- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Can Carvana’s (CVNA) Stellantis Push Reframe Its Competitive Moat Or Expose Strategic Limits?

- Carvana recently expanded beyond used cars by acquiring Stellantis dealerships and applying its online, no-haggle model, with its Casa Grande, Arizona store becoming the top-selling Chrysler, Jeep, Ram, and Dodge dealer in the US.

- This move into new car sales has intensified friction with traditional Stellantis dealers and triggered tighter acquisition restrictions, highlighting how Carvana’s approach can unsettle entrenched industry structures.

- We’ll now examine how Carvana’s push into new car sales via Stellantis dealerships influences its investment narrative and long-term positioning.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

Carvana Investment Narrative Recap

To own Carvana, you need to believe its online, asset-light retail model can keep scaling while maintaining profitability and operational discipline. The Stellantis new-car push tests that thesis at the margins, but the immediate catalyst still looks tied to execution in reconditioning and logistics, while the biggest risk remains cost creep and complexity as volumes grow. So far, this expansion appears incremental rather than a fundamental shift to the near term risk/reward profile.

The recent ADESA Chicago and Syracuse integrations are especially relevant here, because they speak directly to whether Carvana can handle higher throughput without eroding unit economics. As Carvana experiments with new-car sales via Stellantis stores, the added reconditioning capacity and national inventory pooling from these sites could either support smoother scaling or magnify bottlenecks and one off costs, making these build outs a key operational backdrop to watch alongside the Stellantis tensions.

Yet behind the growth story, investors should also be aware of how rising compliance and operational costs could start to...

Read the full narrative on Carvana (it's free!)

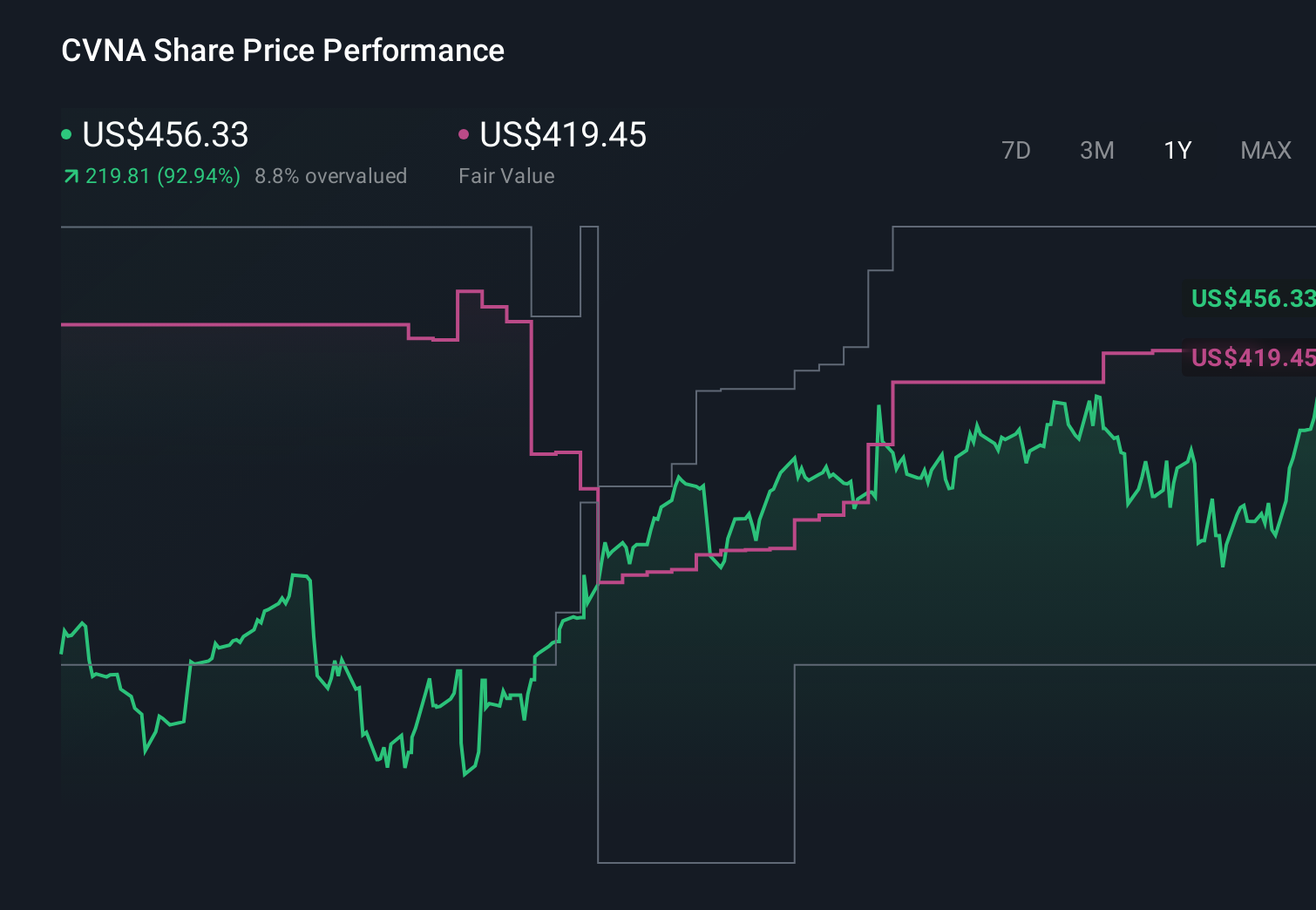

Carvana's narrative projects $40.2 billion revenue and $3.0 billion earnings by 2029. This requires 25.6% yearly revenue growth and about a $1.6 billion earnings increase from $1.4 billion today.

Uncover how Carvana's forecasts yield a $428.50 fair value, a 560% upside to its current price.

Exploring Other Perspectives

Compared with the consensus story, the most pessimistic analysts already assumed only about US$38.4 billion of revenue and US$1.7 billion of earnings by 2029, so this Stellantis development could either soften their concerns about rising compliance and capital costs or reinforce them, which is why it is worth weighing several viewpoints before you decide what you believe.

Explore 14 other fair value estimates on Carvana - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Looking For Alternative Opportunities?

Our top stock finds are flying under the radar-for now. Get in early:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com