- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Undiscovered Gems in the US Market May 2026

In the last week, the United States market has stayed flat despite being up 27% over the past year, with earnings forecasted to grow by 17% annually. In this environment, identifying stocks with strong growth potential and solid fundamentals can lead to uncovering hidden opportunities that may not yet be widely recognized.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Southern Michigan Bancorp | 108.80% | 7.38% | 0.84% | ★★★★★★ |

| ASA Gold and Precious Metals | NA | 12.65% | 41.20% | ★★★★★★ |

| Sound Financial Bancorp | 16.13% | 0.44% | -12.60% | ★★★★★★ |

| SIFCO Industries | 12.27% | -4.21% | -2.87% | ★★★★★★ |

| First Northern Community Bancorp | NA | 7.26% | 11.00% | ★★★★★★ |

| Anbio Biotechnology | NA | -30.09% | -3.45% | ★★★★★★ |

| Affinity Bancshares | 41.71% | 1.36% | -0.22% | ★★★★★★ |

| Winchester Bancorp | 123.28% | 9.14% | -54.82% | ★★★★★★ |

| NameSilo Technologies | 3.13% | 14.25% | 15.06% | ★★★★★☆ |

| High Templar Tech | 13.55% | -66.76% | -26.62% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

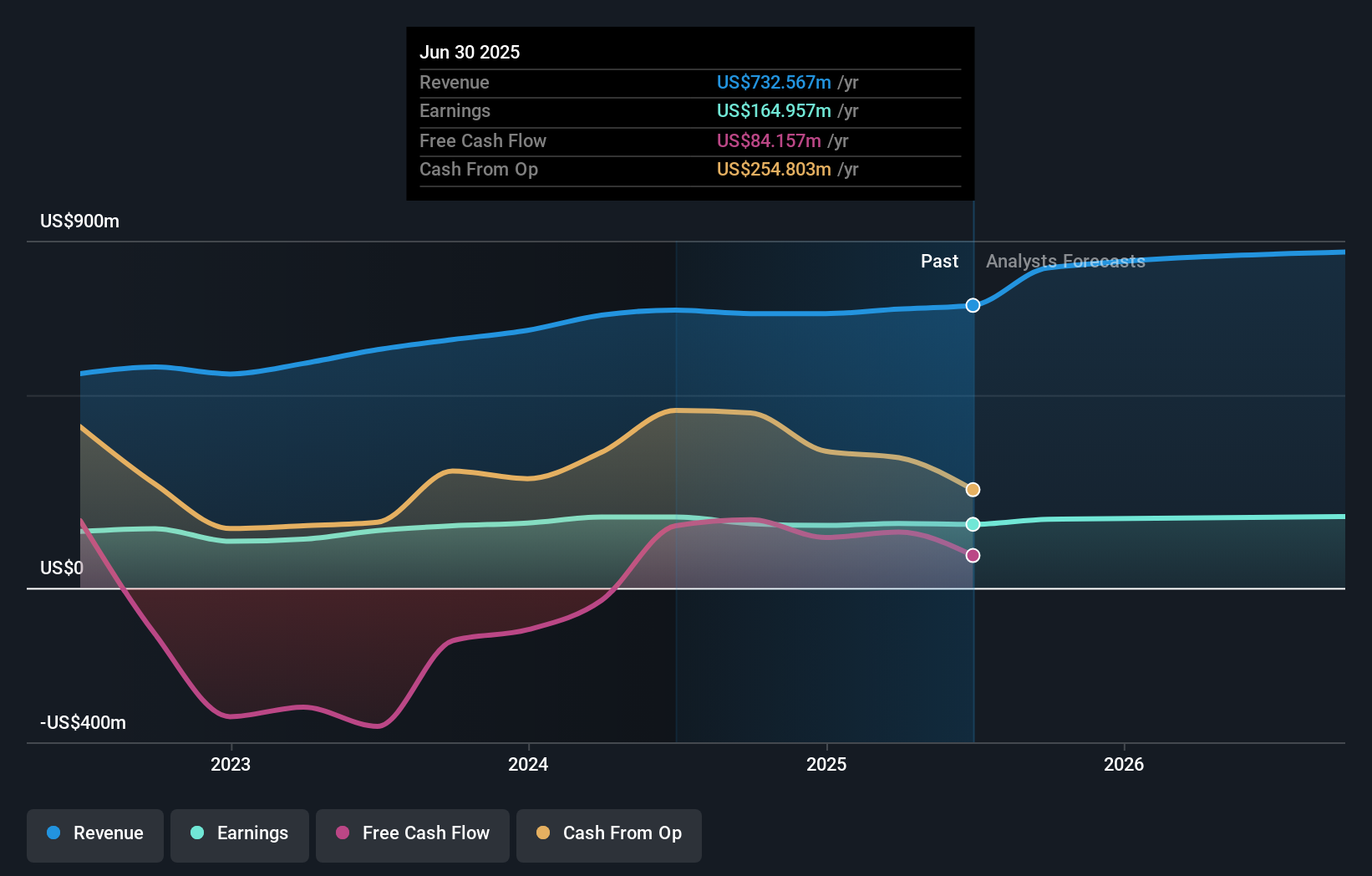

Pathward Financial (CASH)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Pathward Financial, Inc. is a bank holding company for Pathward, National Association, offering a range of banking products and services in the United States with a market cap of approximately $1.70 billion.

Operations: Pathward Financial generates revenue primarily from its Consumer segment, contributing $511.33 million, followed by the Commercial segment with $246.49 million.

Pathward Financial, with total assets of US$7.1 billion and equity of US$850.7 million, is making waves in the fintech space through strategic digital banking investments. Despite a high bad loan ratio at 2.4%, it boasts a robust net interest margin of 7.4%. The company has repurchased 855,201 shares this year for US$71.97 million, enhancing shareholder value amid competitive pressures from fintech rivals and regulatory challenges. With earnings growing at 7.5% annually over five years, Pathward remains a compelling choice for those eyeing potential in the financial sector's evolving landscape.

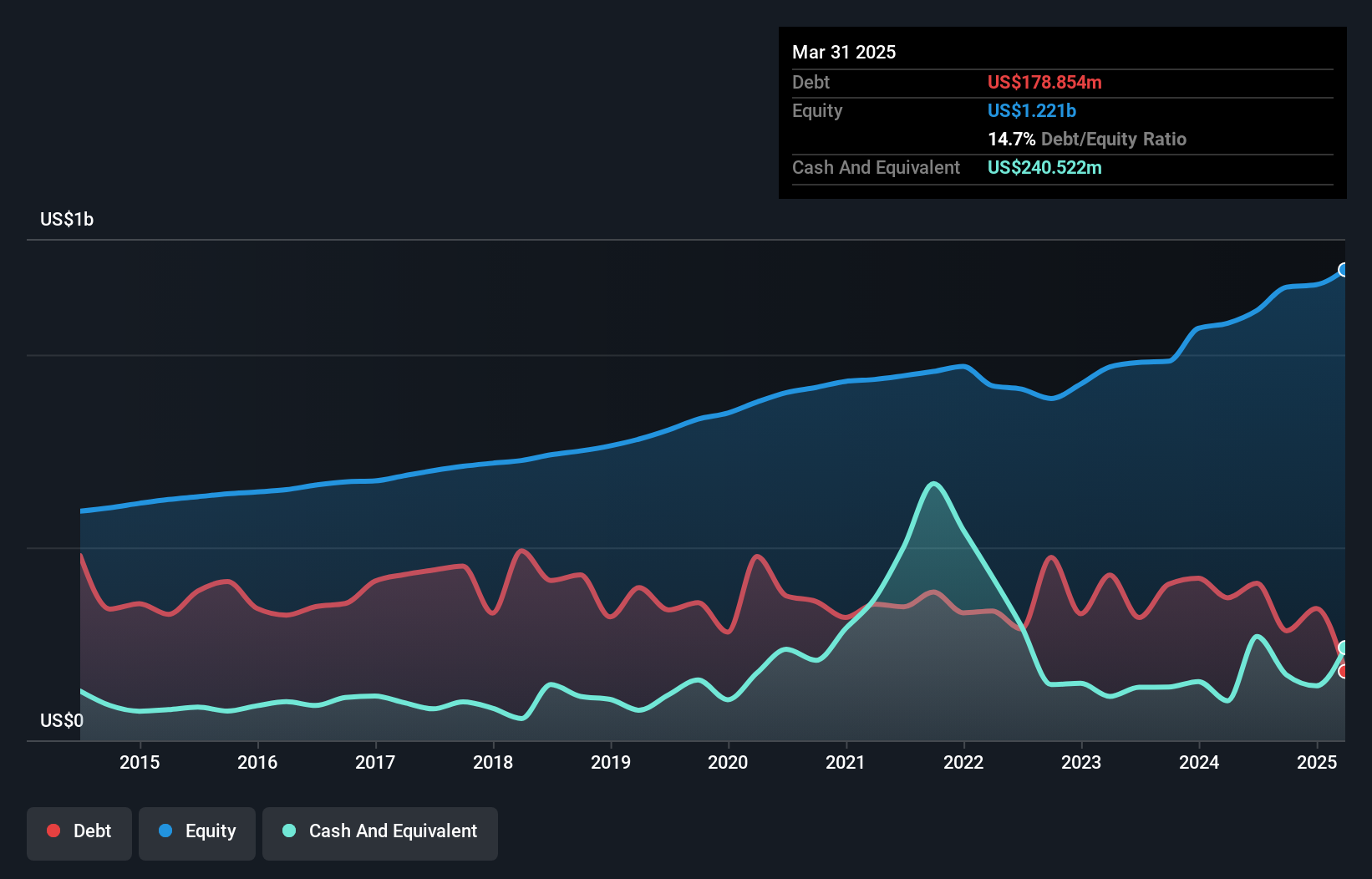

1st Source (SRCE)

Simply Wall St Value Rating: ★★★★★★

Overview: 1st Source Corporation, with a market cap of $1.74 billion, is the bank holding company for 1st Source Bank, offering commercial and consumer banking services, trust and wealth advisory services, and insurance products to individual and business clients in the United States.

Operations: 1st Source Corporation generates revenue primarily from its commercial banking segment, accounting for $426.31 million.

1st Source, with total assets of US$9.1 billion and equity of US$1.3 billion, stands out for its robust financial health. The bank's total deposits are at US$7.2 billion against loans totaling US$6.9 billion, reflecting a solid balance sheet structure. Its net interest margin sits comfortably at 4.1%, while the allowance for bad loans is more than adequate at 229%. Over the past five years, earnings have grown by 7.5% annually, although recent growth of 14% lagged behind industry averages of nearly 23%. Recently, it completed a share repurchase program worth $37 million and increased dividends to $0.43 per share.

- Click here and access our complete health analysis report to understand the dynamics of 1st Source.

Gain insights into 1st Source's historical performance by reviewing our past performance report.

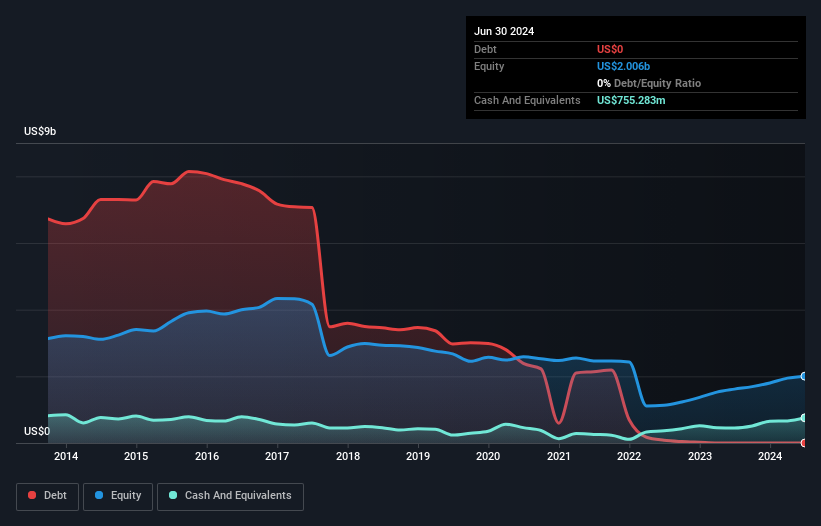

Teekay (TK)

Simply Wall St Value Rating: ★★★★★★

Overview: Teekay Corporation Ltd. is involved in the global marine transportation of crude oil and other marine services, with a market capitalization of $1.16 billion.

Operations: Teekay generates revenue primarily from crude oil marine transportation and related marine services. The company's financial performance includes a market capitalization of approximately $1.16 billion.

Teekay showcases a compelling profile with its debt to equity ratio dropping from 82.3% to 2.1% over five years, indicating strong financial management. The company is trading at a significant discount, about 80.1% below its estimated fair value, suggesting potential upside for investors who spot this opportunity early. Recent earnings highlight a net income of US$153 million for Q1 2026 on sales of US$286 million, reflecting robust performance despite industry challenges. A special dividend of $1 per share further sweetens the deal for shareholders, while earnings growth outpaces the Oil and Gas sector's negative trend by reaching 13%.

- Click here to discover the nuances of Teekay with our detailed analytical health report.

Evaluate Teekay's historical performance by accessing our past performance report.

Key Takeaways

- Gain an insight into the universe of 336 US Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com