is that these improvements arrived after a period of modest earnings expansion and declining free cash flow margins, suggesting a potential shift in how efficiently the company converts its market position into profits.

- We’ll now examine how this operational turnaround and Barclays’ upgrade may influence First Advantage’s existing investment narrative and future expectations.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

First Advantage Investment Narrative Recap

To own First Advantage, you need to believe its background screening and identity platform can translate market presence into sustained, high quality profitability. The short term catalyst is continued evidence that margin gains and the return to positive EPS are repeatable across future quarters. The biggest risk is still pressure on hiring volumes and pricing in a competitive market. The Q1 2026 beat and Barclays’ upgrade support the catalyst but do not remove that risk.

The most relevant recent announcement is the Q1 2026 result itself, which showed 8.6% revenue growth and a shift from losses to a small profit. For a story previously clouded by modest earnings growth and falling free cash flow margins, this step back into the black matters for confidence in any operational turnaround. It gives investors a concrete reference point when weighing the upside from efficiency gains against the ongoing risks in client demand and competition.

Yet beneath the improving margins, investors should still be aware of the risk that intense competition and pricing pressure could eventually...

Read the full narrative on First Advantage (it's free!)

First Advantage's narrative projects $1.9 billion revenue and $168.3 million earnings by 2029. This requires 7.1% yearly revenue growth and a $203.1 million earnings increase from -$34.8 million today.

Uncover how First Advantage's forecasts yield a $15.00 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Before this latest quarter, the most pessimistic analysts were only assuming about 7.4% annual revenue growth and earnings of roughly US$169.3 million by 2029, so compared with the recent margin improvement and Barclays’ focus on execution, their story reflects a far more cautious view of how much Sterling integration and new technology can really add.

Explore another fair value estimate on First Advantage - why the stock might be worth just $15.00!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your First Advantage research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free First Advantage research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate First Advantage's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The future of work is here. Discover the 35 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com