- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Wynn Resorts (WYNN) Valuation After Strong Q1 Results And Macau Recovery Progress

Wynn Resorts (WYNN) is back in focus after reporting Q1 fiscal 2026 results that showed revenue up 9.2% year over year and adjusted EPS rising 16.8%, helping drive a 4.1% share move.

See our latest analysis for Wynn Resorts.

Even after the post earnings move, the recent 30 day share price return is down 8.81% and the year to date share price return is down 20.67%, while the 1 year total shareholder return of 8.47% points to a recovery that has taken time to build.

If this kind of rebound story interests you, it could be a good moment to broaden your search and look at 20 top founder-led companies

With earnings growing faster than revenue, analysts seeing room for higher EPS, and some valuation tools flagging a discount, the key question is simple: is Wynn Resorts genuinely undervalued, or is the market already pricing in that future growth?

Most Popular Narrative: 28.4% Undervalued

With Wynn Resorts last closing at $97.24 against a narrative fair value of $135.89, the current price sits well below what this widely followed view suggests.

The imminent launch of Wynn Al Marjan Island, with first-mover advantage and limited near-term competition in a potentially multi-billion-dollar new market, is a major forward catalyst that is currently underappreciated by investors and could drive a meaningful step-change in both consolidated revenue and EBITDAR.

Curious how this opening, projected earnings growth, improving margins, and a premium future P/E all connect to that higher fair value? The full narrative lays out the numbers and the logic behind them in detail.

Result: Fair Value of $135.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Macau staying supportive and large projects like Al Marjan hitting timelines and returns, with weaker trends or cost overruns as potential spoilers.

Find out about the key risks to this Wynn Resorts narrative.

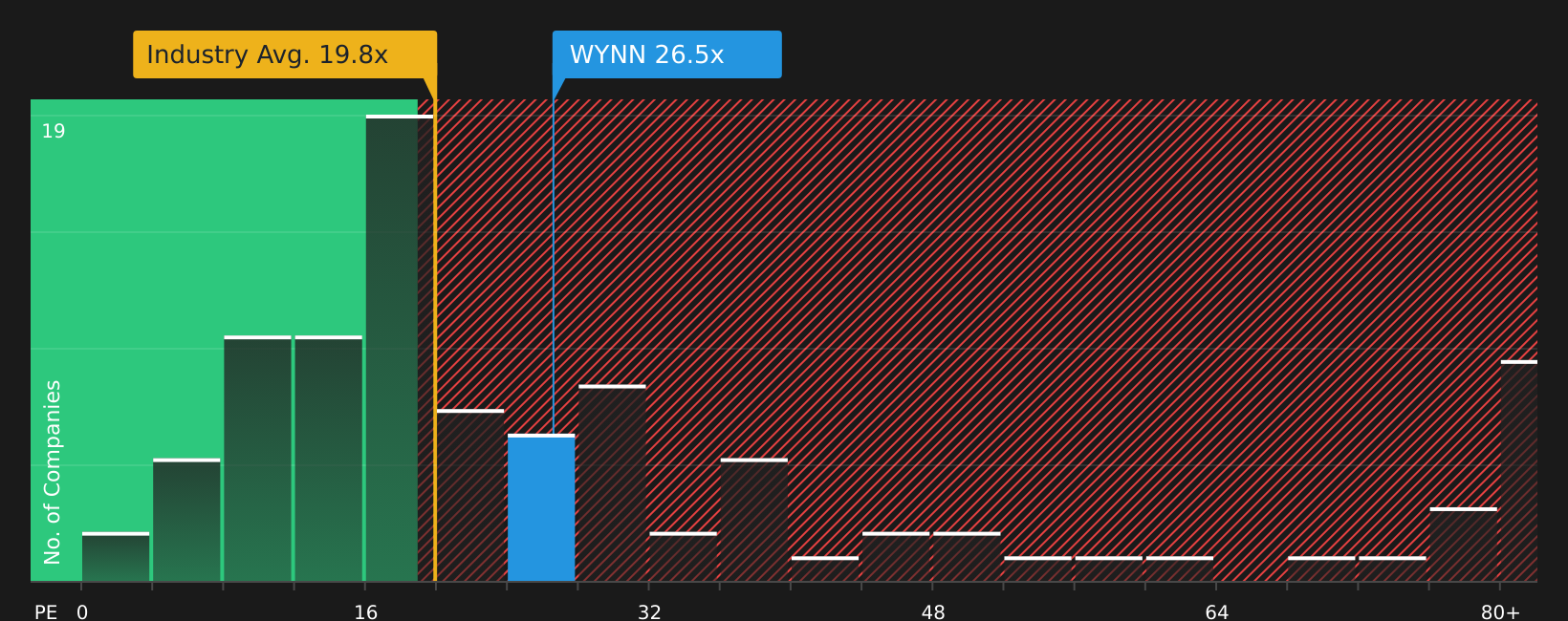

Another Angle on Valuation

That 28.4% discount to the narrative fair value stands in contrast to the current P/E of 26.5x. The stock trades above both the US Hospitality average of 19.8x and the peer average of 24.7x, yet below a fair ratio of 29.2x. This combination points to mixed signals on risk and opportunity.

To see how those P/E gaps play out in practice, and what they might mean for future repricing, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and caution resonates with you, it is worth looking through the underlying numbers yourself and forming a view quickly. To see how the balance of risks and rewards stacks up for your own thesis, check out the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Wynn Resorts has your attention, do not stop here. The same tools that surfaced this story can help you spot other opportunities before they move.

- Target potential value opportunities by scanning 49 high quality undervalued stocks that combine quality fundamentals with appealing pricing signals.

- Build a steadier income stream by reviewing 10 dividend fortresses that prioritize higher yields with a focus on resilience.

- Dial down portfolio risk by concentrating on 66 resilient stocks with low risk scores that score well on financial strength and volatility metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com