- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

How New Callable Debt, NII Pressures, and Crypto Exposure Could Reframe Bank of America (BAC)

- In mid-May 2026, Bank of America Corporation announced and completed several fixed-income offerings, issuing multiple series of senior unsecured, callable notes across maturities from 2027 to 2046 with fixed coupons ranging from 4.25% to 6.00% and individual deal sizes up to US$50 million. These transactions coincided with broader scrutiny of the bank’s profitability profile, including an analyst downgrade highlighting pressure on net interest income and structural cost headwinds.

- Beyond capital-raising, the bank featured in areas as varied as crypto-related exposures, AI-powered bond trading platforms, and a US$2.25 million ATM fee settlement, underlining how its funding actions, regulatory exposure, and evolving business mix are all in focus for investors assessing its long-term earnings quality.

- We’ll now examine how CFRA’s downgrade and concerns over net interest income growth interact with this funding activity to reshape Bank of America’s investment narrative.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Bank of America Investment Narrative Recap

To own Bank of America, you need to be comfortable with a large, globally diversified bank that is still heavily driven by net interest income, while also investing in technology and fee-based businesses. CFRA’s downgrade puts the pressure on near term NII trends and cost control, but the recent series of small, callable fixed income deals does not materially change the main near term catalyst or the key risk around margin pressure.

The most relevant recent development here is CFRA’s move from Buy to Hold, citing valuation and sensitivity to net interest income declines, even as Q1 2026 earnings and capital returns remained solid. That reassessment sits directly against the backdrop of Bank of America’s ongoing funding activity and highlights how closely many investors are watching the balance between rising funding costs and efforts to stabilise net interest income.

Yet behind the strong capital returns and steady dividends, investors should be aware of growing concern that net interest income growth is lagging peers and ...

Read the full narrative on Bank of America (it's free!)

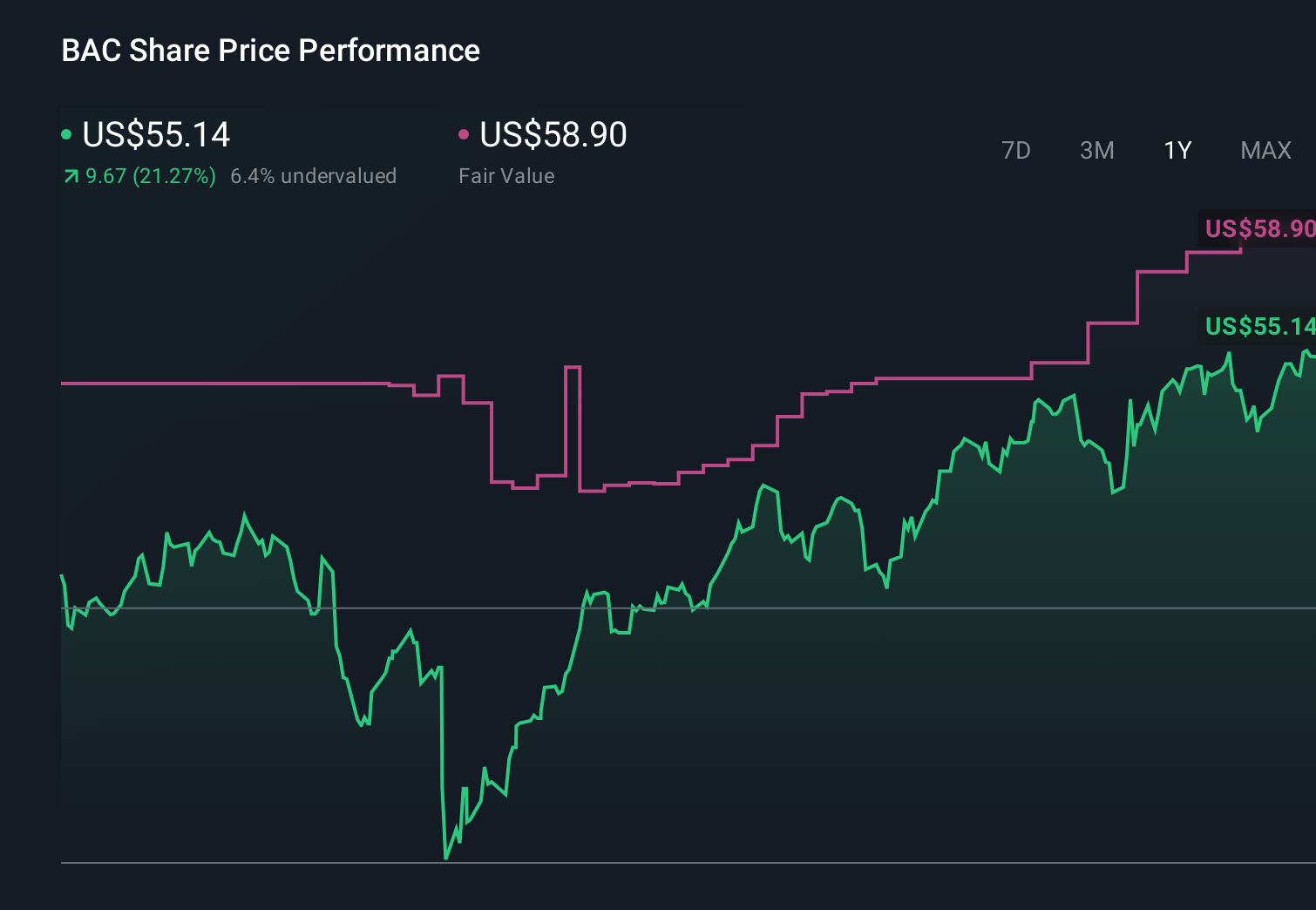

Bank of America's narrative projects $133.8 billion revenue and $36.7 billion earnings by 2029. This requires 6.9% yearly revenue growth and a $6.4 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $62.98 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Eight members of the Simply Wall St Community value Bank of America between US$56.50 and about US$66.88 per share, showing a wide span of expectations. Against this, concerns about slower net interest income growth and margin pressure give you a different lens on what could drive the bank’s future performance, so it can be useful to compare several of these viewpoints.

Explore 8 other fair value estimates on Bank of America - why the stock might be worth just $56.50!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Bank of America research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com