- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Simpson Manufacturing (SSD) Valuation As Shares Show Mixed Recent Returns

Stock performance snapshot

Simpson Manufacturing (SSD) has drawn investor attention after recent price moves, with the stock up around 3.3% over the past month but down about 11.7% over the past 3 months.

At a last close of US$182.00 and a market value near US$7.35b, the company has a trailing 1 year total return of roughly 12%, alongside reported annual revenue of US$2,381.88m and net income of US$355.42m.

See our latest analysis for Simpson Manufacturing.

Recent trading has been choppy, with a 1-day share price gain of 1.9% and a 30-day share price return of 3.3%. However, the 90-day share price return is down 11.7%, while the 1-year total shareholder return sits near 12%. This suggests that momentum has cooled after a stronger long term run.

If this kind of mixed performance has you comparing ideas, it could be a good time to broaden your watchlist and check out 18 top founder-led companies

With Simpson Manufacturing trading near US$182.00 and sitting close to analyst estimates and intrinsic value models, the key question is whether investors are overlooking further upside or if the stock already reflects its future growth.

Most Popular Narrative: 16.4% Undervalued

On the most followed narrative, Simpson Manufacturing's fair value of $217.80 sits meaningfully above the last close at $182.00, setting up a valuation story built around earnings power and margins rather than short term price swings.

The accelerating adoption of off-site, modular, and mass timber construction solutions is creating significant demand for high-performance, engineered fasteners and connectors, an area where Simpson continues to see double-digit OEM volume growth and increasing traction with new digital and software solutions. This is likely to support above-market revenue growth.

Curious what kind of revenue pace, margin profile and earnings multiple are needed to arrive at that fair value gap. The narrative leans heavily on steady top line expansion, firmer profit margins and a richer future P/E, plus a specific discount rate that brings it all back to today's price.

Result: Fair Value of $217.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on housing and construction demand remaining resilient, while higher steel and input costs could pressure margins and challenge the current valuation story.

Find out about the key risks to this Simpson Manufacturing narrative.

Another angle on value

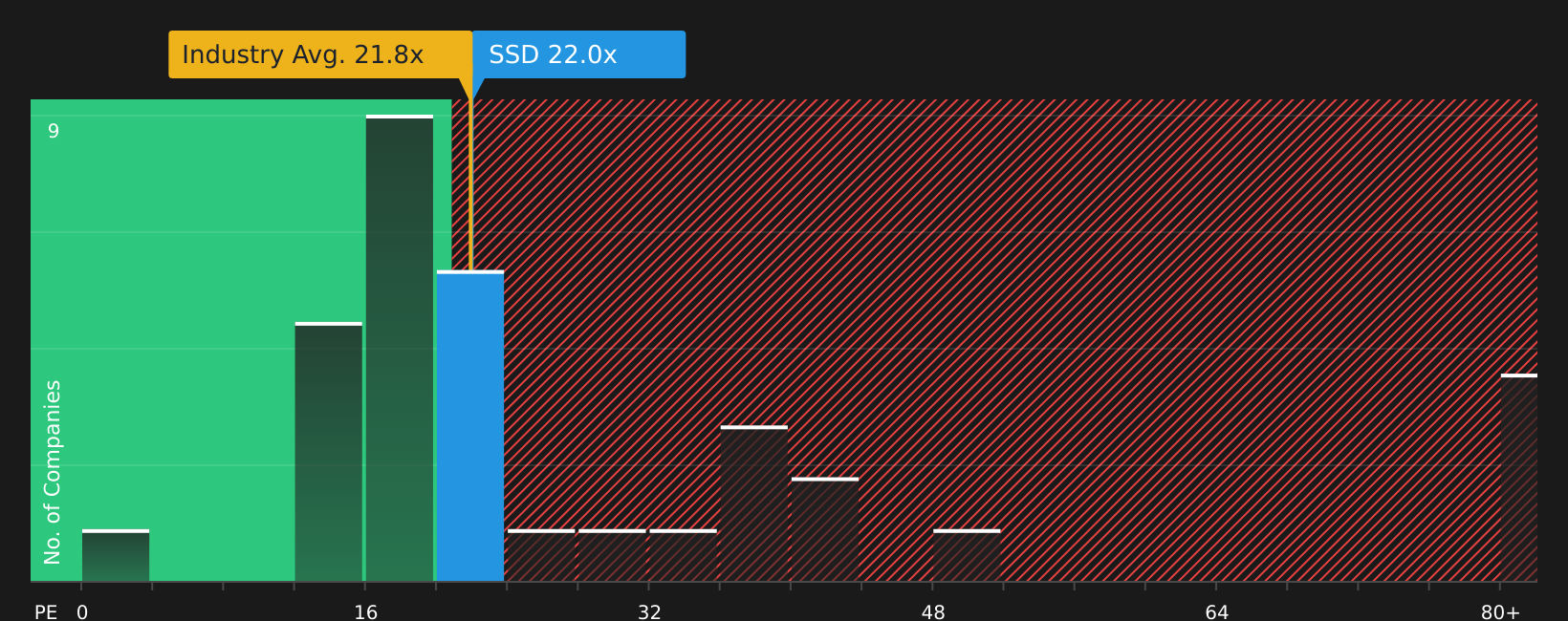

The narrative points to a fair value of $217.80, but the current P/E of 21.1x tells a more cautious story. It is slightly richer than the US Building industry at 20.3x, yet cheaper than peers at 25.2x and under the 23.1x fair ratio that the market could drift toward. For you, that raises a simple question: is this a moderate premium or a reasonable entry for a quality business?

To see how this pricing gap looks when you stress test assumptions using earnings multiples, take a closer look at our valuation breakdown for Simpson Manufacturing, including how it stacks up against peers and the fair ratioSee what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The blend of optimism and caution in this article is useful, but the real test is how it aligns with your own view. Move quickly and weigh the potential upside yourself by checking out the 3 key rewards

Looking for more investment ideas?

If Simpson Manufacturing is already on your radar, do not stop there. Use this momentum to line up your next opportunities before the crowd catches on.

- Spot potential value plays early by scanning 52 high quality undervalued stocks that combine attractive prices with stronger fundamentals.

- Secure more dependable income streams by reviewing 12 dividend fortresses that focus on higher-yield stocks.

- Protect your capital with a shortlist built from 65 resilient stocks with low risk scores that aim for resilience when conditions get tougher.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com