- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

StoneX Group (SNEX) Valuation Check After Strong Earnings Beat And Sharply Higher Net Income

StoneX Group (SNEX) is back on investors’ radar after reporting second quarter results that showed net income and earnings per share more than doubling versus a year earlier, with earnings topping analyst expectations.

See our latest analysis for StoneX Group.

The earnings beat comes after a strong run for the stock, with the share price up 31.4% over the past three months and a 70.7% year to date share price return. The 5 year total shareholder return of more than 4x highlights how long term holders have been rewarded.

If you are looking for other ideas in financial services and adjacent areas, this is a good moment to broaden your search with 18 top founder-led companies

With earnings per share more than doubling and the stock already up sharply, the big question now is whether StoneX is still trading at a discount, or if the recent surge means the market is already pricing in future growth.

Price-to-Earnings of 19.7x: Is it justified?

On a headline basis, StoneX trades on a P/E of 19.7x, which prices the stock above its peer average but below the wider US Capital Markets group.

The P/E ratio compares the share price to earnings per share, so a higher figure often means the market is willing to pay more today for each dollar of current earnings. For a global financial services network like StoneX, that can reflect how investors view the sustainability and quality of earnings across its Commercial, Institutional, Retail, and Payments segments.

Compared to its direct peer set, StoneX is described as expensive with a 19.7x P/E versus a 14.7x peer average, which suggests investors are assigning a premium to its earnings profile. At the same time, that 19.7x P/E is said to be good value versus the broader US Capital Markets industry average of 40x, which points to a much lower valuation than many larger sector players. Relative to an estimated fair P/E of 15.1x, the current multiple is also indicated as rich, a level the market could move toward if sentiment or earnings expectations shift.

Explore the SWS fair ratio for StoneX Group

Result: Price-to-Earnings of 19.7x (OVERVALUED)

However, there are still risks here, including any reset in earnings expectations toward the indicated fair P/E and shifts in sentiment around global trading activity.

Find out about the key risks to this StoneX Group narrative.

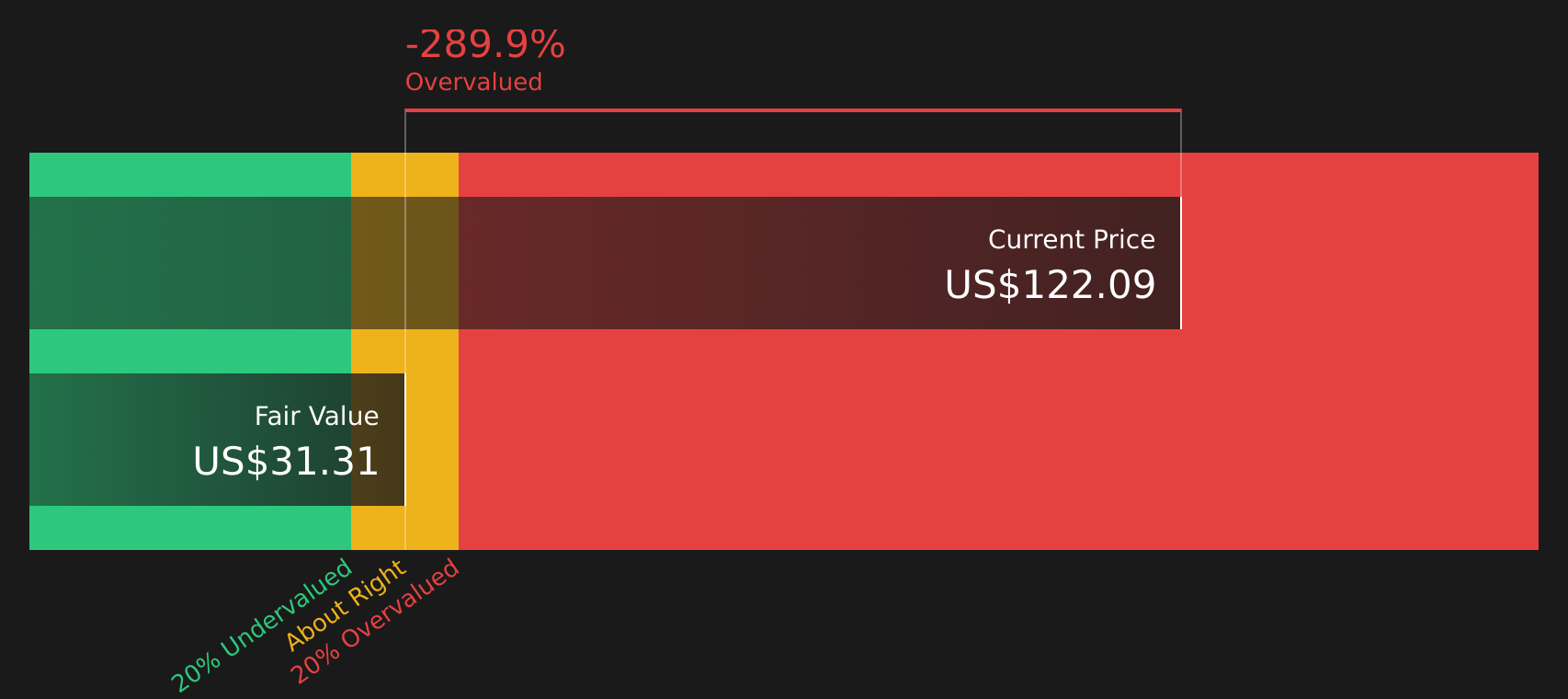

Another View: Cash Flows Paint a Stricter Picture

While the P/E ratio suggests StoneX looks relatively inexpensive versus the broader US Capital Markets group, the SWS DCF model sends a different message. At a share price of $110.8, the stock is reported as trading well above an estimated future cash flow value of $31.31, which points to an overvalued reading on this method. For an investor weighing these two signals, the key question is which one should carry more weight.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out StoneX Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals on value and expectations can feel unsettling, so do not wait to form an informed view based on the full data set. To see how the upside and downside balance out, take a closer look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you might miss opportunities that suit your goals even better. Broaden your watchlist using focused screeners that surface clear, data backed ideas.

- Target resilience by checking companies that pass strict balance sheet filters through the solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for potential value by scanning companies with stronger fundamentals and attractive pricing using the 52 high quality undervalued stocks.

- Spot potential long term compounding stories before they are widely followed by reviewing the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com