- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Assessing NXP Semiconductors (NXPI) Valuation After A Powerful Share Price Surge

Recent performance snapshot for NXP Semiconductors (NasdaqGS:NXPI)

NXP Semiconductors (NasdaqGS:NXPI) has drawn investor attention after a strong run, with the stock up around 40% over the past month and roughly 34% over the past 3 months.

See our latest analysis for NXP Semiconductors.

That surge sits on top of a stronger backdrop, with a 1-year total shareholder return of 53.91% and a 3-year total shareholder return of 96.90%, while recent 1-day and 7-day share price gains suggest positive momentum rather than a one off move.

If this kind of momentum has your attention, it could be a good moment to see which other chip related plays are moving through the 44 AI infrastructure stocks

With NXP trading around $310.15 and sitting at a premium to its analyst price target and intrinsic value estimate, the key question is whether recent strength leaves more upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 4% Overvalued

The most followed narrative currently pegs NXP Semiconductors' fair value at $298.29, which sits below the last close of $310.15, setting up a valuation built on detailed growth and margin assumptions.

The industrial & IoT business is seeing a broad-based cyclical recovery across all geographies, now extending beyond consumer IoT and into core industrial applications. This, combined with growing customer engagements around higher performance and Edge AI-capable MCU/MPU platforms, is setting the stage for a return to NXP's historical 8 to 12% annual growth rate in this segment, benefitting top-line performance.

Want to see what kind of revenue build, margin lift, and future earnings multiple are baked into that fair value line? The underlying narrative leans on detailed segment growth, higher profitability assumptions, and a tighter discount rate, all pulling together into a single target investors are watching.

Result: Fair Value of $298.29 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still real swing factors here, including tougher China competition and the risk that acquisitions lift costs faster than revenues for a while.

Find out about the key risks to this NXP Semiconductors narrative.

Another way to look at NXP's valuation

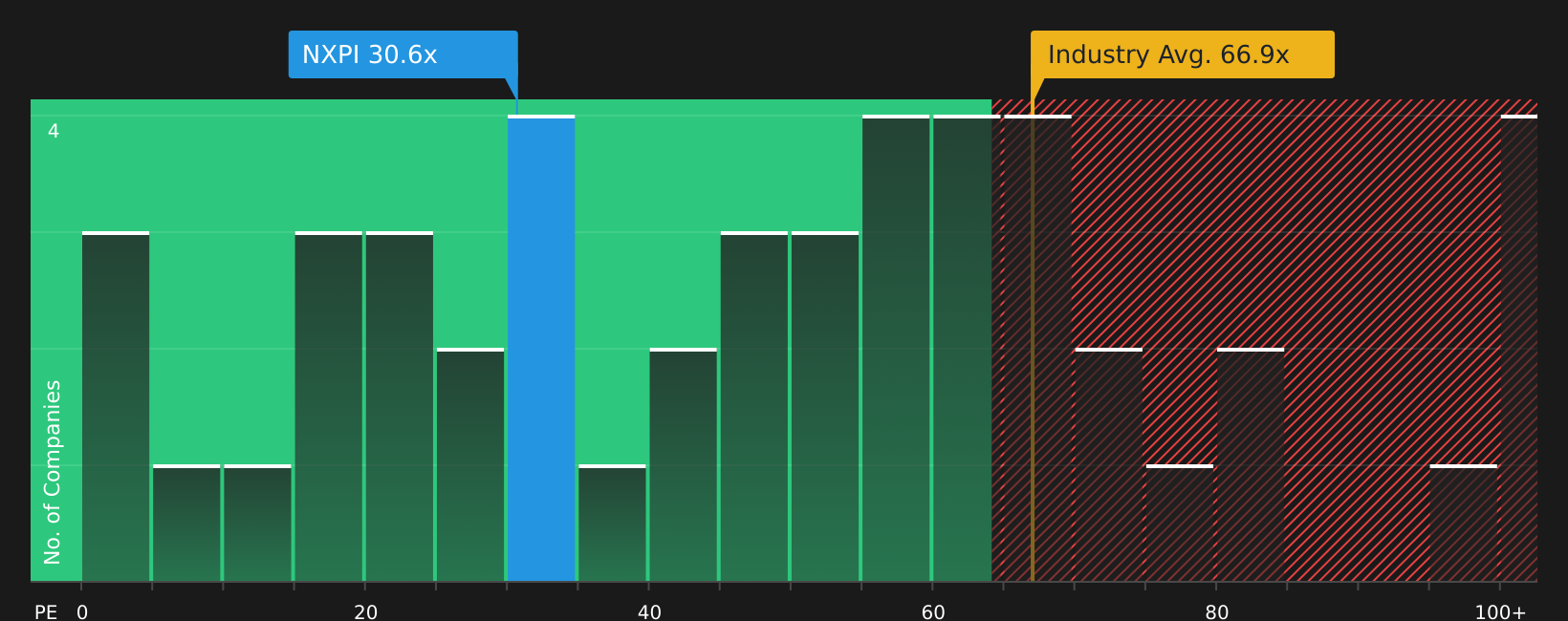

The first narrative leans on detailed growth and margin forecasts to argue NXP is around 4% overvalued, but the P/E story is a bit different. At 29.5x earnings versus about 58.3x for the US Semiconductor industry and 105.4x for peers, the stock trades at a steep discount, while the fair ratio of 36.5x implies the market could shift closer to that level over time. Does that gap point to valuation risk if earnings disappoint, or room for the multiple to move if expectations hold up?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment mixed between strong returns and questions around valuation, it makes sense to check the data yourself and move quickly while the picture is fresh. To weigh the positives against the concerns in one place, take a close look at the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If NXP has you thinking more broadly about your portfolio, this is the moment to scan for other opportunities before the next wave of interest hits.

- Spot potential mispricings early by checking out 51 high quality undervalued stocks that combine solid fundamentals with room for the market to reassess.

- Strengthen your income stream by reviewing 10 dividend fortresses that aim to pair higher yields with resilience.

- Sleep easier by focusing on 67 resilient stocks with low risk scores that score well on financial health and business stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com