- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing RB Global (RBA) Valuation After Mixed Share Price Momentum And Growth Expectations

Why RB Global (RBA) is on investors’ radar right now

RB Global (RBA) is back in focus after recent share price moves. The stock is up over the past week but down over the past month, prompting fresh interest in its valuation and business trends.

See our latest analysis for RB Global.

Recent share price momentum has been mixed, with a 1-day share price return of 1.97% and 7-day return of 2.58% offset by a 1-year total shareholder return that is slightly down, while the 3-year and 5-year total shareholder returns remain strong.

If RB Global’s mix of auctions, data, and services has caught your attention, it could be a good moment to broaden your search with 20 top founder-led companies

With annual revenue of US$4.7b, net income of US$403.9m, and the stock trading at US$104.72 at a reported discount to some valuation estimates, is this an opportunity or is the market already pricing in future growth?

Most Popular Narrative: 15.7% Undervalued

RB Global’s most followed narrative points to a fair value of $124.20 per share against the last close of $104.72, which frames a clear valuation gap for investors to examine.

Expansion of the international buyer base and new alliance partnerships, along with ongoing growth in e-commerce marketplace activities, are expected to drive higher transaction volumes and revenue as more asset sales and auctions move online. Joint ventures and acquisitions (e.g., LKQ in the U.K., J.M. Wood in the U.S., and new operations in Australia) are building a larger global footprint and improving cross-selling opportunities, supporting long-term revenue and margin growth.

Curious what kind of revenue path and margin profile would support that higher fair value, and how rich a future earnings multiple this narrative builds in? The full story connects ambitious profit growth assumptions with a valuation framework that leans heavily on expanding services and online volumes.

Result: Fair Value of $124.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear swing factors, including the possibility of softer transaction volumes if customers pull back on asset sales, and potential integration missteps related to recent acquisitions and new markets.

Find out about the key risks to this RB Global narrative.

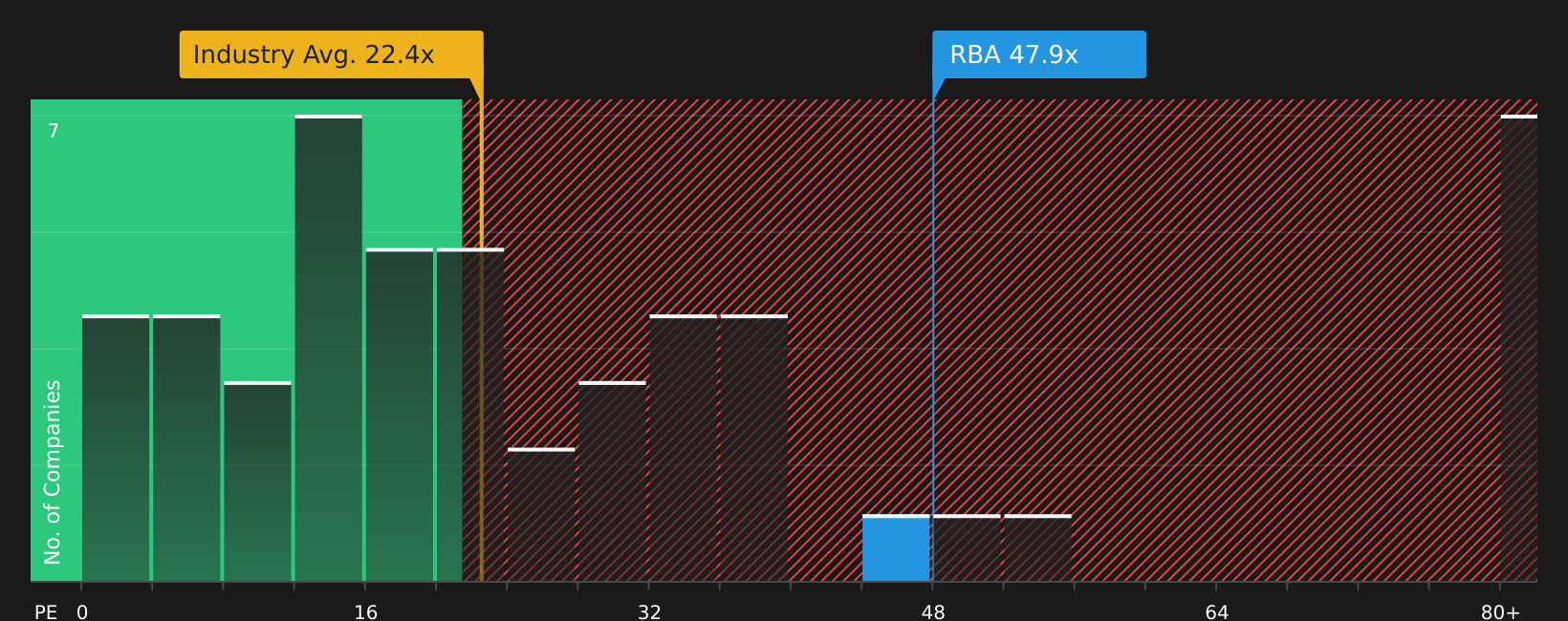

Another View: What The P/E Ratio Is Saying

The DCF based fair value points to upside, but the P/E picture is less forgiving. RB Global trades on a P/E of 48.3x versus a peer average of 31.9x and a fair ratio of 30.6x. This suggests investors are paying a premium that could amplify any disappointment.

For a closer look at how the current price compares with earnings based benchmarks, including sector peers and the fair ratio the market could move toward, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of cautious premium and upbeat narrative has you curious, take a closer look at the underlying data and form your own judgment. To understand what is making some investors optimistic, start with the 4 key rewards

Looking for more investment ideas?

Before you move on, consider exploring fresh opportunities across other companies that could fit your portfolio better than sticking with familiar options.

- Target value with 49 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial strength.

- Prioritize resilience through 67 resilient stocks with low risk scores designed to highlight companies with lower risk scores and more robust profiles.

- Hunt for potential future standouts using screener containing 21 high quality undiscovered gems that surface lesser known companies with strong underlying fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com