- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

Aura Minerals (NasdaqGS:AUGO) Valuation In Focus After Strong Q1 Output Gains And Rising Cost Concerns

Aura Minerals (AUGO) is back in focus after first quarter results showed higher gold equivalent output, record revenue and a move from loss to profit, alongside insider selling and rising cost concerns.

See our latest analysis for Aura Minerals.

The share price has pulled back recently, with a 7 day share price return of down 6.69% and a 30 day share price return of down 30.69%. However, the year to date share price return of 51.28% and a 1 year total shareholder return above 3x indicate that longer term momentum remains notable as investors reassess the recent dividend increase, quarterly earnings and upcoming conference appearance.

If strong production updates have your attention, it could be a moment to broaden your watchlist with other producers through the 33 elite gold producer stocks.

With the stock down sharply in the past month but still showing very strong multi year returns, alongside an intrinsic discount and a gap to analyst targets, you have to ask: is this a fresh entry point, or is the market already pricing in future growth?

Most Popular Narrative: 68.6% Overvalued

Based on the most followed narrative, Aura Minerals' fair value of $44.88 sits well below the last close at $75.64, which is a wide gap investors will want to understand before making any valuation calls.

The analysts have a consensus price target of $44.88 for Aura Minerals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $52.8, and the most bearish reporting a price target of just $34.2.

There is a detailed growth story sitting behind that fair value, built on brisk earnings expansion, a margin reset and a valuation multiple that still assumes discipline on dilution and capital spend. This raises the question of what combination of revenue growth, profitability shift and discounting connects today’s profits to that future earnings base and fair value.

Result: Fair Value of $44.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued execution on MSG productivity gains and the NASDAQ listing’s push for higher liquidity could both challenge the current view that the stock is overvalued.

Find out about the key risks to this Aura Minerals narrative.

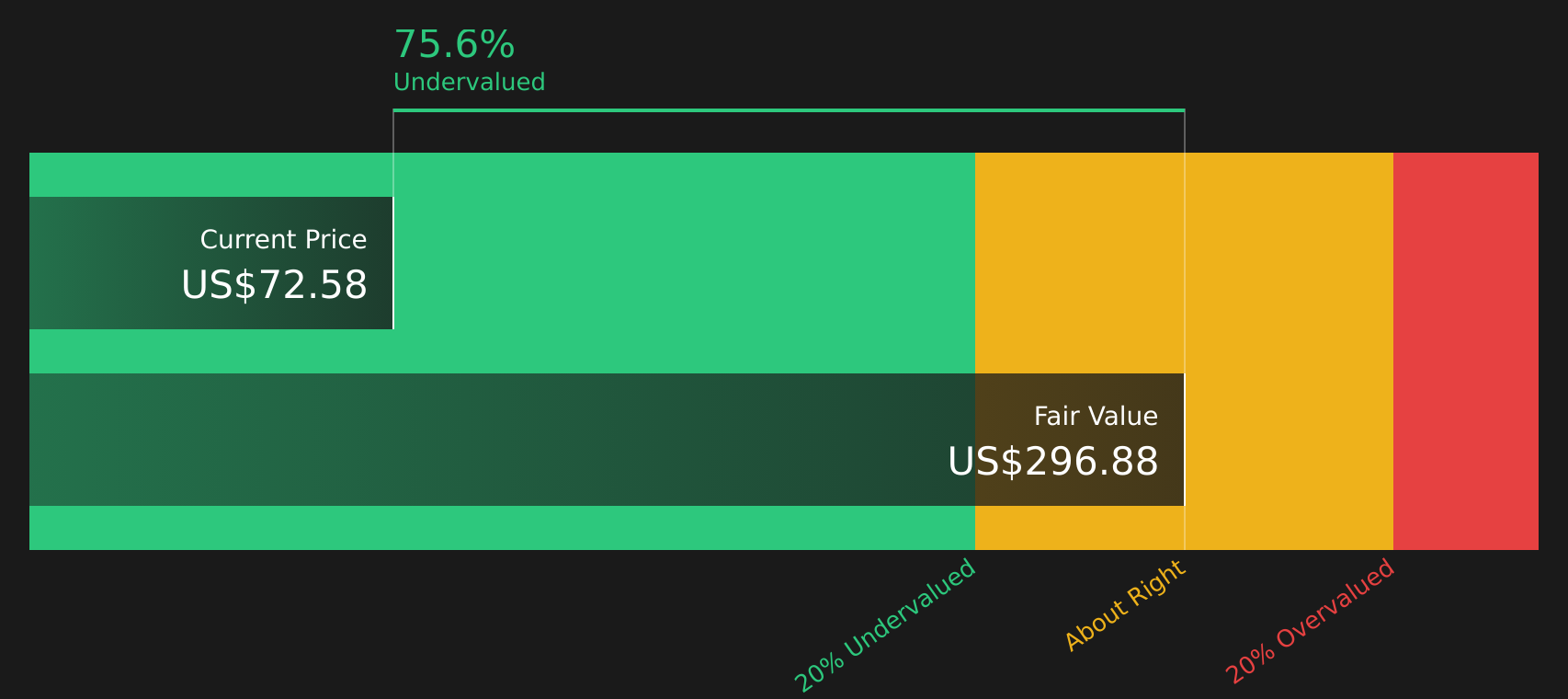

Another View: DCF Suggests A Very Different Story

While analyst targets point to Aura Minerals being overvalued around $75.64 versus a fair value of $44.88, the Simply Wall St DCF model paints almost the opposite picture, with an estimated future cash flow value of $298.39, suggesting the stock trades at a steep discount instead. Which framework feels more realistic to you: earnings multiples, or long term cash flows?

Our DCF model is only as useful as the assumptions you believe in, so it is worth stress testing the inputs and asking how sensitive that $298.39 figure is to changes in growth, margins and discount rates before leaning too heavily on it as a guide for decision making. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aura Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment split between risks and rewards, it makes sense to look through the data yourself and decide where you stand. If you want a quick way to weigh both sides before prices move again, start with the 3 key rewards and 4 important warning signs.

Looking for more investment ideas?

If Aura Minerals is on your radar, this is the moment to widen your search and line up a few more stocks that could strengthen your portfolio.

- Spot potential bargains before the crowd by scanning 52 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect them yet.

- Build a steadier income stream by reviewing 12 dividend fortresses that focus on higher yields with an emphasis on resilience.

- Sleep a little easier at night by checking 65 resilient stocks with low risk scores that stand out for lower risk scores and more robust profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com