- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

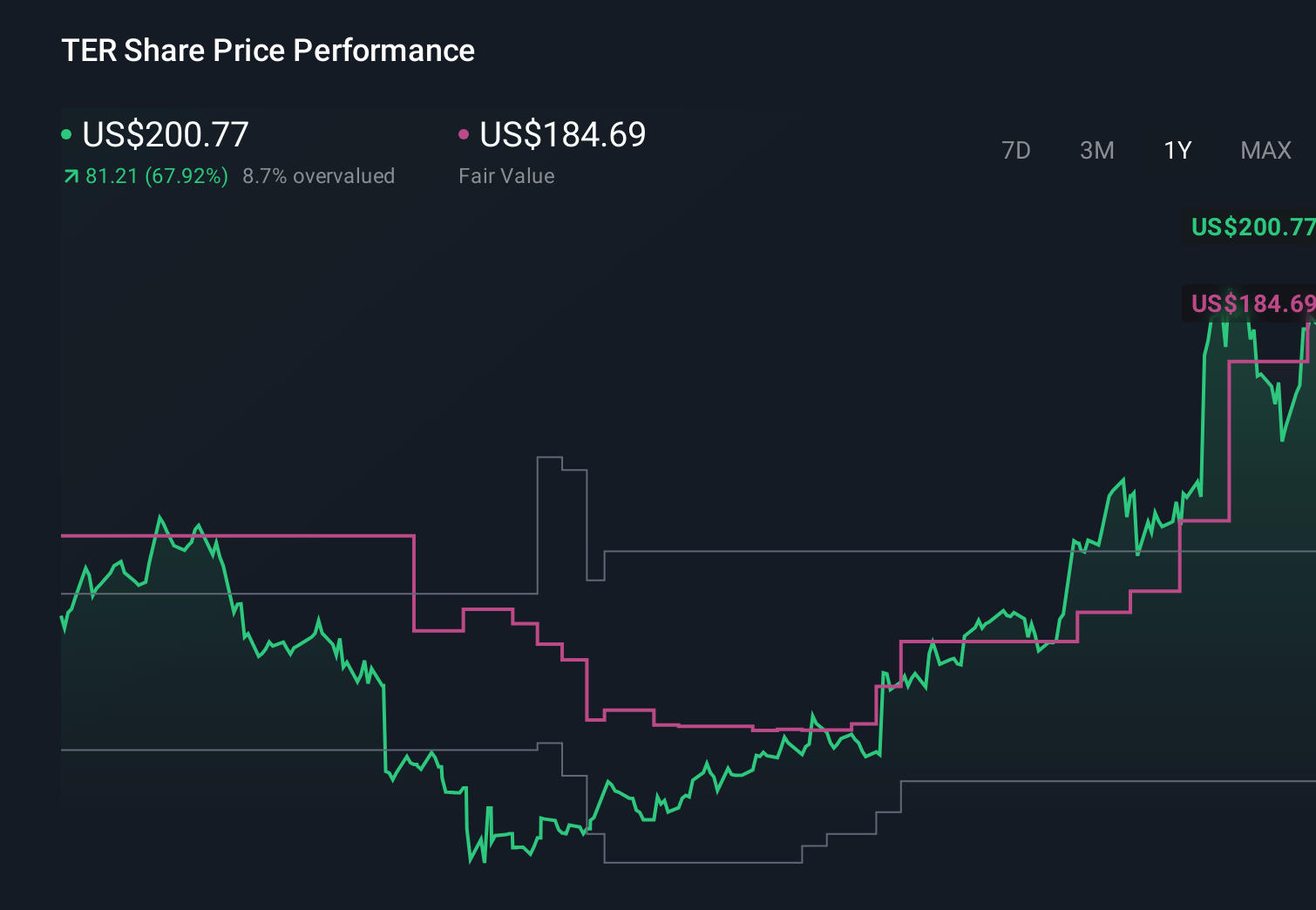

Why Teradyne (TER) Is Down 5.2% After Record Q1, New Dividend And Softer Q2 Outlook

- In recent weeks, Teradyne reported record first-quarter revenue of US$1.28 billion, declared a US$0.13 per-share quarterly dividend payable on June 12 2026, and issued guidance for a sequential decline in second-quarter revenue and adjusted profit.

- These results highlight how AI-driven semiconductor test demand, now representing nearly 70% of Teradyne’s revenue mix, is reshaping the company’s earnings profile and risk exposure.

- We’ll now examine how the AI-driven surge in semiconductor test demand updates Teradyne’s investment narrative and future earnings assumptions.

Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

Teradyne Investment Narrative Recap

To own Teradyne, you need to believe that AI-driven demand for semiconductor test equipment and related automation can support durable earnings, even with cyclical swings. The key near term catalyst is whether AI infrastructure spending continues translating into strong test orders, while the biggest risk is how exposed that demand is to geopolitics and export rules. The latest earnings beat and cautious Q2 outlook do not materially change those twin forces, but they sharpen attention on valuation and volatility.

The most relevant recent announcement is Teradyne’s record Q1 2026 revenue of US$1,282.5 million, up 87% year over year, powered by AI semiconductor test demand now approaching 70% of sales. That surge directly ties into the core catalyst around AI accelerators and high bandwidth memory test, but it also heightens the risk that any slowdown in AI chip capex, tighter trade policy or prolonged export restrictions could have an outsized impact on near term results.

But behind the strong AI test story, investors should also be aware of the growing concern around elevated valuation and insider selling...

Read the full narrative on Teradyne (it's free!)

Teradyne's narrative projects $6.7 billion revenue and $2.0 billion earnings by 2029. This requires 20.9% yearly revenue growth and an earnings increase of about $1.1 billion from $854.1 million today.

Uncover how Teradyne's forecasts yield a $369.53 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts expected Teradyne to reach about US$7.3 billion in revenue and US$2.2 billion in earnings by 2029, which is a far more bullish view than the baseline narrative and hinges heavily on AI data center test demand remaining strong and relatively uninterrupted; the latest AI driven Q1 beat may support that case, but it could also magnify concerns around concentration risk and show just how differently you and other investors might interpret the same numbers.

Explore 7 other fair value estimates on Teradyne - why the stock might be worth as much as 21% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Teradyne research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Teradyne research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Teradyne's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com