- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At CarMax (KMX) Valuation After Retail Sector Rotation On Strong Earnings From Major U.S. Retailers

CarMax (KMX) shares moved higher after stronger than expected quarterly results from major retailers like Target, Lowe's, and TJX. The reports sparked renewed interest in consumer discretionary stocks and a rotation back into retail.

See our latest analysis for CarMax.

At a share price of US$40.33, CarMax has seen a 3.62% 1 day share price return and a 9.21% 7 day share price return, while its 1 year total shareholder return is down 35.23%. This suggests recent momentum is improving against a weaker multi year backdrop as investors reassess risk after sector wide retail updates, earlier board changes and activist involvement.

If this kind of retail rebound has your attention, it could be a good time to broaden your search and review 20 top founder-led companies

With CarMax stock trading at US$40.33, a modest discount to both its intrinsic estimate and the average analyst target, the key question is whether investors are seeing a genuine value opportunity or if the market is already pricing in a recovery.

Most Popular Narrative: 5.3% Overvalued

CarMax's fair value in the most followed narrative sits at $38.31, slightly below the last close of $40.33. This frames the current debate over upside.

The continued focus on operational efficiencies and planned cost reductions in logistics and reconditioning are expected to support stable or increased net margins and profitability as savings enhance the bottom line.

Planned investments in new store locations and reconditioning centers are intended to increase the company's physical footprint and operational capacity, driving revenue growth through expanded service capacity and higher vehicle sales.

Want to see what kind of earnings path and profit profile have to line up for that fair value to make sense? The narrative leans on improving margins, a different mix of revenue drivers, and a future earnings multiple usually reserved for stronger growth stories. Curious which assumptions carry the most weight in that calculation and how sensitive the outcome is to small changes in them? The full narrative lays out those levers in detail.

Result: Fair Value of $38.31 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story also depends on continued credit discipline and stable wholesale margins. Any slip in loan losses or unit profitability could quickly challenge it.

Find out about the key risks to this CarMax narrative.

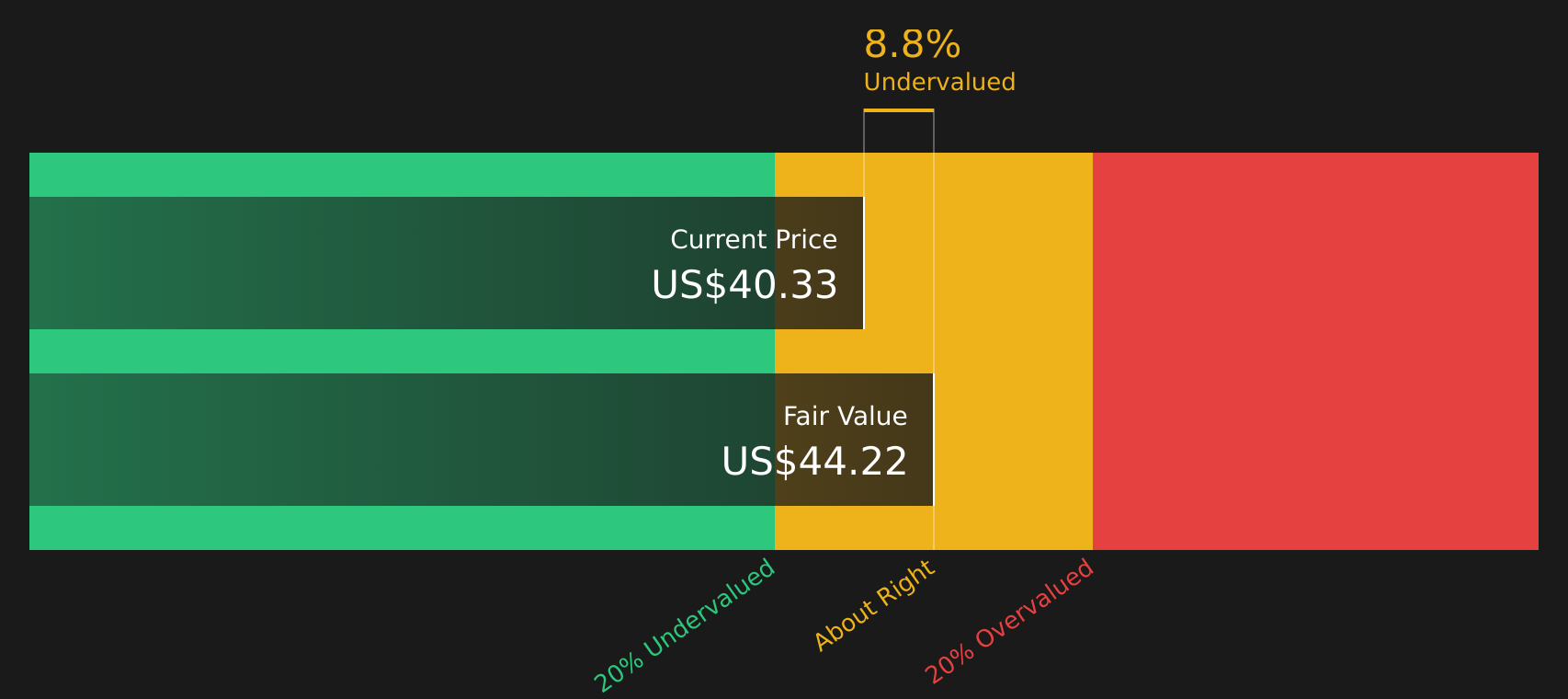

Another View: Cash Flows Point To A Different Story

While the most followed narrative sees CarMax as about 5.3% overvalued at $38.31, our DCF model presents a slightly different picture. On that view, the stock at $40.33 trades about 8.8% below an estimated $44.22 fair value. This raises the question of whether the market is leaning too heavily on earnings multiples and near term sentiment.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CarMax for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Uncertain which side of the CarMax story feels stronger right now: the risks or the potential rewards. Move quickly, review the data yourself, then weigh up the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you are serious about making the most of this research, do not stop at a single stock; broaden your opportunity set with targeted screeners that surface clear, data backed ideas.

- Zero in on quality at a discount by scanning 49 high quality undervalued stocks that pair strong fundamentals with prices that sit below many investors' radars.

- Protect your downside first by reviewing 66 resilient stocks with low risk scores that score well on resilience, stability, and balance sheet strength.

- Spot future standouts early by working through the screener containing 21 high quality undiscovered gems before they become crowded trades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com