- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

What Photronics (PLAB)'s New Senior Finance Leader Means For Shareholders

- Earlier in May 2026, Photronics, Inc. appointed Christopher Dayton as Senior Vice President, Finance, reporting to President & Chief Financial Officer Eric Rivera and overseeing financial planning, treasury, tax, and global financial processes from its Brookfield, Connecticut headquarters.

- Dayton’s more than 25 years of global manufacturing finance experience, including senior roles at BIC Corporation and Campbell Soup Company, adds depth to Photronics’ financial leadership as it pursues complex, capital-intensive growth initiatives.

- With Dayton now supporting Photronics’ financial governance and long-term growth plans, we’ll examine how this leadership change influences its investment narrative.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Photronics Investment Narrative Recap

To own Photronics, you need to believe in the long term demand for advanced photomasks across IC and display markets, supported by heavy, multi year capital investment. The appointment of Christopher Dayton as Senior Vice President, Finance looks more like a reinforcement of financial governance than a change to the near term catalyst, which still centers on executing that elevated capex program, or to the key risk around balance sheet pressure if returns on these projects fall short.

In this context, the recent installation of an advanced mask writer at the Korea facility stands out, as it directly supports Photronics’ push into higher value AMOLED and Gen 8.6 display opportunities. Dayton’s role in financial planning and treasury oversight sits alongside this expansion, which ties the company’s growth ambitions even more closely to disciplined capital allocation and the timing of future cash flows.

Yet, while these investments are critical, investors should also be alert to the risk that heavy capex could strain cash generation if...

Read the full narrative on Photronics (it's free!)

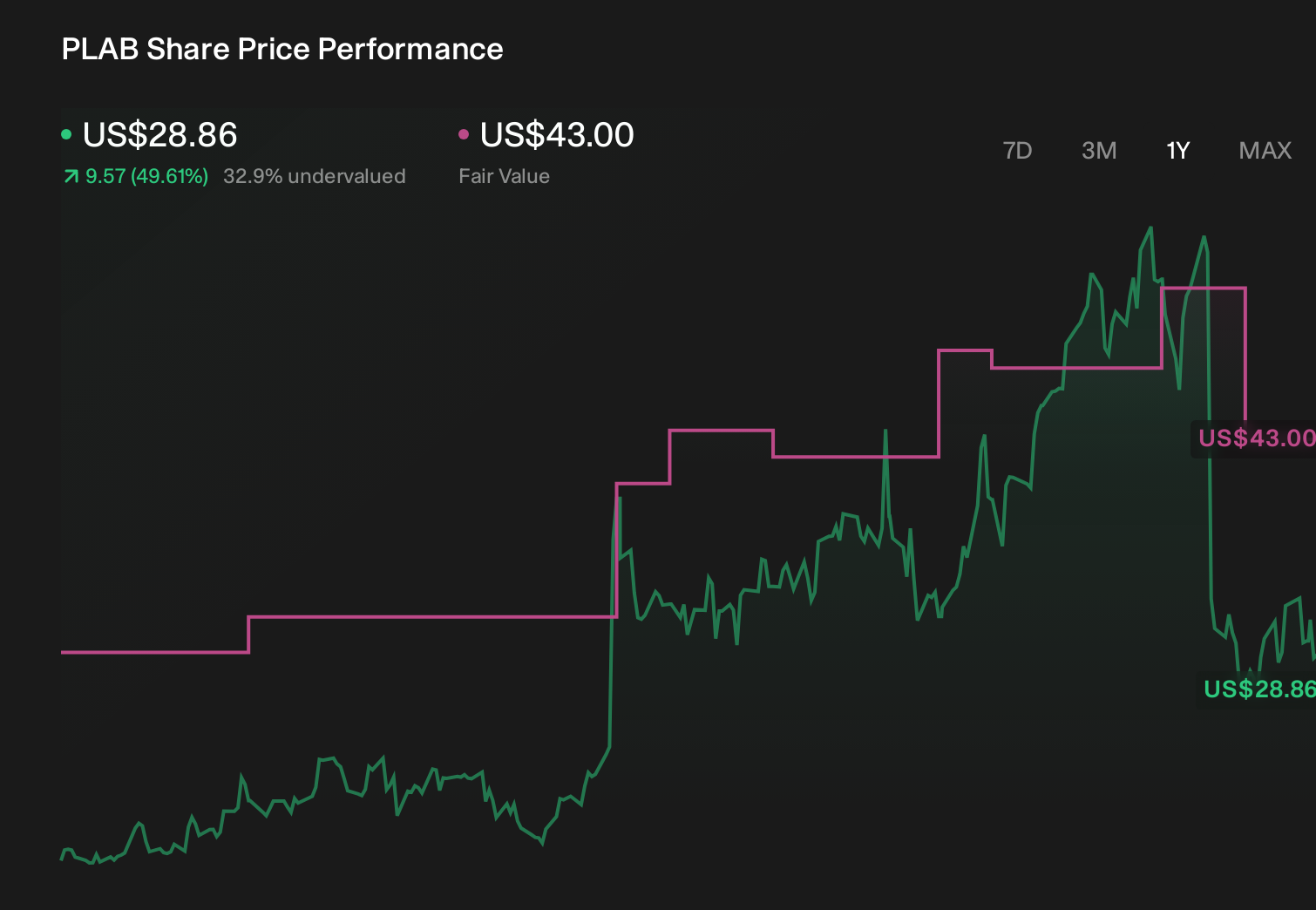

Photronics’ narrative projects $973.4 million revenue and $138.1 million earnings by 2029.

Uncover how Photronics' forecasts yield a $51.50 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Seven fair value estimates from the Simply Wall St Community span roughly US$18 to US$52 per share, reflecting very different expectations. When you set those views against Photronics’ elevated capital spending needs, it underlines how important it is to compare several independent takes on the company’s prospects.

Explore 7 other fair value estimates on Photronics - why the stock might be worth as much as $51.50!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Photronics research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com