- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Can PVH’s (PVH) Leadership Shuffle Clarify the Calvin Klein and Tommy Hilfiger Investment Story?

- PVH Corp. recently reshaped its leadership, promoting Adelyn Cheong to CEO of PVH Americas, expanding Jonathan Bottomley’s remit across consumer and brand strategy, appointing Joel Samaha to lead global licensing and expansion, and naming Ying Wu as President, PVH China alongside her APAC finance role.

- This reshuffle concentrates global brand, consumer insight, and partnership responsibilities under experienced insiders and a long‑time adviser, potentially sharpening execution around Calvin Klein and Tommy Hilfiger across regions and channels.

- We’ll now examine how Adelyn Cheong’s move from leading PVH China to heading PVH Americas could influence PVH’s broader investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

PVH Investment Narrative Recap

To own PVH, you need to believe its Calvin Klein and Tommy Hilfiger franchises can translate brand strength into healthier margins despite tariffs, operational complexity, and mixed digital progress. The near term catalyst is whether execution on the PVH+ plan can lift earnings from a slim 0.3% net margin, while the key risk is that heavy dependence on two legacy brands and uneven D2C traction limit any payoff. The latest leadership reshuffle does not fundamentally change those near term stakes.

The most relevant update here is Adelyn Cheong’s promotion to CEO of PVH Americas, shifting a leader with China and APAC experience into PVH’s largest region. Given that analysts were expecting only about 2.4% annual revenue growth but a sharp earnings ramp, her track record around digital, consumer centricity, and operations sits squarely in the spotlight as PVH tries to turn consensus profit growth expectations into reality.

Yet behind this optimism, investors should also be aware that...

Read the full narrative on PVH (it's free!)

PVH's narrative projects $9.4 billion revenue and $707.7 million earnings by 2028. This requires 2.3% yearly revenue growth and about a $239 million earnings increase from $468.5 million today.

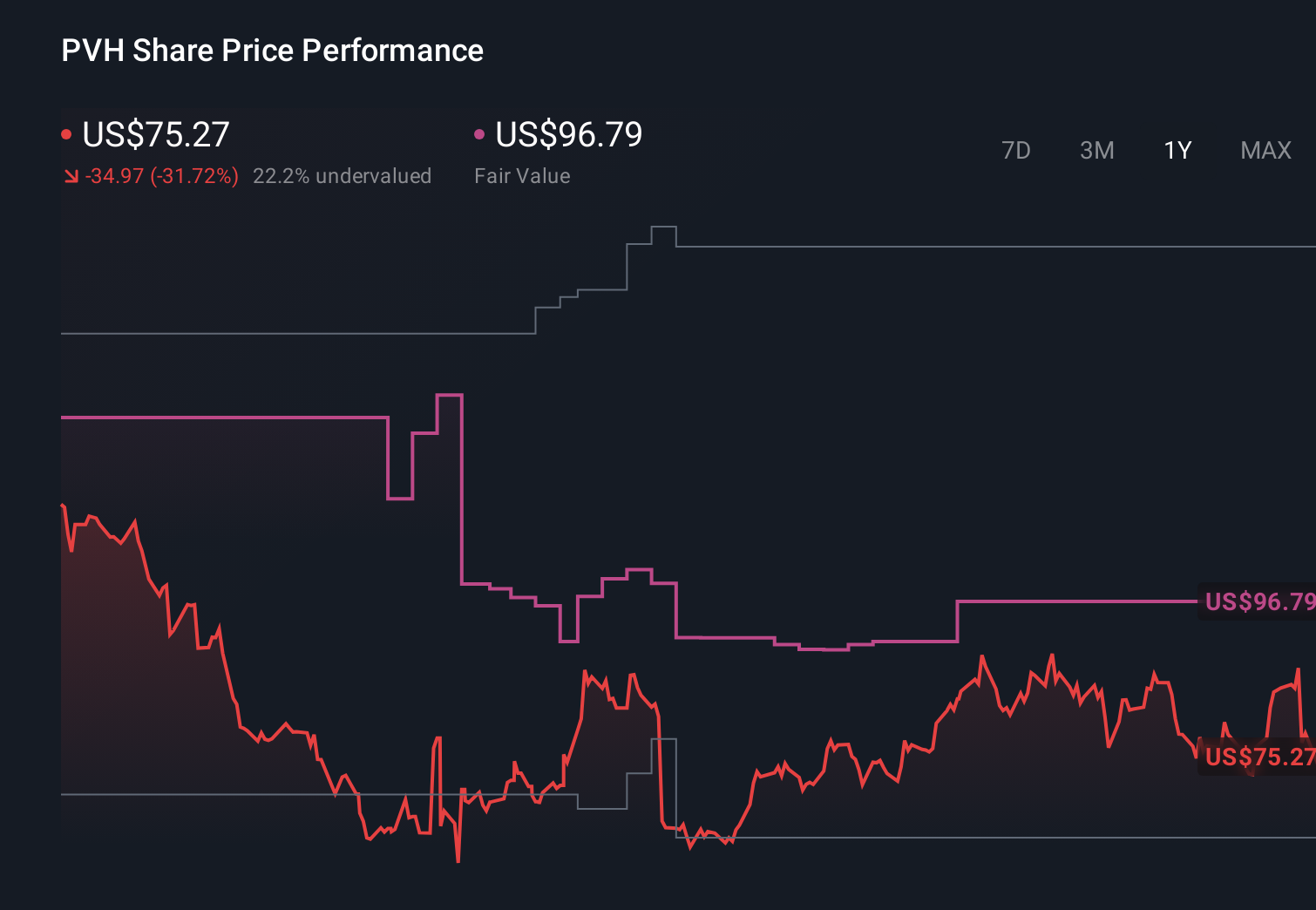

Uncover how PVH's forecasts yield a $96.79 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts see things very differently, assuming only about 1.3% annual revenue growth and needing earnings to climb to roughly US$766.0 million, so if you worry that online first rivals could keep chipping away at PVH’s wholesale roots, this new leadership story might or might not be enough to shift that more cautious view.

Explore 4 other fair value estimates on PVH - why the stock might be worth just $96.79!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your PVH research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free PVH research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PVH's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com