- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Oceaneering International (OII) Valuation After New West Delta Deep Marine Contract Win

Oceaneering International (OII) has announced that its Offshore Projects Group won an integrated offshore installation contract from Burullus Gas Company for Egypt’s West Delta Deep Marine project, covering subsea infrastructure, ROV support, and survey services.

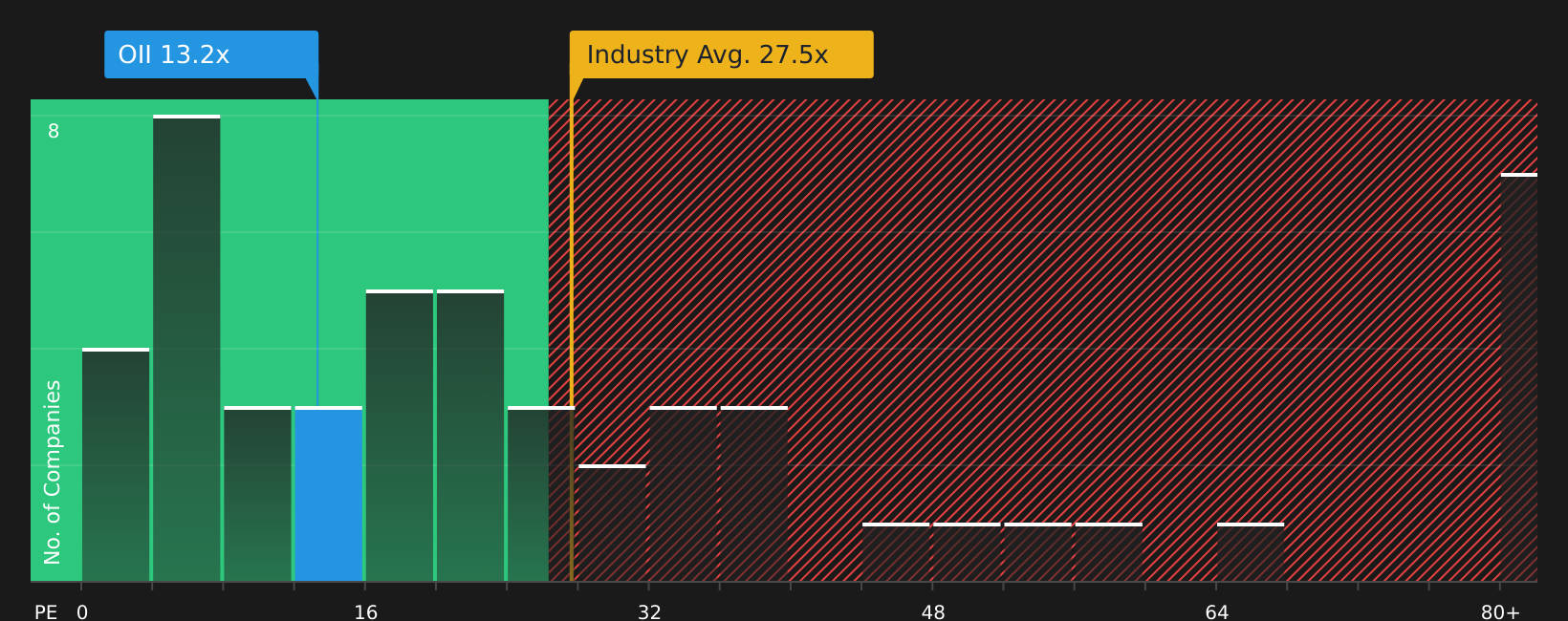

See our latest analysis for Oceaneering International.

At a share price of US$38.40, Oceaneering International has delivered a 54.53% year to date share price return and a 1 year total shareholder return of 103.17%. This suggests momentum has been building, even as recent insider stock grants and mixed first quarter results keep risk perceptions in focus.

If this offshore contract has caught your attention and you want to see where robotics and automation could matter next, take a look at 34 robotics and automation stocks

With shares at US$38.40, trading slightly above the average analyst target and near estimated intrinsic value, the key question for you is simple: is Oceaneering International undervalued today, or is the market already pricing in future growth?

Most Popular Narrative: 8.9% Overvalued

Oceaneering International's most followed narrative places fair value at $35.25, below the last close of $38.40. This frames the latest contract win against an already full valuation.

The ongoing global energy transition and intensifying decarbonization efforts continue to limit new offshore oil & gas developments, which threatens Oceaneering's long-term project backlog and could ultimately reduce future revenue growth as the addressable market gradually contracts.

Curious why a business with rising earnings is tied to such a cautious fair value path? The narrative leans heavily on shrinking margins, slower top line assumptions, and a much richer future earnings multiple. Want to see how those pieces fit together and what has to go right for the story to hold?

Result: Fair Value of $35.25 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear swing factors here, including the ADTech segment adding steadier government backed work, and higher margin subsea robotics potentially supporting pricing and earnings resilience.

Find out about the key risks to this Oceaneering International narrative.

Another Angle on Valuation

The narrative prices Oceaneering International at $35.25 using detailed earnings and discount assumptions. However, the current P/E of 11.3x sits well below the US Energy Services industry at 27.2x and peers at 37x, and above a fair ratio of 8.2x. Is the market underestimating risk or giving you a margin of safety?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Feeling torn between the optimistic contract news and the more cautious valuation signals? Take a moment to review the data for yourself and weigh both sides. A helpful place to start is with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If this Oceaneering International story has you thinking more carefully about price, risk, and potential, do not stop with just one stock when there are many others to compare.

- Spot potential value opportunities early by checking companies highlighted in the 51 high quality undervalued stocks.

- Prioritize stability and resilience by scanning stocks in the 67 resilient stocks with low risk scores.

- Hunt for fresh opportunities before they hit the spotlight with the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com